You're sitting at the kitchen table, two W-2s and a stack of 1099s staring you down. It’s tax season. Again. If you’re like most couples, you’re probably wondering if the 2024 tax calculator married filing jointly tools are actually going to give you a straight answer or just a headache. Taxes are weirdly personal, and for married folks, the math gets complicated fast.

Honestly, most people just want to know two things: Are we getting a refund, and did the IRS change the rules on us? The short answer is yes, things changed. Inflation was a beast, so the IRS bumped up the brackets and the standard deduction to keep us from "bracket creep"—that annoying situation where a small raise at work actually leaves you with less money because you’re pushed into a higher tax tier.

The Numbers That Actually Matter for Your 2024 Return

If you're using a 2024 tax calculator married filing jointly, the very first thing it’s going to ask for is your combined income. But before you even get to the "taxable" part, you get a massive freebie. For the 2024 tax year (the ones you’re filing in early 2025), the standard deduction for married couples filing jointly jumped to $29,200.

That is a $1,500 increase over the previous year.

🔗 Read more: Freddie Mac Customer Service Explained (Simply)

Think about that for a second. You basically get to ignore nearly thirty grand of your income before the government even starts looking at your wallet. If you or your spouse are 65 or older, you get an extra $1,550 on top of that. Blind? Another $1,550. These "sweeteners" are why most couples don't bother with itemizing anymore. Unless you have massive mortgage interest or huge medical bills, the standard deduction is usually the winner.

