Honestly, walking into 2026 without Warren Buffett at the helm of Berkshire Hathaway feels a bit like watching the Bulls take the court without Jordan. It’s weird. But if you’re looking at the brk/b stock price today, you’ll notice the market isn't exactly in a blind panic, even if the "succession discount" is finally a real thing we have to talk about.

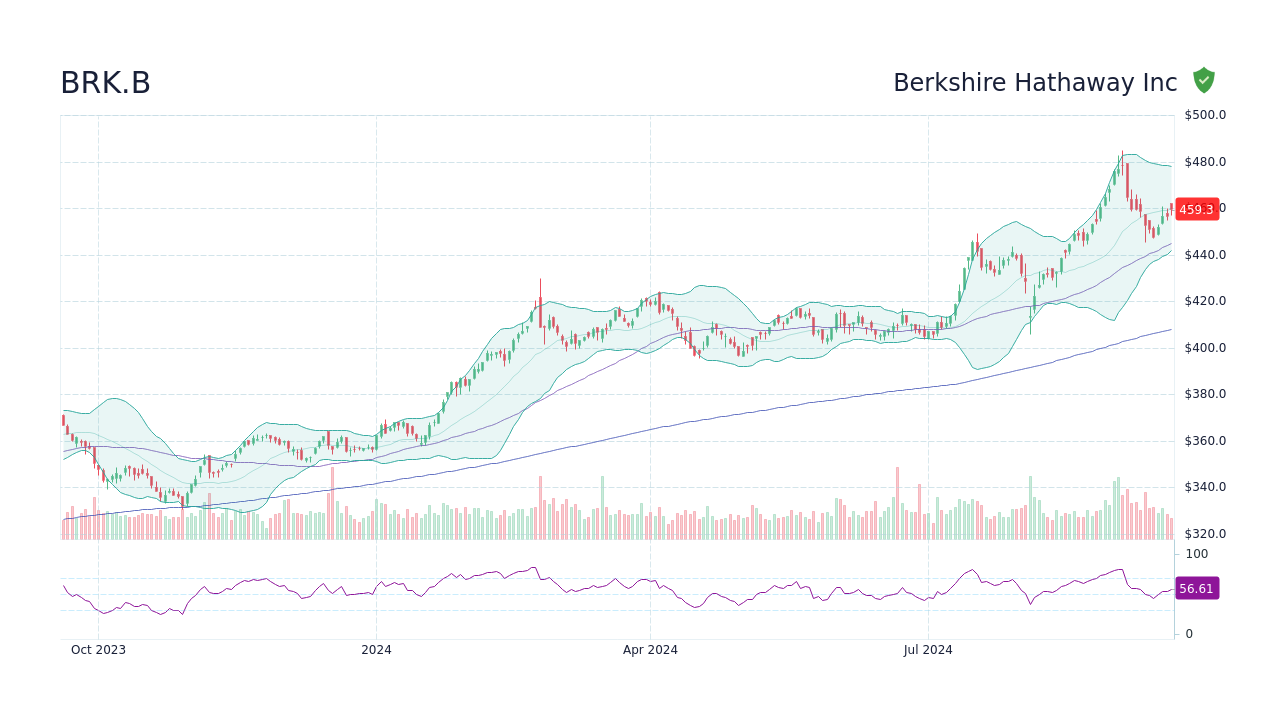

As of this Sunday, January 18, 2026, the markets are closed, but we’re chewing on Friday’s finish. Berkshire Hathaway Class B (BRK.B) wrapped up the week at $493.29. It’s been a choppy start to the year. Just a few weeks ago, we were flirting with $500, but the reality of Greg Abel taking the big seat on January 1st has investors acting a little skittish.

Succession isn't just a TV show; it's a billion-dollar math problem.

🔗 Read more: Hawaii Income Tax Calculator: Why Your Take-Home Pay Might Surprise You

The Reality Behind the BRK/B Stock Price Today

The stock is down about 10% since the formal retirement announcement last year. Some people call this a "crash," but let’s be real—it’s more of a recalibration. When you lose the world’s greatest capital allocator, the "Buffett Premium" evaporates. You’re left with the actual businesses.

