So you've finally landed that gig or promotion, and you're staring at a contract that says you're making thirty bucks an hour. It sounds solid. It feels like a real "adult" wage. But then your brain starts doing that frantic mental math while you’re trying to figure out if you can actually afford that apartment with the floor-to-ceiling windows or if you're stuck with the one overlooking the dumpster. Honestly, figuring out 30 and hour is how much a year isn't just about multiplying a couple of numbers on your phone's calculator and calling it a day.

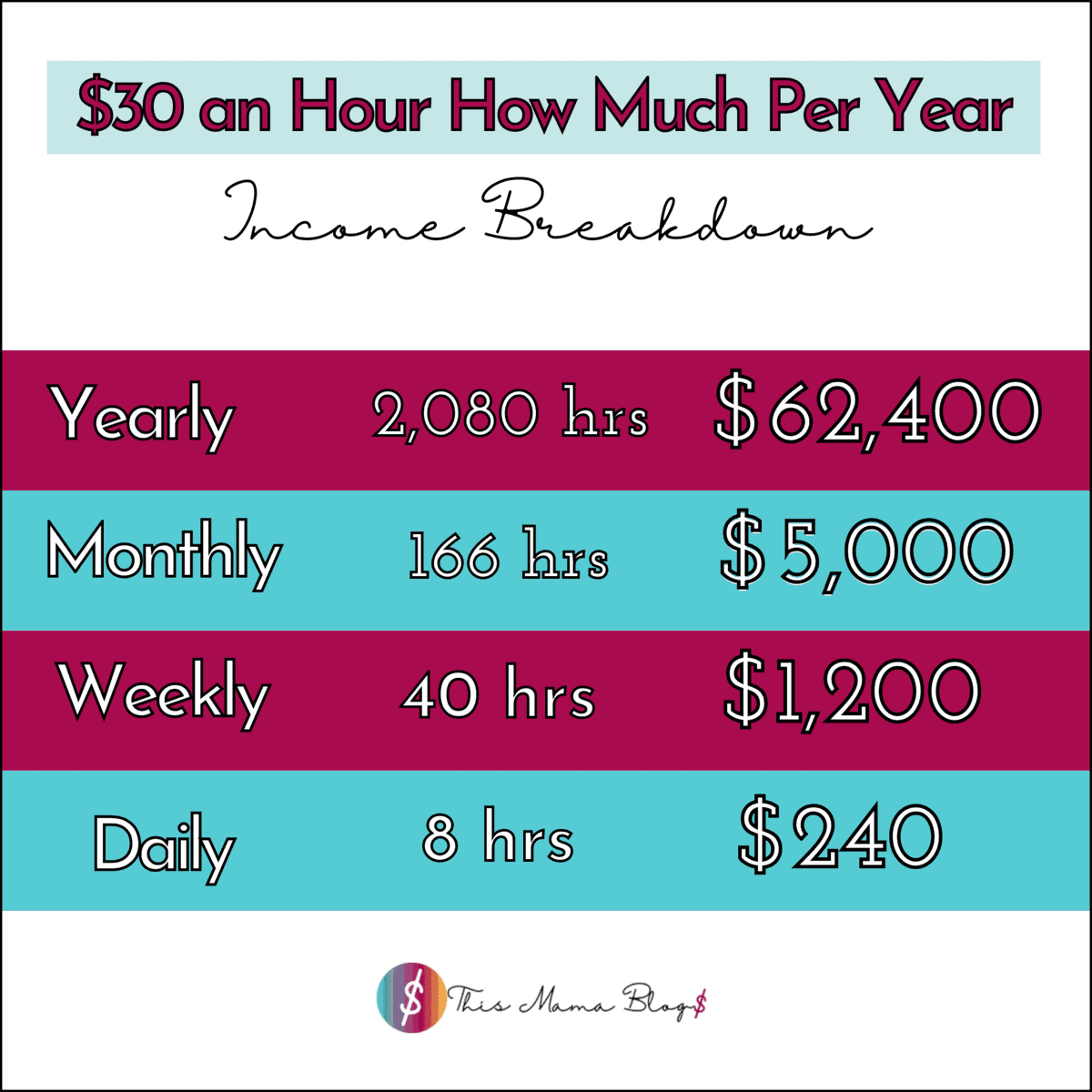

Most people just do the "standard" math. They take 40 hours, multiply by 52 weeks, and get $62,400. Boom. Done. Except, life isn't a math textbook. Unless you're a robot that never gets sick, never takes a vacation, and somehow dodges the IRS, that $62,400 is a total fantasy.

