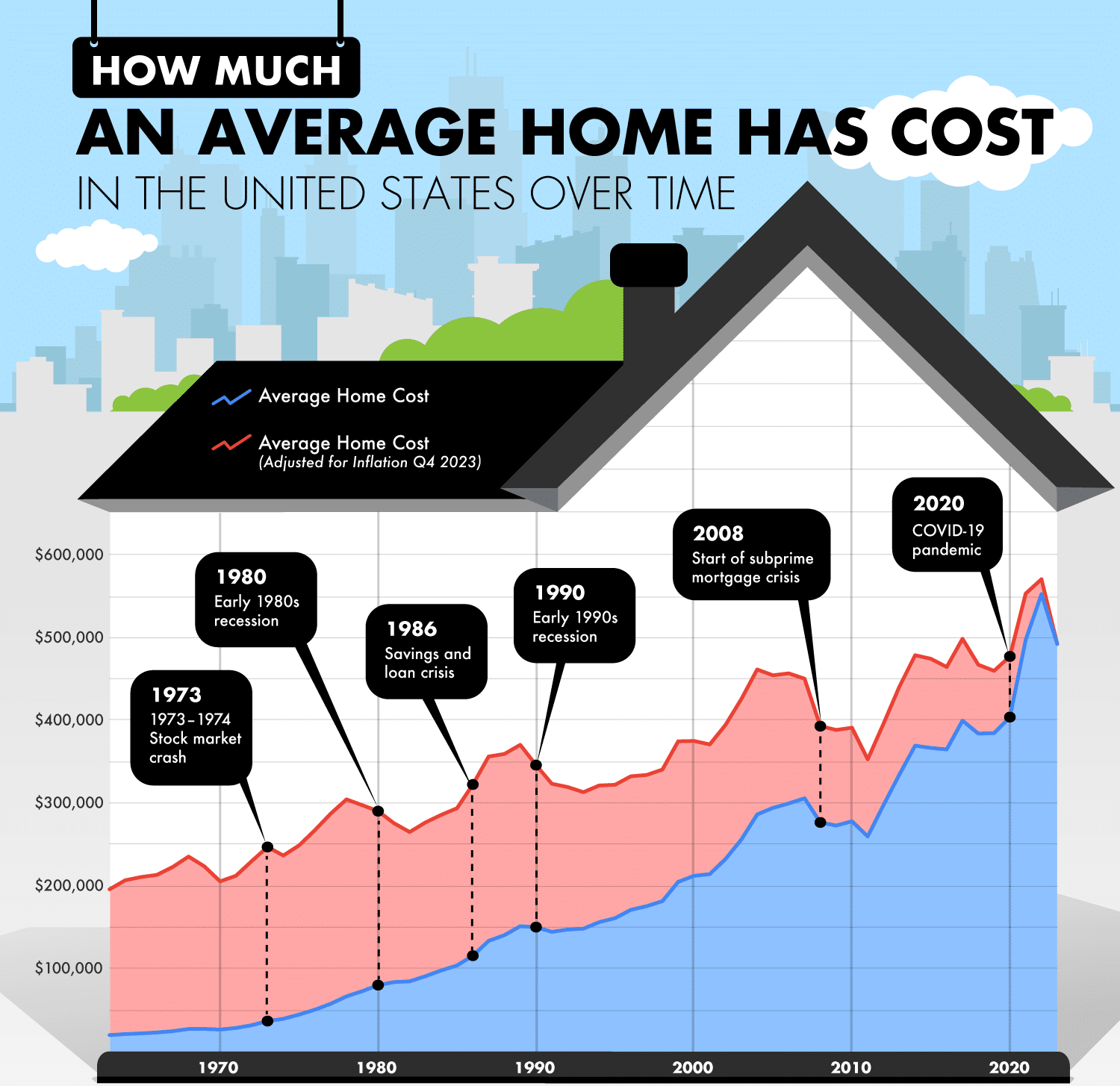

Honestly, the housing market in 2026 is a weird beast. If you've been doom-scrolling through real estate TikToks, you probably think the world is ending or that a $200,000 house is a mythical creature like a unicorn. It's not. But the gap between "I can afford this" and "I need to sell a kidney" has never been wider depending on where you stand on a map.

Most people look at the national average—which is hovering around $512,800 for the average sales price—and they just give up. Big mistake. National numbers are basically useless for your actual life. They’re skewed by those $15 million glass boxes in Malibu and the penthouses in Manhattan.

When you break down the average cost of homes by state, you start to see the "haves" and "have-nots" of the American economy. Some states are cooling off after a wild five-year run, while others are just starting to heat up as people flee the expensive coasts.

The Reality of Six-Figure Differences

The spread is staggering. You could literally buy four houses in West Virginia for the price of one modest single-family home in Hawaii. That isn't hyperbole; it’s the math.

As of early 2026, Hawaii remains the king of "How do people live here?" with a median home value pushing $977,000. It’s followed closely by California at roughly $906,500. If you’re looking at these states, you aren't just buying a house; you’re paying a massive "sunshine and scenery" tax.

On the flip side, the Midwest and parts of the South are still the last bastions of the sub-$300k home. West Virginia is currently the most affordable state in the union, with an average cost of homes sitting around $225,500.

Why the Gap is Widening

It isn't just about demand. It's about how much it costs to actually put a nail in a piece of wood. In places like Massachusetts (median $702,400) or Washington ($690,100), strict zoning laws and high development fees mean builders can’t just "whip up" affordable housing.

