Money is a weird subject in America. We’re obsessed with it, yet we barely talk about the actual numbers. You might see a headline about the stock market hitting a record high and think everyone is getting rich. Or you hear about a "middle-class squeeze" and assume the sky is falling. Honestly, the reality is somewhere in the messy middle.

If you’re trying to figure out where you stand, looking at the average household income in the united states is the first step, but it’s also a bit of a trap.

The numbers look good on paper. According to the most recent U.S. Census Bureau data released in late 2025, the real median household income in 2024 was $83,730. That’s the "middle" point. Half of the country makes more, half makes less. If you look at the average (the mean), that number jumps way up to around $121,000.

Why the massive gap?

Simple. The ultra-wealthy. When a handful of billionaires walk into a room, the "average" income of everyone in that room skyrockets, even if most people there are struggling to pay rent. That’s why the median—that $83,730 figure—is a much better yardstick for your life.

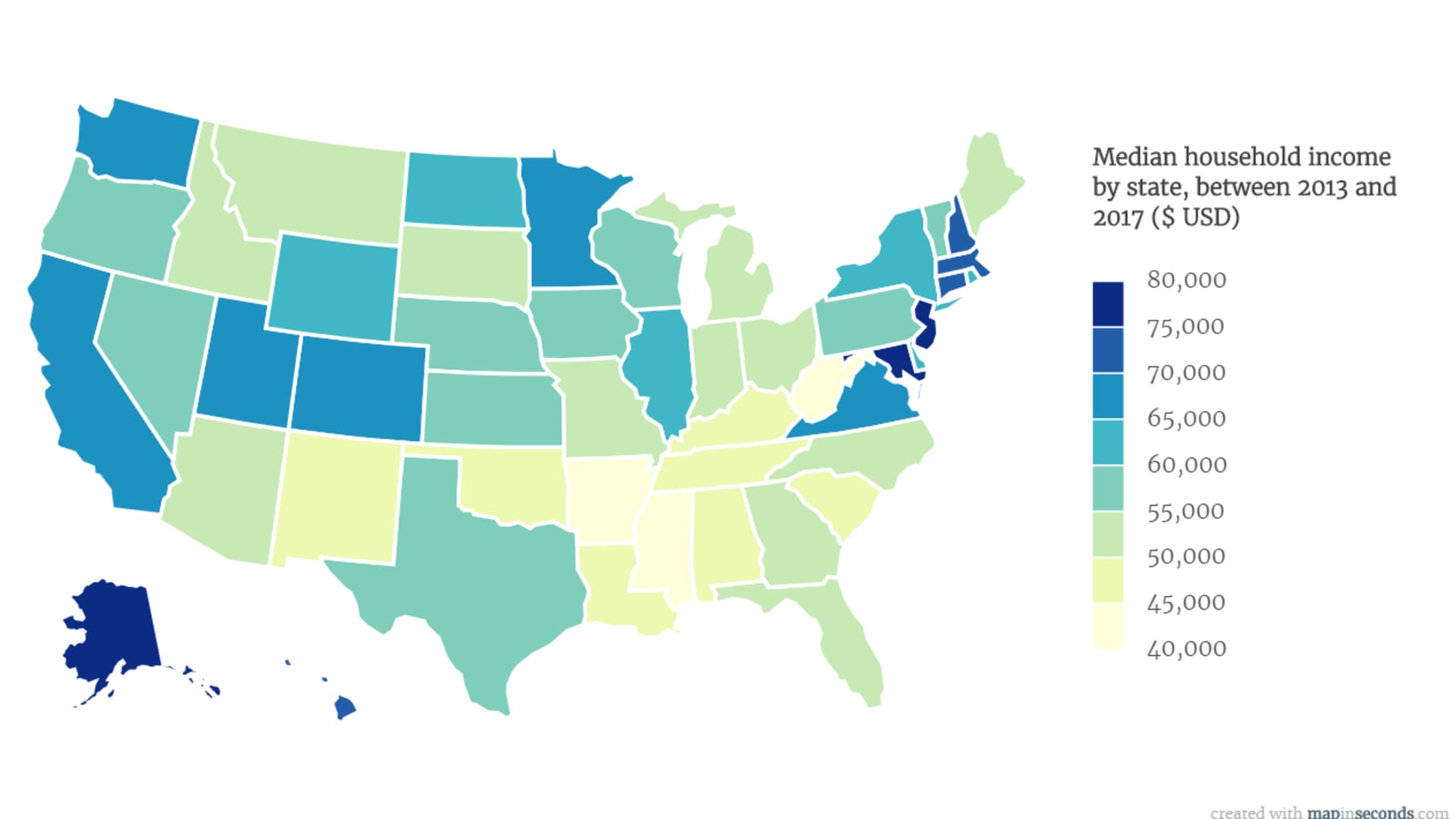

The Great Geography Gap

You can't talk about income without talking about where you park your car at night. A $100,000 salary in Jackson, Mississippi, makes you a local mogul. In San Francisco? You’re probably looking for a roommate.

The coastal divide is real. In 2024, the median household in the San Jose-San Francisco-Oakland area brought in $125,105. Meanwhile, in places like the Middlesborough-Corbin area of Kentucky, that number plummeted to $46,740.

