So, you're looking at your grocery receipt or your electric bill and wondering if the numbers are ever going to stop climbing. Honestly, it feels like we’ve been hearing about "sticky" prices for years now. If you want the quick answer to the current inflation rate US data, here is the latest: as of mid-January 2026, the annual inflation rate is sitting at 2.7%.

That figure comes straight from the Bureau of Labor Statistics (BLS) report released on January 13, 2026, covering the full year through December 2025.

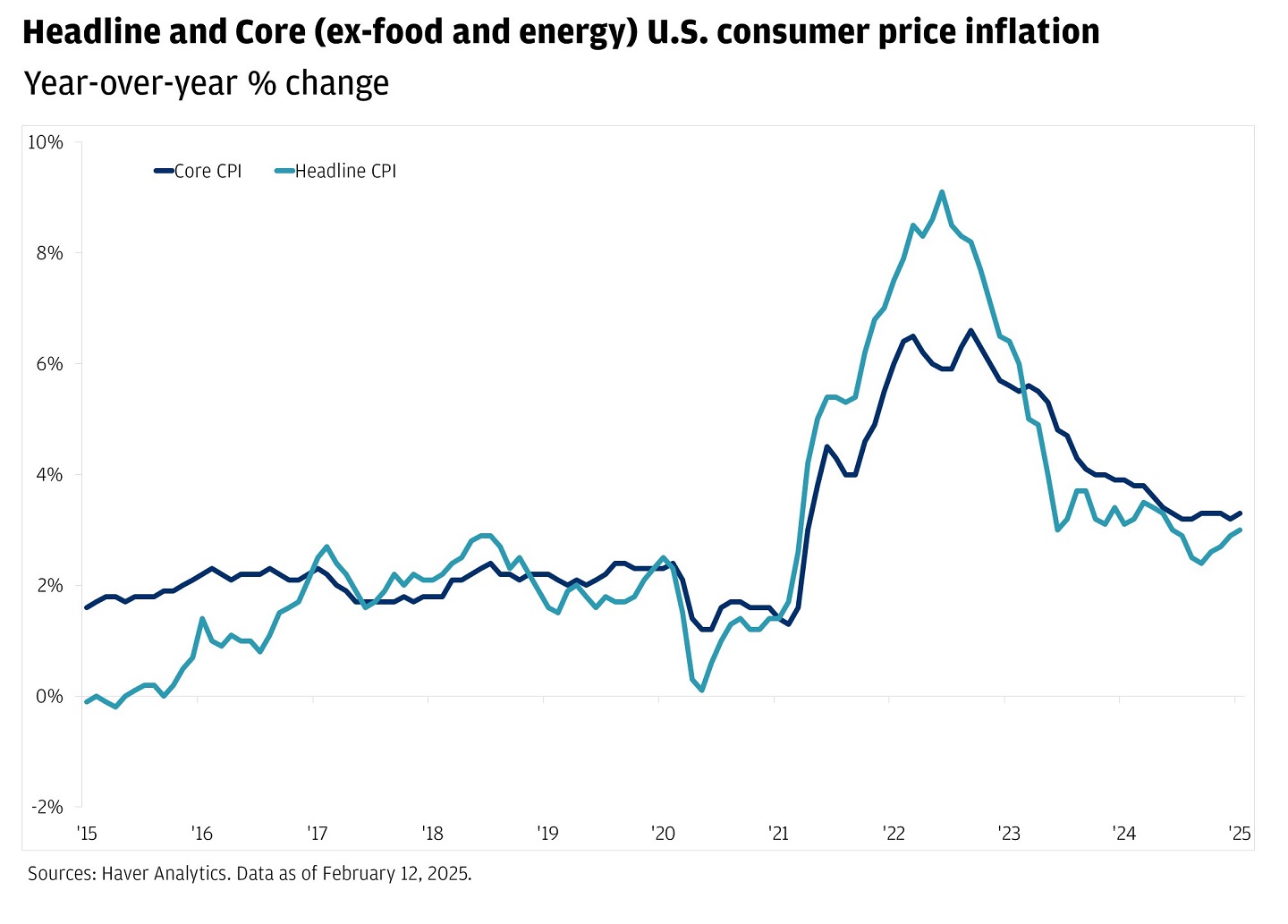

It didn't budge from the previous month. It’s flat. But "flat" at 2.7% doesn't mean prices are low; it just means they are rising at the same pace they were thirty days ago. While that's a massive relief compared to the 9.1% nightmare we saw back in 2022, we aren't exactly back to the "good old days" of 2% yet.

The Core Problem: Why 2.7% Feels Like More

Most people look at the 2.7% headline number and think, "No way. My eggs cost way more than 3% extra." You aren't crazy. The headline current inflation rate US is an average. It's a giant basket of everything from used cars to haircuts.

