Living in New York City is a choice. A choice for the best pizza at 3 a.m., the chaotic energy of the subway, and—unfortunately—the privilege of paying some of the most complex local taxes in the country. If you've ever squinted at your paystub and wondered why your take-home pay feels like it went through a paper shredder, you’re looking at the city tax rate nyc in action.

NYC is one of the few places in the United States that layers a local personal income tax on top of your state and federal obligations. It’s a literal price of admission for the 8.3 million people who call the five boroughs home. Honestly, it’s a lot to keep track of, especially with the 2026 adjustments and the new "Affordability Agenda" rolling out from Albany.

The Reality of the City Tax Rate NYC Right Now

If you live in the city, you pay. It doesn't matter if you work in a skyscraper in Midtown or remotely from a kitchen table in Astoria. The city tax rate nyc is based strictly on your residency. Unlike the New York State tax, which applies to anyone earning money within state lines, the NYC local tax is generally reserved for people who actually live here.

For the 2025-2026 tax cycle, these rates aren't just one flat number. That would be too simple for New York. Instead, we use a progressive system.

Basically, the more you make, the higher the percentage they take. Currently, the rates bounce between 3.078% and 3.876%.

Think of it as a four-step ladder. If you're a single filer making under $12,000, you're at the bottom step of 3.078%. But once your taxable income crosses that $50,000 threshold, you’ve hit the top step of 3.876%. Most middle-class New Yorkers find themselves sitting right at that top bracket almost immediately. It’s a steep climb for a relatively small income range.

How the 2026 Changes Affect Your Wallet

Governor Kathy Hochul recently made some waves with the FY2026 budget. There’s a lot of talk about "middle-class tax cuts," and while most of that happens at the state level, it changes the math for your overall burden.

Beginning January 1, 2026, we’re seeing a shift in how brackets are calculated to account for inflation. The standard deduction is also creeping up. For single filers, it’s now $16,100, and for married couples filing jointly, it’s $32,200. This is a big deal because it lowers the "taxable" portion of your income before the city tax rate nyc even touches it.

The New "No Tax on Tips" Proposal

One of the most interesting pivots for 2026 is the proposal to eliminate state income taxes on up to $25,000 of tipped income. For the thousands of servers, bartenders, and delivery workers in NYC, this is a massive win. While the city tax is separate, the "taxable income" base usually mirrors what the state sees. If the state ignores that first $25k in tips, your city tax liability could potentially drop alongside it.

The Child Tax Credit Boost

Families are getting a break, too. The Empire State Child Credit is seeing its biggest expansion ever. We're talking up to $1,000 per child under four years old. If you're struggling with the high cost of living in Brooklyn or Queens, these credits often act as the "offset" for the city tax you've been paying all year.