And those businesses? They’re doing just fine.

Berkshire just closed a massive $9.7 billion deal for OxyChem (Occidental Petroleum’s chemical wing) on January 2nd. That’s a classic Abel move—industrial, cash-heavy, and unsexy. While everyone else is chasing AI startups with no revenue, Berkshire is out here buying chemical plants.

Why the $490 level matters

Technically, we're in a bit of a "no man's land." The 200-day moving average is sitting right around $497. We’ve dipped below it. For the chart junkies, that's a signal to pay attention. If the brk/b stock price today stays under that $497 mark, we might see it drift toward $480 before finding a real floor.

👉 See also: Why The Restaurant Store on Kane Street Is Still the Best Kept Secret in Baltimore

Analysts at Zacks currently have an average price target of $537.75. That’s about 9% upside from where we are sitting right now. Is that enough to get excited? Depends on your timeframe.

What's Changed with Greg Abel?

Greg Abel isn't trying to be a second Warren. He’s an operator. He’s the guy who made Berkshire Hathaway Energy a powerhouse.

One thing that’s basically the talk of Wall Street right now is the cash hoard. It hit a staggering $381.7 billion at the end of Q3. Think about that. They have more money than the GDP of several countries just sitting in T-bills.

There’s a growing rumor—and some credible analyst predictions from folks like Matt DiLallo—that 2026 might be the year Berkshire finally pays a dividend.

Imagine that.

The company that famously refused to return cash for decades might finally start cutting checks. Why? Because holding $380 billion in a falling-rate environment is a drag on returns. If Abel wants to win over the skeptics, a dividend is the fastest way to do it.

The Tech Shift

We also saw a quiet $4.9 billion buy into Alphabet (Google) recently. Buffett always stayed away from what he didn't understand, but Abel and the team (Todd Combs and Ted Weschler) seem more comfortable in the digital age.

- Geico is finally catching up on its tech stack.

- The BNSF Railway is leaning into automation.

- The insurance float is being deployed with a bit more of a "modern" lens.

Is It a "Buy" or a "Wait and See"?

The brk/b stock price today looks "cheap" on a Price-to-Earnings (P/E) basis—around 15.8x. That’s cheaper than the broader S&P 500.

But you have to account for the "Succession Discount."

Investors are worried that without Warren, the "magic" is gone. Gaurav Dalmia, a seasoned Berkshire watcher, recently compared this to Satya Nadella taking over Microsoft. Everyone thought Microsoft was dead money. They were wrong.

However, Berkshire isn't a software company. It's a massive, slow-moving conglomerate. It doesn't pivot; it drifts.

What to watch next

- The Q4 Earnings Call: This will be the first one without Buffett as CEO. The tone will matter as much as the numbers.

- Share Repurchases: Berkshire hasn't bought back its own stock in five quarters. If they start buying again at $490, that’s a massive "Buy" signal from the insiders.

- The Dividend Decision: If an announcement comes during the annual meeting in May, expect the stock to pop.

Actionable Steps for Investors

If you’re holding BRK.B, don't panic. The underlying assets—the railroads, the energy plants, the insurance businesses—are still printing money. The intrinsic value, according to some DCF models, is actually closer to $590.

If you’re looking to enter, keep an eye on that $489 support level.

If it breaks that, you might get an even better entry point. But honestly, trying to time a Berkshire entry is usually a fool's errand. You buy it because you believe in the "Fortress Berkshire" model.

💡 You might also like: Sysco Boston Explained: How the Plympton Hub Actually Keeps New England Restaurants Running

Check your portfolio's exposure to tech versus industrials. If you're too heavy on Nvidia and Microsoft, the brk/b stock price today offers a decent hedge. It’s a bet on the "boring" parts of the American economy that actually keep the lights on.

Set a price alert for $485. If it hits, look at the volume. If the selling is exhausted, that might be your window to pick up shares of a post-Buffett company that’s still very much a cash-generating machine.