Money is weird. We talk about it constantly but rarely get the numbers right, especially when we start throwing around terms like "average" and "median" at the dinner table. If you've ever felt like your paycheck is vanishing into a black hole while the news says the economy is booming, you aren't alone. Honestly, the way we measure the average household salary in us is kinda broken if you don’t know how to read between the lines.

Most people use "average" when they really mean "typical." But in a country with over 130 million households, the typical experience is a world away from the mathematical average.

The Math vs. The Reality

Let’s get the dry stuff out of the way first. According to the U.S. Census Bureau’s latest data release in late 2025, the real median household income in the United States sits at approximately $83,730.

Wait. Why did I say median instead of average?

Because the actual average—the mean—is way higher, hovering around $121,000. That massive gap exists because a tiny sliver of the population makes so much money it drags the entire mathematical average upward. Think of it like a bar where ten people earn $50,000 a year, and then Elon Musk walks in. Suddenly, the "average" person in that bar is a billionaire. But nobody’s bank account actually changed.

The median is the true "middle." It means half of American households make more than $83,730, and half make less. If you’re trying to figure out where you stand, the median is your North Star.

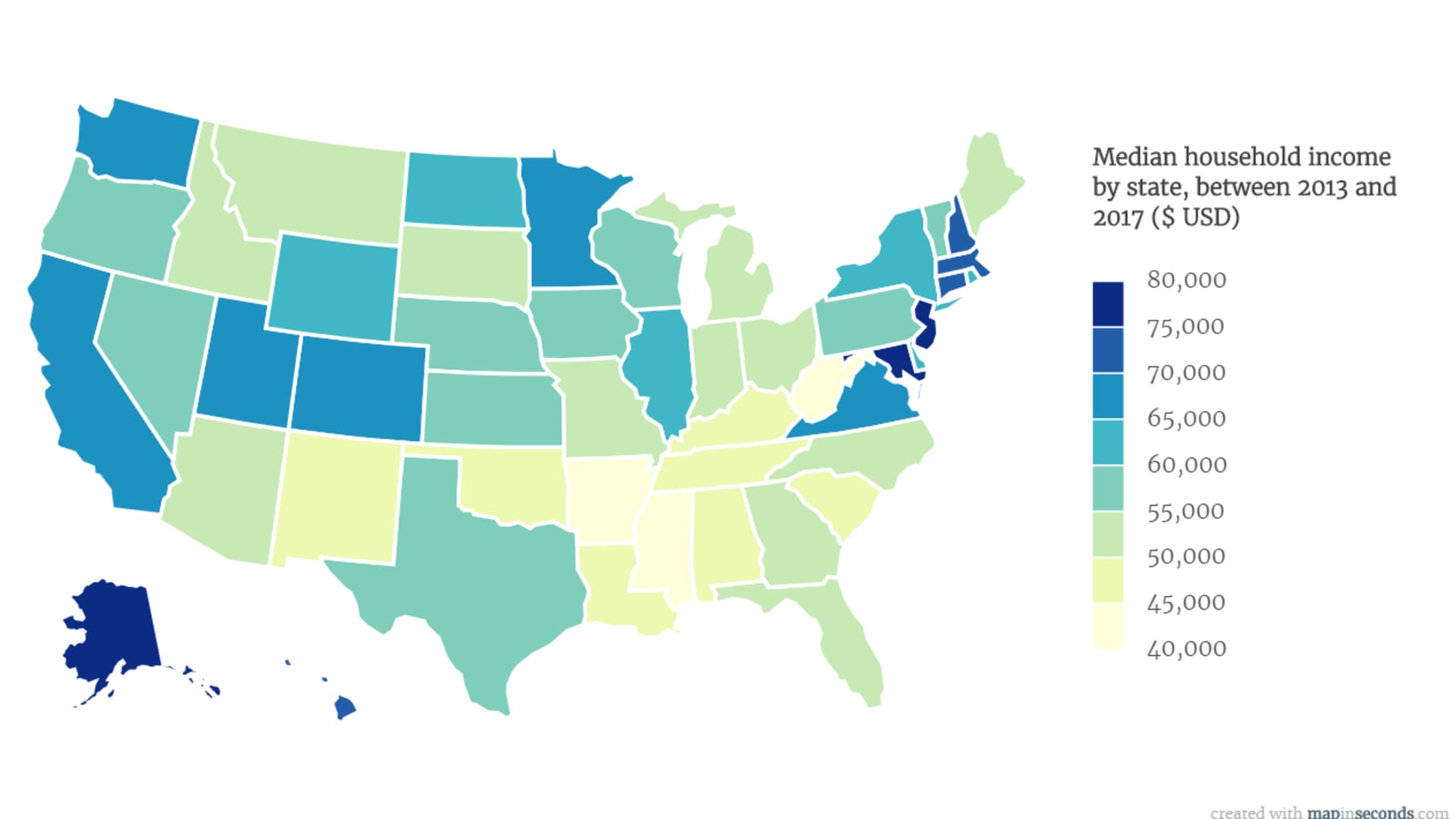

Geography is the Great Income Divider

You’ve probably heard people say $100k isn't what it used to be. In some places, that's an understatement.

If you’re living in the San Jose-San Francisco-Oakland area, the median household income is a staggering $125,105. You might feel rich on paper, but after you pay $4,000 for a two-bedroom apartment that smells like old gym socks, you're basically broke. Compare that to somewhere like the Middlesborough-Corbin area in Kentucky, where the median drops to around **$46,740**.