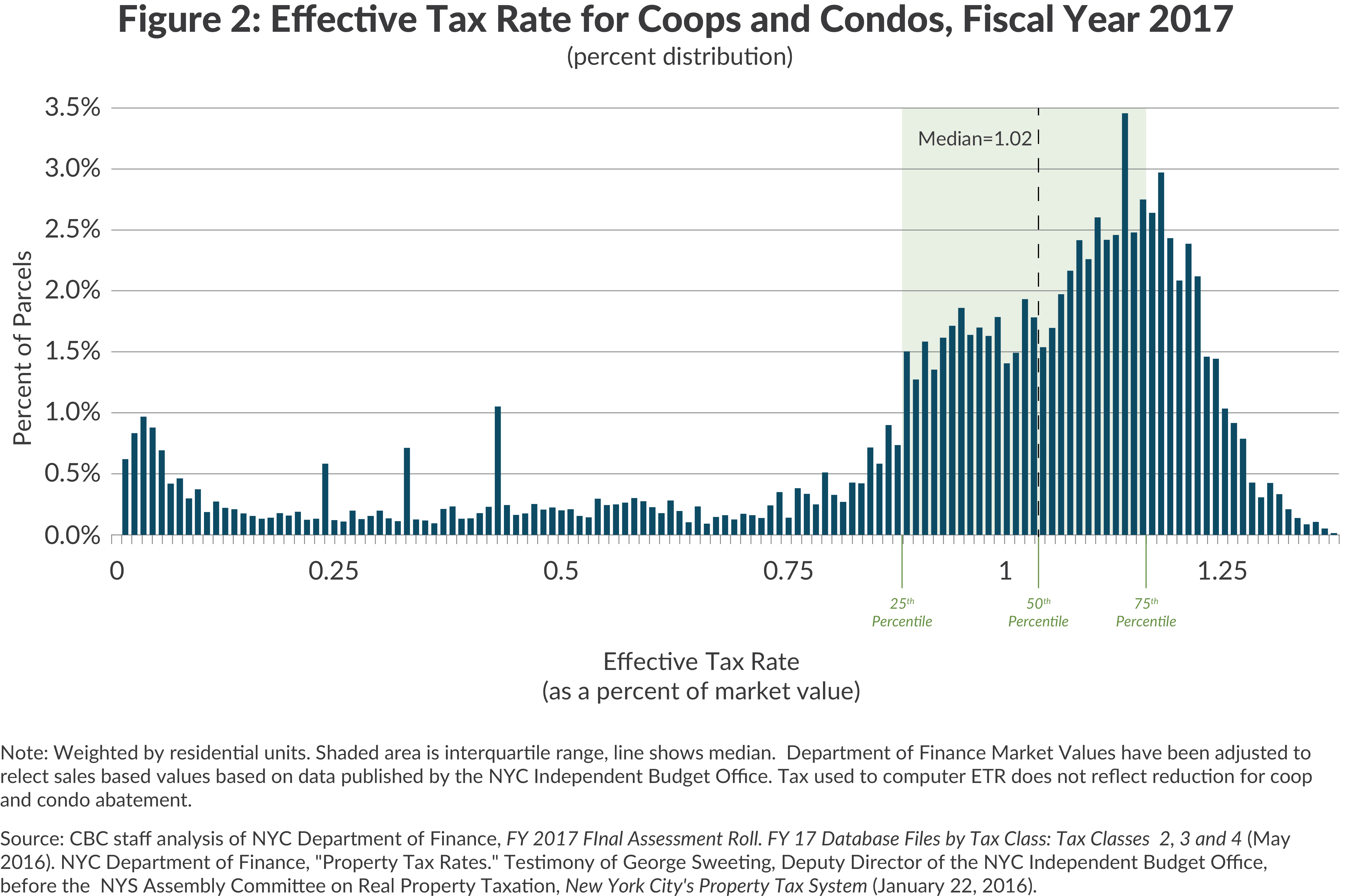

Property Taxes: The Hidden Giant

You might think you’re off the hook if you don't own a condo or a brownstone. You're not. Landlords just bake the property tax into your rent.

The NYC property tax rates for the 2025/2026 fiscal year were recently finalized. It was a bit of a rollercoaster in the City Council. They actually lowered the "Class Shares Cap" to 1%, which was intended to protect owners of one-to-three family homes.

Here is what the actual rates look like for this year:

- Class 1 (Homes): 19.843%

- Class 2 (Apartment buildings/Condos): 12.439%

- Class 4 (Commercial property): 10.848%

Class 1 saw its lowest rate in a decade, while Class 4 (commercial) hit a 19-year high. This shift is a deliberate attempt to keep long-term residents from being priced out of their homes by skyrocketing assessments, even if the city tax rate nyc on income stays relatively static.

Sales Tax: The 8.875% Punch

Every time you buy a coffee or a new pair of shoes (if they're over $110), you’re hit with a combined sales tax. It’s not just one tax. It’s a cocktail.

- New York State takes 4%.

- New York City takes 4.5%.

- The Metropolitan Commuter Transportation District (MCTD) adds a 0.375% surcharge.

Total? 8.875%.

The "clothing under $110" rule is still the best loophole in the city. If your sneakers are $109.99, you pay zero sales tax. If they are $110.01, you pay the full 8.875% on the whole amount. It’s a weirdly specific rule, but it’s one of the few ways to dodge the city's reach legally.

Residency: The 184-Day Rule

This is where people get into trouble. The "City of New York" is very protective of its tax base. If you have a place in the city and you spend more than 183 days here (meaning 184 or more), you are a resident for tax purposes. Even if your "permanent" home is in Florida.

Audit teams are notorious for checking cell phone towers, credit card swipes, and even social media posts to prove you were in the five boroughs. If they prove you’re a resident, they will come for that city tax rate nyc back-pay with interest.

Practical Steps to Manage Your NYC Tax Bill

Don't just let the city take what it wants. You have options to lower the blow.

Max out your 401(k) or 403(b). NYC taxes your Adjusted Gross Income. By putting money into a pre-tax retirement account, you lower your AGI. This can literally pull you down into a lower city tax bracket. If you can drop your taxable income below that $50,000 mark as a single filer, you save nearly a full percentage point on the city tax rate nyc.

Look into the EITC. The Earned Income Tax Credit isn't just for federal returns. New York City has its own version. If you’re earning under $63,000 (depending on your kids), you might be eligible for a credit that wipes out your city tax liability entirely.

Check your withholding. If you moved to the city recently, make sure your employer knows. If they are only withholding state tax and not the city tax, you’re going to have a very painful surprise come April. Use the IT-2104 form to update your status.

Keep receipts for "New York Sourced" income. If you are a freelancer who lives in Jersey but works in the city, you technically shouldn't be paying the NYC resident income tax, but you will pay state tax. Make sure your records clearly show where the work was performed so you don't get double-dipped by mistake.

✨ Don't miss: Credit Card Interest Cap: Why the 10 Percent Rate Matters

Living here isn't cheap. The taxes are part of the deal. But knowing exactly where that 3.8% is going—and how to keep a little more of it—is the only way to survive the New York hustle.

The most effective way to handle the 2026 tax season is to adjust your workplace withholdings immediately to reflect the new standard deductions. If you haven't looked at your Form IT-2104 since you were hired, now is the time to file a fresh one with your HR department. This ensures the city tax rate nyc is calculated accurately against your current salary and filing status, preventing a massive underpayment penalty later.