👉 See also: US China Trade Tariffs Explained: What Most People Get Wrong in 2026

Then you have the tech factor. Washington’s prices are high because the people buying them often have stock options that look like phone numbers. Meanwhile, in Mississippi ($235,400) or Arkansas ($239,600), the local economy doesn't support those $800k price tags, so the market stays grounded.

Average Cost of Homes by State: The 2026 Breakdown

Forget the tidy tables for a second and let's look at the regional "vibes" because that’s how people actually move.

The Northeast "Sticker Shock"

If you're in New England, I have bad news. Inventory is still tight. Massachusetts is sitting at a median of $702,400. Even Connecticut, which used to be the "affordable" alternative to New York, has seen prices jump to about $523,600. Why? Because people realized they could live in a cute town and commute to a high-paying city job only twice a week.

The Cooling Sunbelt

Here is a surprise: Florida and Texas are actually chilling out. After the post-pandemic frenzy, Florida home prices have actually dipped in some spots, like Cape Coral, where prices dropped by about 10%. The average Florida home is around $436,600 now. It’s still pricey, but the "multiple offer" madness has died down.

The Mid-Market Heroes

States like Georgia ($398,400) and North Carolina ($380,000-ish) are where the middle class is currently congregating. They offer a balance—you get a yard and a decent school district without needing to be a venture capitalist.

What Everyone Gets Wrong About Affordability

The "sticker price" is a lie. Well, it’s not a lie, but it’s only half the story.

✨ Don't miss: Zee Enterprise Share Price: What Most People Get Wrong

You might see that Indiana has an average cost of homes around $255,000 and think, "I'm moving tomorrow!" But you have to look at the price-to-income ratio. Danielle Hale, chief economist at Realtor.com, points out that while home prices might rise 2.2% this year, wages in some states are rising faster.

This means that in "real terms," housing is actually getting slightly more affordable in specific pockets.

The Mortgage Rate Trap

Don't wait for 3% interest rates. They aren't coming back. Expert consensus from the NAR and MBA suggests that for 2026, the 30-year fixed rate will hover between 6% and 6.4%.

"2026 is the year of small wins," says Kara Ng from Zillow. "We're seeing a more balanced market where not every seller gets exactly what they want."

This shift is huge. In 2021, if you asked for a home inspection, the seller would laugh you out of the room. In 2026, buyers actually have some leverage. You can ask for repairs. You can haggle on the closing costs. That effectively lowers your "true cost" even if the average cost of homes by state remains high.

Hidden Costs: Taxes and Insurance

Let's talk about the "vampire" costs that suck your bank account dry after you buy.

New Jersey might have a median home price of $427,600 (which sounds okay compared to CA), but the property taxes are brutal—often over $9,500 a year. Contrast that with West Virginia, where the median annual property tax is roughly $835.

📖 Related: UPS Seasonal Delivery Driver: Is the Peak Season Paycheck Actually Worth It?

Then there’s insurance. If you’re looking at coastal states, your insurance premiums might have doubled in the last two years. In some parts of Florida or Louisiana, the cost of insuring the home is becoming a bigger hurdle than the mortgage itself.

Where the Smart Money is Moving

The new "hot spots" for 2026 aren't the ones you’d expect.

- Idaho: It's the #1 hottest market right now. Even with a median price of $505,300, people are flocking there for the lifestyle.

- Hartford, Connecticut: Zillow predicts this will be one of the strongest growth markets this year.

- The "Affordability" Kings: South Carolina, Delaware, and Utah are seeing massive influxes of buyers who are tired of the $800k price tags in their home states.

Is California Really "Cold"?

Technically, yes. California's market is labeled "cold" not because nobody wants to live there, but because the prices have hit a ceiling. When the average house is $900,000, you run out of people who can actually buy them. We're seeing slight price declines there (around -0.6%), which is a healthy correction, not a crash.

Actionable Steps for 2026 Buyers

If you’re looking at the average cost of homes by state and feeling overwhelmed, take a breath. The market is finally stabilizing.

- Look at the "Price-to-Income" ratio, not just the price. A $400k home in a high-wage state might be "cheaper" than a $250k home in a state with no jobs.

- Target the "Cooling" markets. Florida and Texas have more inventory right now. More inventory = more power for you to negotiate.

- Check the taxes. Before you fall in love with a house, look up the 2025 tax assessment. It can change your monthly payment by hundreds of dollars.

- Don't time the rates. If you find a house that fits your budget at 6.2%, buy it. You can always refinance later if rates drop to 5.5%, but you can't "refinance" a purchase price that went up while you were waiting.

The 2026 housing market isn't the Wild West anymore. It's a slow, steady climb. Whether you’re eyeing a $225k starter home in the Appalachians or a $700k colonial in Mass, the key is knowing that the "average" is just a starting point. Your local reality is what actually matters.

Keep an eye on regional inventory levels. In the South and West, where they’re actually building new houses, you’ll find more "haves." In the Northeast and Midwest, where inventory is stagnant, expect prices to stay stubborn. Real estate is, and always will be, a game of geography.

Next Steps for Your Search

- Calculate your debt-to-income ratio to see how much of a mortgage you can actually carry at 6.3% interest.

- Research property tax rates for the specific counties you are considering, as these vary wildly even within a single state.

- Get a pre-approval now to lock in a rate, but keep an eye on the weekly Freddie Mac updates as the Fed continues its cautious 2026 policy.