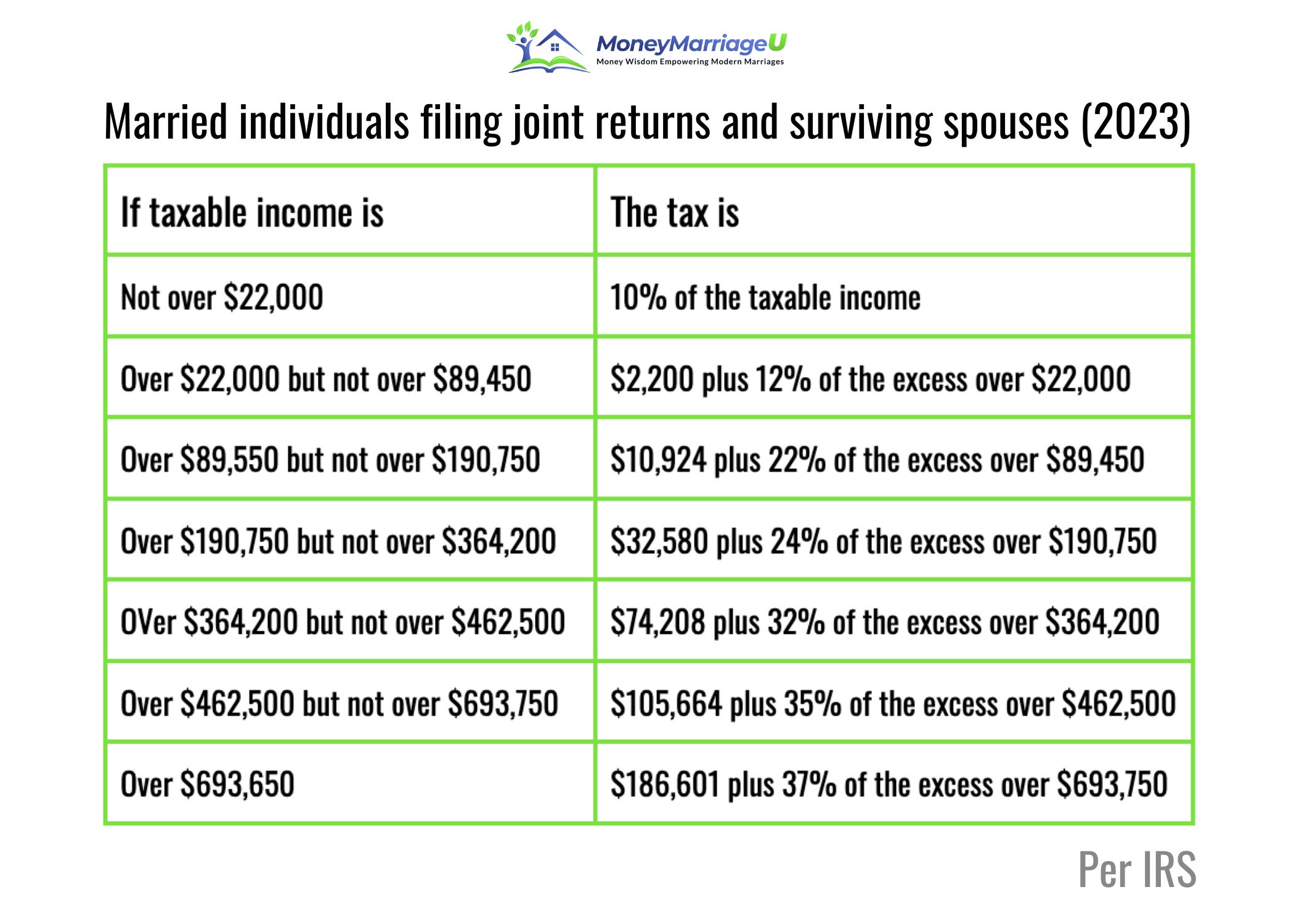

2024 Tax Brackets for Joint Filers

The IRS doesn't just charge you one flat rate. It’s a ladder. You pay a little bit at the 10% rate, then a little more at the 12% rate, and so on. Here is how the 2024 brackets actually shake out for a married couple:

- 10%: $0 to $23,200

- 12%: $23,201 to $94,300

- 22%: $94,301 to $201,050

- 24%: $201,051 to $383,900

- 32%: $383,901 to $487,450

- 35%: $487,451 to $731,200

- 37%: Over $731,200

Let’s say you and your spouse make a combined $100,000. You don't pay 22% on the whole thing. You take off your $29,200 standard deduction first. Now you're at $70,800 in taxable income. That puts your "top" dollar in the 12% bracket. You’re actually doing pretty well.

Why a 2024 Tax Calculator Married Filing Jointly Can Save You From the "Marriage Penalty"

You've heard of the marriage penalty, right? It’s that old idea that two people living together pay more in taxes than they would if they stayed single. While that still happens for very high earners (we’re talking half-million-dollar households), for most of us, there’s actually a "marriage bonus."

If one spouse makes $80,000 and the other makes $10,000, filing jointly is a massive win. The lower-earning spouse "pulls" the higher-earner’s income down into the lower brackets. It’s basically a way to average out your earnings.

However, don't just assume.

📖 Related: Why Your Certified Management Accountant Practice Test Scores Are Lying to You

Sometimes—rarely, but sometimes—filing separately makes sense. Usually, this happens if one person has massive student loans on an income-driven repayment plan or huge out-of-pocket medical expenses. Most 2024 tax calculator married filing jointly tools allow you to run the numbers both ways. It takes an extra ten minutes, but it could save you a couple of grand.

Credits You Shouldn't Leave on the Table

Deductions lower the income you're taxed on, but credits are the real MVPs. They are a dollar-for-dollar reduction of the tax you owe.

- Child Tax Credit: Still at $2,000 per kid under age 17. The refundable portion (the part you get back even if you owe zero tax) is up to $1,700 for 2024.

- Earned Income Tax Credit (EITC): If you’re a family with kids making under $66,819 (for 3+ kids), this can be huge. The max credit for 2024 is $7,830. That’s not a typo.

- Dependent Care Credit: If you're paying for daycare so you both can work, you can claim a percentage of those costs. It’s usually capped at $3,000 for one kid or $6,000 for two or more.

Common Mistakes That Trip Up Couples

The IRS processed over 160 million returns last year. They see the same errors every single time.

First off, names must match Social Security cards. If your spouse changed their name after the wedding but didn't tell the Social Security Administration, your e-file will likely get rejected. It sounds dumb, but it happens thousands of times a year.

✨ Don't miss: The 4 elements to a contract: Why your "handshake deal" might actually be legal

Secondly, don't forget the "other" income. Did you sell some Bitcoin? Did you have a high-yield savings account that actually paid decent interest for once? You’ll get a 1099-INT or 1099-B for those. If you don't report it, the IRS computers will catch it six months from now and send you a "CP2000" notice with interest and penalties. Just don't.

Taking Action: Your Next Steps

Stop procrastinating. Seriously.

The first thing you should do is gather your documents. Put them in one physical folder or one digital one. You need those W-2s, 1099s, and any 1098-E forms for student loan interest.

Next, find a reliable 2024 tax calculator married filing jointly online. Use a few different ones to see if the numbers align. If you're using software like TurboTax or H&R Block, they’ll do the heavy lifting, but it’s always smart to have a "ballpark" number in your head first so you aren't shocked by the final result.

Finally, check your withholding. If you ended up owing a ton of money this year, go to your HR portal at work and update your W-4. It’s a five-minute fix that prevents a massive bill next April. If you got a massive refund, you might actually want to lower your withholding. Why give the government an interest-free loan all year when that money could be in your own savings account?

The tax code is a mess, but for most married couples, 2024 is actually looking slightly better than previous years thanks to those inflation adjustments. Run the numbers, claim your credits, and get it over with.