Tax season is basically the adult version of waiting for a final grade on a test you didn't study for. You’re sitting there, staring at a screen or a pile of receipts, wondering if the government is going to send you a check or if you're going to be eating ramen for a month. Honestly, most people just want to know one thing: "How much of my money do I actually get to keep?"

The answer depends on the current irs tax rates, which are more like a shifting landscape than a fixed set of rules. For the 2026 tax year, things have gotten interesting because of a massive piece of legislation called the One Big Beautiful Bill Act (OBBBA). It basically took the "temporary" tax cuts we’ve been living with since 2017 and made them permanent. If that hadn't happened, we’d be looking at a much nastier tax bill right now.

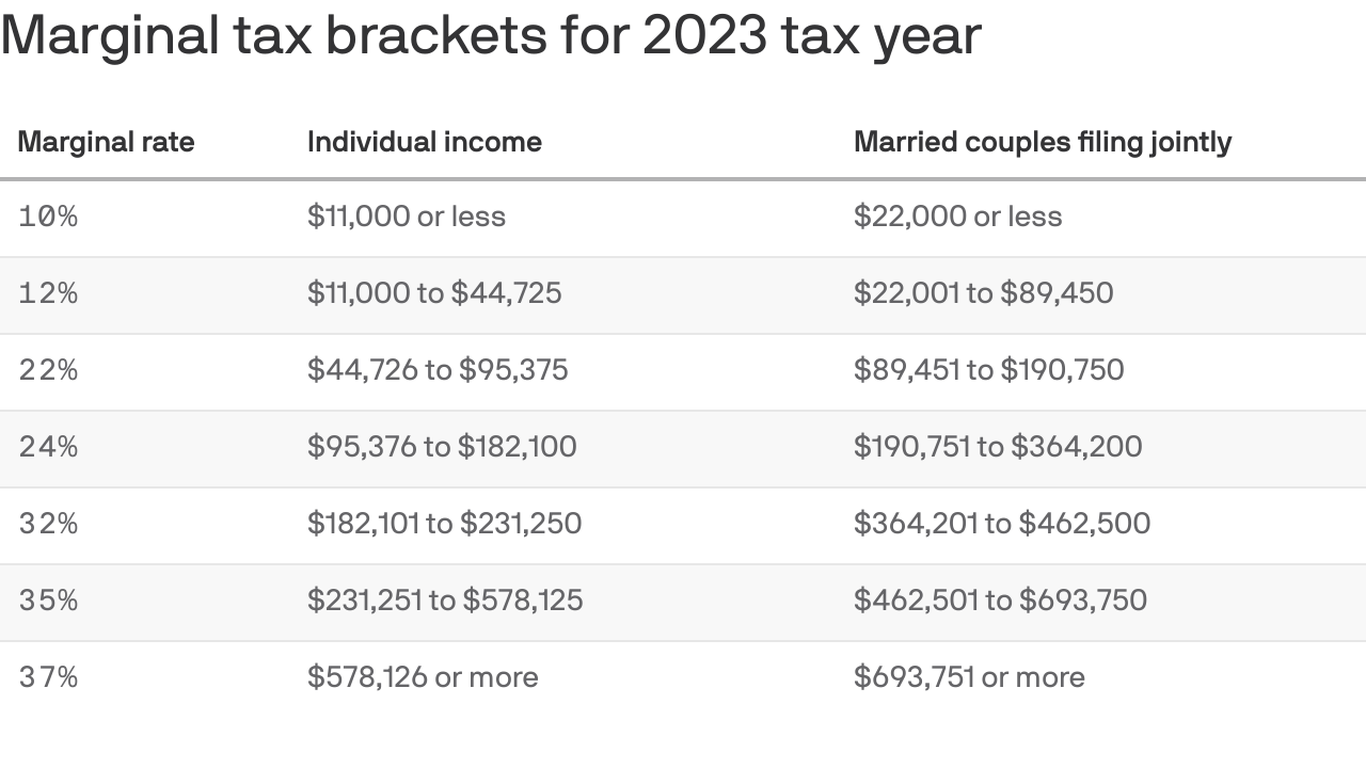

The 2026 Tax Bracket Ladder

Most people think that if they "land" in a 24% tax bracket, the IRS just takes 24% of everything they earned. That is a total myth. Our system is progressive. Think of it like a ladder. You pay a little bit on the first rung, a bit more on the second, and so on. You only pay the higher rate on the money that actually reaches that higher rung.

