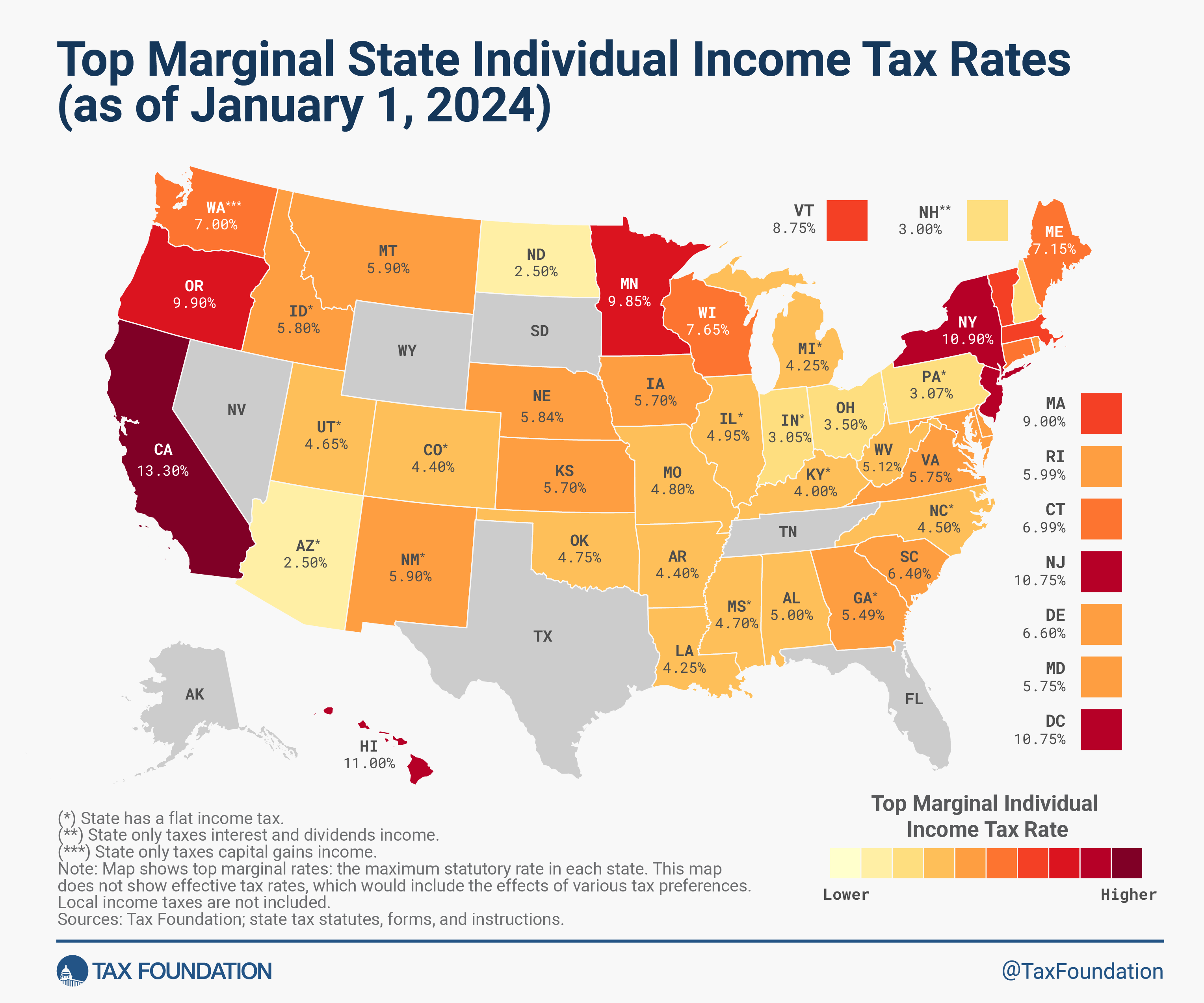

If you’ve ever looked at your paycheck in California and felt a tiny sting of betrayal, you aren't alone. It’s a common rite of passage here. You land a raise, you’re feeling great, and then the Golden State takes its cut. But there is a massive misunderstanding about how this actually works. Most people hear "13.3%" and think the government is snatching thirteen cents of every single dollar they earn.

California marginal tax rates don't work like a flat fee. It’s more like a staircase. You only pay the higher rates on the "steps" of income that actually reach those levels.