The Raw Math vs. Reality

Let's break the numbers down for a second. If you’re working a standard 40-hour week, you’re looking at $1,200 a week before anyone touches it. Monthly, that’s about $5,200. It looks great on paper. But here’s the kicker: how many of us actually work 2,080 hours a year?

In 2026, the calendar is a bit of a weird one. We've got 261 weekdays. If you work every single one of those, you're actually at 2,088 hours. That extra day is a nice little $240 bonus if you're hourly. But then you have to account for the 11 federal holidays. If your boss doesn't pay for those, you’re suddenly down to 250 work days. That brings your "real" gross income down to $60,000 flat.

It’s a big swing.

Then there's the "unpaid" stuff. Think about it. Do you get paid for your lunch break? Most people don't. If you're at the office for nine hours but only getting paid for eight, that hour of your life is basically a donation to the corporate gods. If you only work 37.5 hours a week—which is super common in some industries—your yearly total drops to $58,500. Still decent, but $4,000 less than that "calculator" result you saw online.

The Tax Man Cometh (And He’s Greedy)

Let’s talk about the elephant in the room: taxes. You never actually see $62,400. Not even close. For the 2026 tax year, the IRS has shifted the brackets again to account for inflation. If you’re filing as a single person, a big chunk of your income is going to fall into the 12% federal bracket, but you’ll also be brushing up against that 22% line once you cross the $50,400 threshold.

Don't forget FICA. That’s 7.65% right off the top for Social Security and Medicare.

Basically, by the time the federal government, your state (unless you're lucky enough to live in a place like Florida or Texas), and maybe even your city take their cut, your "take-home" is going to look a lot different. In a mid-tax state like Illinois or New York, you might only be pocketing around $46,000 to $48,000. That’s roughly $3,800 to $4,000 a month.

Suddenly, that $5,200 a month dream feels a bit more like a $3,900 reality.

📖 Related: All Car Brand Logos Explained: What Most People Get Wrong

Can You Actually Live on 30 an Hour?

This is where things get really subjective. If you're living in Wichita, Kansas, $60k a year makes you feel like royalty. You can get a nice place, eat out at that steakhouse everyone likes, and still have money for a hobby. But try doing that in San Francisco or Manhattan.

According to 2026 cost of living data, an equivalent lifestyle to $60,000 in a mid-sized city would require over $88,000 in New York City just to keep up. Housing is the absolute budget killer here. The old rule of thumb is that you shouldn't spend more than 30% of your gross income on rent. At $30 an hour, that means your rent ceiling is about $1,560.

Good luck finding a one-bedroom for $1,500 in Seattle or San Diego right now. You’re likely looking at roommates or a very long commute.

The Lifestyle Creep Factor

There’s this thing that happens when you move from, say, $20 an hour to $30. You start thinking, "Hey, I can afford the better coffee," or "I'll just Get DoorDash tonight." It's dangerous. Because while 30 and hour is how much a year seems like a lot, it’s also the "danger zone" of income. It's enough to feel comfortable, but not enough to be careless.

One major car repair or a surprise dental bill can wipe out a month of savings at this level if you aren't careful. It’s the middle-class trap. You make too much for any kind of government assistance or subsidies, but not enough to ignore the price of eggs.

Maximizing the 30-an-Hour Life

If you want to make this wage work for you, you’ve gotta be smarter than the average bear. It's not just about the hourly rate; it's about the benefits.

- The 401(k) Match: If your company offers a 3% match, that’s an extra $1,800 a year of free money. It effectively raises your "hourly" rate without you doing anything.

- Health Insurance Premiums: If you have to pay $400 a month for a crappy high-deductible plan, your $30 an hour is actually more like $27.50.

- Overtime: This is the secret weapon. If you're non-exempt and you can pull just five hours of "time and a half" a week, you're looking at an extra $225 weekly. Over a year, that adds nearly $11,000 to your gross.

Next Steps for Your Budget

Don't just trust the $62,400 figure. Sit down and look at your specific situation. Check your state's tax rates for 2026. Look at your commute costs.

The first thing you should do is pull your last three bank statements. Highlight every "fixed" cost—rent, car, insurance, phone. If those add up to more than $2,500, that $30 an hour is going to feel very tight. You might need to look at a side hustle or, better yet, negotiate for a higher "total compensation" package that includes things like transit passes or remote work days to save on gas.

Knowing exactly where your money goes is the only way to make $30 an hour feel like the "good" wage it’s supposed to be.