📖 Related: Tuition for South Carolina State University Explained: What You'll Actually Pay

When you strip out the volatile stuff—specifically food and energy—you get what economists call "Core CPI." Right now, that core rate is slightly lower at 2.6%.

Here is where it gets tricky. While the overall number looks stable, the stuff you actually buy every week is acting up. In the latest report, food prices jumped 0.7% in a single month. That is a huge monthly spike. If you feel like your wallet is leaking cash at the checkout line, it's because food-at-home costs are rising faster than the general average.

What’s actually getting more expensive?

It’s a weird mix of winners and losers right now.

- Electricity: Up a staggering 6.7% over the last year.

- Natural Gas: Even worse, up 10.8%.

- Hospital Services: Climbing by 6.6%.

- The "Fun" Stuff: Recreation costs had their biggest one-month jump in decades this past December, rising 1.2%.

On the flip side, some things are actually getting cheaper, which pulls that average down. Gasoline is down about 3.4% compared to last year. If you don't drive much but eat a lot and keep your heater on, your personal inflation rate is way higher than 2.7%.

The "Tariff" Factor and the 2026 Outlook

We can't talk about the current inflation rate US without mentioning the policy shifts. Recently, we’ve seen the impact of the "One Big Beautiful Bill Act" (OBBBA) and various tariff discussions.

Economists like David Mericle at Goldman Sachs are actually somewhat optimistic for the rest of 2026. They think the "drag" from initial tariffs might give way to a boost from tax cuts. They're forecasting core inflation could drift down toward 2.1% by the end of this year.

But not everyone agrees.

J.P. Morgan’s analysts are watching a different set of risks. They worry that a weakening dollar and a tighter labor supply (partly due to immigration crackdowns) could keep a floor under how low prices can go. Basically, if there aren't enough workers to move goods or staff restaurants, wages stay high, and those costs get passed directly to you.

The Fed's Next Move: Will Rates Drop?

The Federal Reserve is in a tough spot. They want that 2% target. They're obsessed with it. Federal Reserve Vice Chair Jefferson recently noted that while we’ve made progress, the "progress slowed over the past year."

What does this mean for your mortgage or credit card?

- The Fed is likely to hold rates steady at their late January 2026 meeting.

- Market "nowcasts" suggest inflation might tick down slightly in the January report (due out February 11), but nobody is celebrating yet.

- If the labor market stays strong—meaning people aren't getting fired in droves—the Fed has no reason to rush into cutting interest rates.

Why This Matters for Your Wallet

Knowing the current inflation rate US is 2.7% is fine for trivia, but it matters for your actual life because it dictates "real wages." In the last month, real average weekly earnings actually dropped by 0.27%.

In plain English: prices rose faster than your last raise.

You're technically working the same hours for less buying power. That’s the "hidden tax" of inflation that everyone hates. Even when the rate is "low" at 2.7%, if your boss didn't give you a 3% bump this year, you took a pay cut.

Actionable Steps for 2026

Since we know the current inflation rate US is staying "sticky" around that 2.7% mark, you need to adjust your strategy. You can't just wait for prices to go back to 2019 levels—they almost certainly won't.

- Lock in Fixed Rates: If you’re carrying high-interest debt, don't bank on the Fed dropping rates 2 or 3 percent this year. They are moving slowly. Look into consolidating debt now while the market is "cautiously optimistic."

- Audit Your Energy: With electricity and natural gas being the biggest "bad actors" in the CPI report (rising 6% to 10%), a $200 smart thermostat or some weather stripping will probably pay for itself in three months.

- Watch the February 11 Update: The next BLS report will include "title changes" for how they track things like home health care and vocational school tuition. These changes can sometimes shift the "weight" of the index, making the headline number look better or worse than it really is.

- Re-evaluate Cash Reserves: With inflation at 2.7% and many high-yield savings accounts still offering 4% or more, you are finally "beating" inflation with your savings. It’s a good time to keep your emergency fund in a liquid, interest-bearing account rather than a standard checking account.

The bottom line is that 2.7% is the new normal for now. It’s not a crisis, but it’s not a victory either. It’s just... there. Staying informed on these monthly shifts helps you see through the political noise and actually plan your budget for what's coming next.

📖 Related: Why the Price of Nike Stock Still Matters for Your Portfolio

Data Reference:

- U.S. Bureau of Labor Statistics (BLS), Consumer Price Index Summary - December 2025 (Released Jan 13, 2026).

- Federal Reserve Board, Speech by Vice Chair Jefferson (Jan 16, 2026).

- Cleveland Fed Inflation Nowcasting (Updated Jan 16, 2026).