Honestly, the system is designed to be progressive. It’s basically built so that lower earners keep more of their cash while those at the top—think tech CEOs and Hollywood types—shoulder the heavier lifting. But even for the average person, the math can get a bit hairy. For the 2025 tax year (the ones you're likely thinking about right now in early 2026), the brackets have shifted slightly to account for inflation.

How the Brackets Actually Break Down

California uses nine different tax brackets for most of us. If you’re a single filer, your first $11,079 of taxable income is only taxed at 1%. That’s practically nothing. But as you climb, the percentages jump to 2%, 4%, 6%, and eventually hit a plateau for many middle-class workers at 9.3%.

If you’re lucky enough (or stressed enough) to earn over $1 million, you get hit with the Mental Health Services Act tax. That adds an extra 1% on top of the highest bracket. This brings the top rate to 13.3%. It’s currently the highest state income tax in the country.

Let's look at a quick example. Imagine you’re single and your taxable income is $60,000. You don't pay 8% on all $60,000.

- Your first $11,079 is taxed at 1% ($110.79).

- The next chunk up to $26,264 is at 2% ($303.70).

- The slice between that and $41,452 is at 4% ($607.52).

- The rest—from $41,452 to $60,000—is taxed at 6% ($1,112.88).

Your total bill? About $2,134.89. That’s an "effective" rate of roughly 3.5%, even though you "reached" the 6% bracket. See the difference?

🔗 Read more: The Rite Aid Millersport Getzville Situation: What You Need to Know Right Now

The 2026 Shift: Inflation and the "One Big Beautiful Bill"

Things got interesting recently. In late 2025, the federal "One Big Beautiful Bill" (OBBBA) passed, which fundamentally changed how inflation adjustments work for 2026. California generally tries to stay in "conformity" with federal rules, but they often march to the beat of their own drum.

For the 2026 tax year, the California Franchise Tax Board (FTB) adjusted the standard deduction. If you’re single, it’s now $5,706. If you’re married filing jointly, it’s $11,412. This is the "free" money you get to subtract from your gross income before the tax brackets even start touching your wallet.

The state also introduced some new nuances for 2026 regarding gambling losses and specific credits. For instance, starting this year, you can only deduct gambling losses up to 90% of your winnings—a slight tweak that might annoy the weekend warriors in Tahoe or Vegas.

Why Your "Taxable Income" Isn't Your Salary

People often confuse their salary with their taxable income. That’s a mistake. You have to subtract things first.

- Adjustments: Things like student loan interest or certain moving expenses.

- Deductions: Either the standard deduction mentioned above or "itemized" ones like mortgage interest (up to $1 million for CA, which is actually more generous than the federal $750k limit).

- Exemptions: California still gives you a personal exemption credit (usually around $149 for individuals), which acts like a gift card against the final tax you owe.

The Billionaire Tax Drama

There’s been a lot of noise about a proposed "Billionaire Tax" for 2026. This initiative, backed by groups like the SEIU-UHW, wants to slap a one-time 5% wealth tax on anyone with a net worth over $1 billion.

Governor Newsom has been pretty vocal about his opposition, worried it’ll chase the ultra-wealthy—and their massive tax contributions—out of the state. It’s a classic California dilemma: do you squeeze the rich to fund Medi-Cal, or do you play it safe so they don't move to Florida? As of now, it's a looming shadow over the 2026 legislative session.

Actionable Next Steps for Your Taxes

Don't just wait for April. If you're living in California, you've gotta be proactive.

Check your withholding. If you had a big life change—got married, had a kid, or bought a house—go to the FTB website and use their calculator. Adjusting your DE 4 (the California version of the W-4) can prevent a nasty surprise next year.

Max out your 401(k) or 403(b). California taxes capital gains as regular income. There is no "special" lower rate for long-term investments like there is at the federal level. By putting money into a traditional retirement account, you lower your taxable income today and dodge those 9.3% or higher California marginal tax rates.

Keep receipts for the "Small Stuff." California allows some deductions that the feds don't, especially around adoption costs or specific educator expenses. Even if you don't think you'll itemize, it pays to have the data ready.

Lastly, if you're an independent contractor or part of the "gig economy," remember that California's estimated tax payments are due quarterly. Missing these leads to penalties that can wipe out your hard-earned profits. Stay ahead of the deadlines, and the "staircase" won't feel nearly as steep.