That is a staggering difference.

It's not just "coastal elites" vs. the "heartland," either. Even within states, the variance is wild. You’ve got tech hubs like Austin or the Research Triangle in North Carolina pulling the state averages up, while rural counties just a two-hour drive away are seeing stagnant wages.

Top Earning States (Median)

- Massachusetts: $99,858

- New Jersey: $99,781

- Maryland: $98,678

- California: $100,149 (Crossing that $100k threshold finally)

On the flip side, states like Mississippi, West Virginia, and Arkansas still hover in the $59,000 to $62,000 range. It feels like two different countries sometimes.

What Does "Middle Class" Even Mean Anymore?

Middle class used to mean a house, two cars, and a vacation. Now? It’s a moving target.

Researchers at the Pew Research Center typically define "middle class" as those earning between two-thirds and double the national median. For 2025 and heading into 2026, that range is basically $56,600 to $169,800.

But wait.

If you live in Arlington, Virginia, you might need to earn at least $93,470 just to get your foot in the "middle class" door. In Detroit, you could technically be considered middle class starting at $25,384. It feels wrong, doesn't it? But that’s what the data says.

📖 Related: Why Your First Aid Kit for Office Is Probably Expired and Useless

The "upper-middle class" is an even more elusive beast. In 2026, experts from firms like Nasdaq suggest you need to be pulling in between $117,000 and $150,000 to be in that top 20% of the middle-income bracket. If you're in Maryland, make that $158,126.

The Education Premium is Real (But Expensive)

We’ve all heard the "college is a scam" discourse. While student debt is a nightmare, the Census data shows a brutal reality: degrees still pay.

In the first half of 2025, the median annual wage for someone with a Bachelor’s degree was roughly $83,356. If you had an advanced degree? You were looking at $101,972. Compare that to a high school graduate earning $49,556 or someone without a diploma making $38,636.

It’s a $44,000 annual gap between the bottom and the top of the educational ladder. Over a 40-year career, that’s nearly $1.8 million.

But there's a catch. Healthcare. A report from the Center for Economic and Policy Research found that the typical working family spent nearly $4,000 on healthcare in 2024. For those in the bottom income tier, about 22% of them are spending more than 10% of their total income just on doctors and insurance.

The Demographic Divide

Income isn't just about what you do; it’s often about who you are. The 2025 Census report highlighted some uncomfortable trends.

Asian households continue to lead the pack with a median income increase of 5.1% recently. Hispanic households also saw a jump of 5.5% to about $70,950. However, Black households saw a decline of 3.3% in the same period.

And the gender pay gap? It’s still there. In 2024, the female-to-male earnings ratio actually fell to 80.9%, down from 82.7% the year before. Men earned a median of $71,090 while women took home $57,520. That’s the second year in a row the gap has widened, which is definitely not the direction we wanted to see.

✨ Don't miss: Why Most People Ignore the Evacuation Assembly Area Sign (And Why That Is Dangerous)

Inflation: The Silent Pay Cut

You got a 4% raise? Congrats! Oh, wait. Inflation was 3%. You basically got a 1% raise.

This is what economists call "real" income. The average household income in the united states might be going up in raw dollars, but "real" median income—which is adjusted for the cost of eggs, gas, and rent—has been relatively flat.

Heather Long, a chief economist, recently pointed out that middle-class Americans are frustrated for a reason. Between a frozen job market in early 2025 and the rising cost of everyday items, the "growth" people see on their paychecks is being eaten alive by the local grocery store.

Actionable Insights: What Do You Do With This?

So, the national numbers are $83k median and $121k average. Now what?

Don't compare yourself to a national average. It's useless. Instead, look at your "local" median. If you're in a high-cost area like Massachusetts or California, you need to be aiming for that $100k mark just to be "average."

Check your quintile. The bottom 20% of households average $18,460. The top 20% average $316,100. If you are in the "middle 20%," you’re averaging around $84,390. Knowing which bucket you fall into helps you understand your tax burden and what kind of government assistance or investment strategies might actually apply to you.

📖 Related: Hamer v. Sidway: Why the Case of the Nimble Nephew Still Dominates Law School

Account for the "Benefit Gap."

Income is just the cash. Don't forget to factor in your health insurance premiums and 401(k) matches. A $70,000 job with great benefits is often worth more than an $85,000 "1099" gig where you pay for everything yourself.

Negotiate based on the 80.9%.

If you're a woman in the workforce, know that the current trend is technically moving against you. Use the $57,520 vs. $71,090 median split as fuel for your next salary review. The data shows the gap is widening, so being aggressive about your "real" value is more important now than it was two years ago.

Move or Pivot?

If you’re in a state like Mississippi where the ceiling is lower, but your skills are remote-capable, "geo-arbitrage" is your best friend. Earning a Denver salary ($106k) while living in a lower-cost area is the fastest way to move from the middle class to the upper-middle class without actually changing your job.

The average household income in the united states is a story of two Americas. One is growing, educated, and coastal; the other is working harder just to stay in the same place. Knowing the real numbers is the only way to make sure you aren't the one getting left behind.