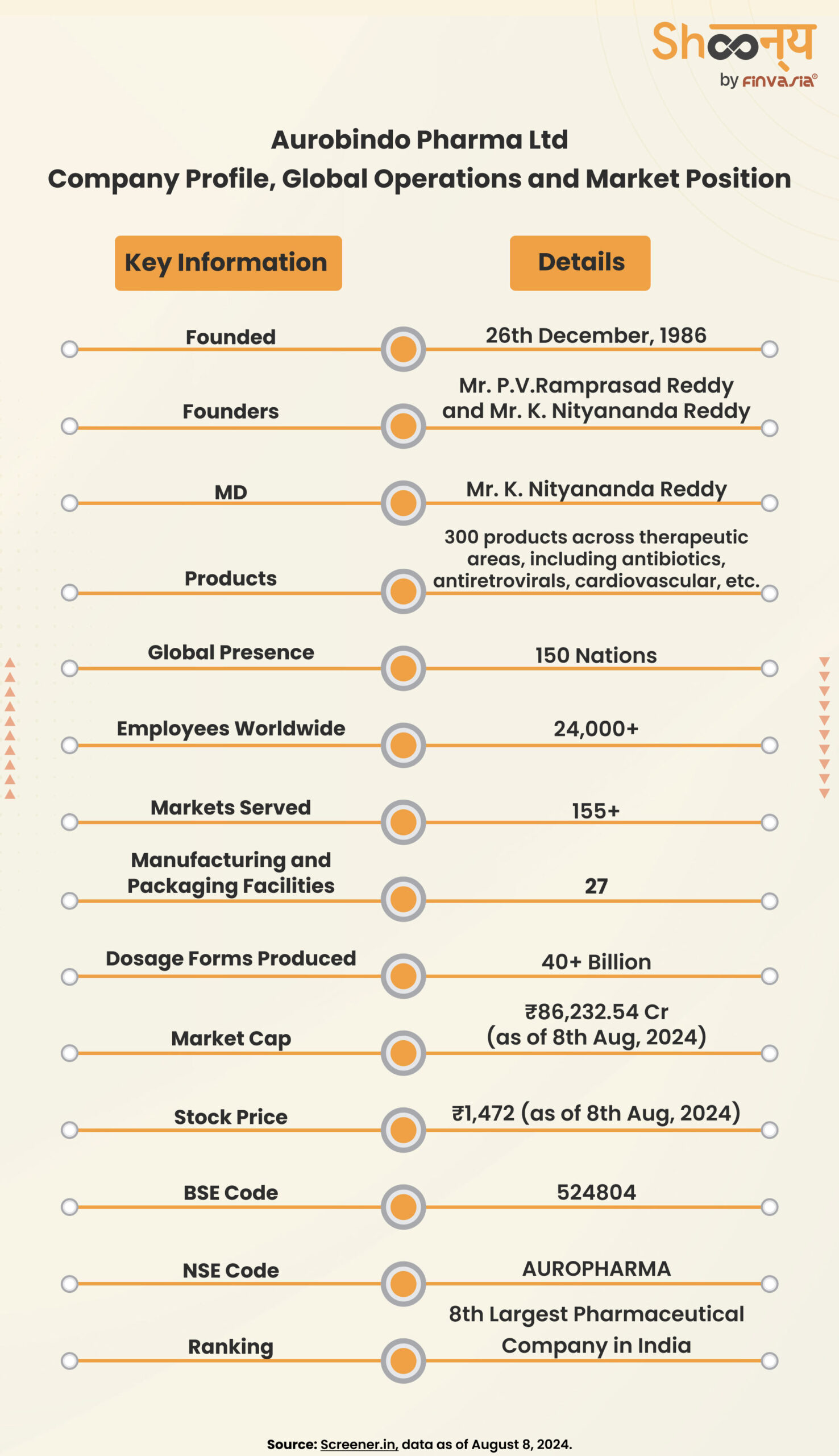

Today, January 16, 2026, the market is giving Aurobindo Pharma a bit of a cold shoulder. If you're looking at the ticker, you'll see the price hovering around ₹1,166.30 on the NSE. That's a drop of about 1.17% from yesterday's close.

Volatility is the name of the game right now.

Honestly, the stock has been playing a game of tug-of-war all day. It opened at ₹1,174.20, peaked at ₹1,195.50 when things looked optimistic in the morning, and then slid down to a low of ₹1,166.30 as the afternoon session wore on. Volume is decent, sitting at over 900,000 shares, but it doesn't feel like a "breakout" day. It feels like a "wait-and-see" day.