It’s a bizarre paradox.

A family in Mississippi—the state with the lowest median income at roughly $59,100—might actually have more "breathing room" than a family in Massachusetts making $104,800. Why? Because the cost of living doesn't just scale; it explodes. SmartAsset’s 2025 study points out that to live "comfortably" as a single adult in Hawaii, you need to clear $124,467. Meanwhile, in West Virginia, you can hit that same comfort level with about $80,829.

📖 Related: eBay Black Friday 2024: What Actually Happened and Why the Refurbished Math Changed Everything

The Top Earners by State (Median)

- Massachusetts: ~$104,800

- New Jersey: ~$102,900

- Maryland: ~$109,000 (for 2-person households)

- California: ~$99,900 (for 2-person households)

On the flip side, states like Arkansas and West Virginia frequently see numbers closer to the $55,000 mark. It’s not just a different zip code; it’s a different economic universe.

The "Middle Class" is Getting Crushed by a Specific Ratio

The most terrifying stat isn't the average household salary in us itself. It’s the home-price-to-income ratio.

Historically, a "healthy" ratio was about 2.6. That meant a house cost about 2.6 times your annual salary. In the 90s, we were around 3.2. Today? The national median single-family home price has surged to five times the median household income. In San Jose, it’s twelve times.

You can’t out-earn that kind of growth with a 3% annual raise.

This is why people feel like they’re falling behind even when their salary goes up. Between 2019 and 2024, home prices jumped nearly 48%, while median income only rose by about 22%. The math just doesn't add up for first-time buyers.

Demographics and the Hidden Gaps

We also need to talk about who is actually seeing these gains.

Asian and Hispanic households saw the most significant bumps in 2024 and 2025, with Hispanic median income rising 4.3% compared to pre-pandemic levels. However, Black households actually saw a slight decline of about 3.3% in recent estimates.

Gender still plays a massive role too. The median male earner in 2024 brought home $71,090, while the median female earner made $57,520. That’s an 80.9% ratio. It’s actually been dropping for two years straight, which is a bit of a gut punch for anyone who thought the gap was closing for good.

And then there’s the "Married Couple" advantage. If you’re married, your median household income is significantly higher than any other demographic. Two incomes are no longer a luxury; they are the baseline for survival in most major American metros.

Why the "National Average" is Sorta Useless to You

If you’re looking at these numbers to judge your own success, stop.

The average household salary in us includes everyone. It includes the 22-year-old barista in Seattle, the 85-year-old retiree in Florida on a fixed pension, and the mid-career software engineer in Austin.

A better metric for most working adults is to look at full-time, year-round workers. If you work 40+ hours a week, the median earnings are usually much higher than the "household" median because household stats include people working part-time or not working at all. For instance, a college-educated male working full-time has a median earning closer to $90,000.

The 2026 Outlook: Moving Beyond the Number

Inflation has cooled, but prices didn't go back down. They just stopped rising so fast. This "new normal" means that a $83k salary in 2026 buys significantly less than it did in 2019.

People are getting creative. The "side hustle" isn't a trend anymore; it's a staple. Data from late 2025 shows more Americans taking on digital freelance work—coding, virtual assistance, content writing—to bridge the gap. Others are simply fleeing. We’re seeing a mass exodus from high-tax, high-cost states like California and New York toward "value" states like Tennessee, North Carolina, and Ohio.

Actionable Steps for Navigating Your Income

If you feel stuck below the median, or even if you're above it but feel broke, here is how you actually move the needle:

1. Calculate your Personal Price-to-Income Ratio

Don't just look at your salary. Look at your local housing market. If the houses in your area are more than 4x your household income, you are statistically likely to stay "house poor." You either need more income (side gig/promotion) or a different zip code.

2. Audit your "Post-Tax" Reality

The Census Bureau notes that while the pretax median is ~$83k, the median post-tax income is closer to **$72,330**. When you’re budgeting, use the post-tax number. Most people over-estimate their "wealth" because they forget the government takes its cut first.

3. Level Up via "Skills-Based" Earning

The highest growth in wages isn't coming from general degrees but from certifications. Cybersecurity, AI tool management, and skilled trades (HVAC, welding) are currently commanding salaries between $70k and $110k without the debt of a four-year degree.

4. Remote Work Arbitrage

If your job allows it, moving to a state where the "comfort" threshold is $80k while keeping a salary tuned for a $120k city is the fastest way to build wealth in the current economy.

The average household salary in us is a benchmark, not a destiny. Understanding that the "average" is skewed by billionaires and that the "median" is heavily influenced by where you live is the first step toward actually making sense of your own bank account.

Key Takeaways

- Median vs. Mean: The median ($83,730) is what most families actually experience; the average ($121,000) is skewed by the wealthy.

- The Housing Gap: Home prices are rising 2x faster than incomes, making the 2020s one of the hardest decades for buyers.

- State Stakes: You need almost $45,000 more per year to live comfortably in Hawaii than in West Virginia.

- Demographic Shifts: Hispanic and Asian households are seeing the fastest income growth, while the gender pay gap has slightly widened recently.

Stop comparing yourself to a national number that doesn't account for your city’s rent or your specific career path. Focus on your local median and your personal purchasing power. That's where the real truth lives.

To get a better handle on your situation, look up the "Cost of Living Index" for your specific city and compare it to the national baseline of 100. If your city is a 150, but your salary is only 10% above the national median, you're technically earning less than someone in a "cheaper" town. Adjust your career goals based on your local reality, not a Washington D.C. spreadsheet.