👉 See also: Price of Johnson & Johnson stock: Why the Market is Finally Paying Attention

Why the Market is Acting This Way

You've got to look at the context. We are literally weeks away from the Q3 FY26 earnings release, which is expected around early February. The company actually closed its trading window on January 1st. This is standard procedure, but it always makes the market a little twitchy.

Investors are basically holding their breath.

There's also a lot of "noise" from recent deals. Just a couple of weeks ago, on New Year's Day, Aurobindo's subsidiary Auro Pharma wrapped up a ₹325 crore acquisition of Khandelwal Labs' non-oncology business. It was a straight cash deal. No equity, no fuss, just a slump sale to grab 23 brands. The market liked it at first because it boosts their domestic presence in pain management and anti-infectives. But now? Now the "acquisition high" has worn off, and everyone is checking the math on how soon that ₹113 crore revenue from Khandelwal will actually impact the bottom line.

The Technical Struggle

Technically, the stock is kind of in a "no man's land." Short-term and long-term moving averages are giving off sell signals.

It’s frustrating for bulls.

The long-term average is sitting stubbornly above the short-term one. If the price can't break past the ₹1,202 resistance level, it might just keep drifting. Support seems to be holding around ₹1,155, so there's a floor, but it’s a shaky one.

What’s Actually Happening Under the Hood

Aurobindo isn't just a generic drug maker anymore. They are the largest generics company in the US by volume, but that’s a crowded room. To stay relevant in 2026, they've been pivoting hard toward complex products.

🔗 Read more: 1 680 000 VND to USD: What You Actually Get After Fees and Inflation

We’re talking biosimilars and specialty injectables.

In their last big update, management pointed out that while US pricing erosion has neutralized (thank goodness), they are spending way more on R&D—roughly ₹50 crore more than previous cycles. This is for the "high-growth" stuff. They also just commercialized a massive plant in China that’s expected to start pumping revenue into the books this year.

Analyst Split: Buy or Run?

If you ask ten analysts, you'll get twelve opinions.

- The Bulls (PhillipCapital, Geojit): They see a target price as high as ₹1,450 to ₹1,540. Their logic is simple: the China plant plus the Khandelwal acquisition equals a much stronger 2026.

- The Bears (Macquarie, Kotak): They’ve issued "Sell" ratings with targets down near ₹1,050 to ₹1,115. They worry about the high R&D spend and the fact that revenue growth has been stuck in the 4–6% range lately.

It’s a classic value vs. growth debate. Aurobindo’s P/E ratio is currently around 19.8x. Compared to peers like Divi's Labs or Torrent Pharma, which trade at much higher multiples, Aurobindo looks "cheap." But it's cheap for a reason—investors are waiting for that massive manufacturing capacity to finally turn into massive profits.

✨ Don't miss: Idaho Income Tax Calculator: Why Your Take-Home Pay Might Surprise You

What to Watch Next

Don't just stare at the daily chart. That’s a recipe for a headache.

The real test comes with the Q3 results in February. Watch the "EBITDA before R&D" margin. In the last report, it was a healthy 25.8%, but the net profit was a bit lower due to higher operational costs. If they can show that the Khandelwal integration is seamless and the China facility is scaling, the sentiment will flip fast.

Also, keep an eye on the Swarnaakshu Solar project. They just extended the timeline to March 31, 2026, to finish that 26% stake acquisition. It’s a move toward "captive" power (making their own energy), which helps margins in the long run.

Actionable Insights for Investors

If you're holding or thinking about buying, here's the reality check:

- Mind the Resistance: Don't chase the stock if it's hitting its head against the ₹1,200–₹1,205 ceiling unless there's high volume.

- The February Pivot: Expect high volatility leading up to the earnings announcement. If you're a conservative investor, waiting for the post-earnings commentary might be safer.

- Domestic Shift: Watch how they use the new 1,600+ stockists gained from the recent acquisition. If domestic growth outpaces the 7–9% industry average, that’s your green flag.

- Stop-Loss Logic: Technical analysts are suggesting a stop-loss around ₹1,093 to protect against a broader market slide.

Aurobindo is a giant in transition. It's moving from "plain vanilla" generics to complex, high-margin medicine. That transition is messy, expensive, and slow. But for those who believe the 2026 China revenue and domestic expansion will pay off, today's dip is just another Tuesday in the pharma world.

Next Steps:

Check the NSE/BSE volume trends in the final 30 minutes of trade today to see if institutional "delivery" buying is happening. Review the company's December 31 disclosure regarding the trading window closure to confirm the exact date for the upcoming Board Meeting, as this will be the primary catalyst for the next major price swing.