For the 2026 tax year, if you’re filing as a Single Filer, your first $12,400 is taxed at just 10%. If you make more than that, the next chunk—up to $50,400—is taxed at 12%. The rungs keep going: 22% starts after $50,400, 24% kicks in at $105,701, and it climbs up to 32%, 35%, and finally 37% for anything over $640,600.

Now, if you're Married Filing Jointly, the rungs are wider. You don't hit that 12% mark until you’ve earned over $24,800. The 22% rate doesn't even touch you until your combined taxable income passes $100,800. It stays at 24% until you cross $211,400. The top 37% rate for married couples doesn't start until you're bringing in more than $768,700. It’s a huge difference. Basically, the IRS gives you a bit of a "marriage bonus" by letting you keep more money in those lower-percentage buckets.

The Standard Deduction: Your "Free" Money

Before you even look at those brackets, you have to talk about the standard deduction. This is the amount of income the IRS basically pretends you didn't earn. It’s your "shield." For 2026, the OBBBA gave this a nice little boost.

If you are single, your standard deduction is $16,100. If you’re married filing jointly, it’s a whopping $32,200.

🔗 Read more: Hair Salon Window Decals: What Most People Get Wrong About Street-Level Branding

Think about that for a second. If you and your spouse make $70,000 together, you subtract $32,200 right off the top. Now you’re only being taxed on $37,800. That’s the "taxable income" that actually goes into the brackets we just talked about.

Wait, it gets better for older taxpayers. If you’re 65 or older, there is a brand new deduction. It’s not just an "adjustment"—it’s a fresh $6,000 deduction per person ($12,000 for a couple). There are income limits, sure. It starts fading away if you make more than $75,000 (single) or $150,000 (married), but for a lot of retirees, this is a massive win. It’s separate from the standard deduction. You can take both.

Capital Gains: The "Rich Person" Tax (That You Can Use Too)

Not all income is treated the same. If you work a job, you pay ordinary income rates. But if you sell a stock you’ve held for more than a year, you’re looking at long-term capital gains. These rates are way lower.

For most people, the capital gains rate is 15%. But here’s the kicker: if your total taxable income is below $49,450 (single) or $98,900 (married), your capital gains tax rate is 0%.

Yes, zero.

You could sell a winning stock and pay nothing to the IRS if your other income is low enough. If you’re a high flyer making over $545,500 (single) or $613,700 (married), that rate bumps up to 20%. Plus, there’s still that 3.8% Net Investment Income Tax (NIIT) for high earners, which brings the total to 23.8%. But for the average person, 15%—or even 0%—is the name of the game.

What about the "No Tax on Tips" Thing?

You’ve probably heard the buzz about "no tax on tips" or "no tax on overtime." This was a huge part of the OBBBA. Basically, for the 2025 and 2026 tax years, if you’re a service worker or someone putting in 60-hour weeks, the government is cutting you a break. There are specific caps and rules—you can't just call your $200,000 salary a "tip"—but for waitstaff and blue-collar workers, this is putting real money back in paychecks every Friday.

Why Your "Effective" Rate Is the Only Number That Matters

Your marginal rate (the highest bracket you touch) is great for cocktail party talk, but your effective rate is the real story. This is the total tax you paid divided by your total income.

Let's say you're single and earn $100,000.

- You take the $16,100 standard deduction. Your taxable income is $83,900.

- The first $12,400 is taxed at 10% ($1,240).

- The next $38,000 (up to $50,400) is taxed at 12% ($4,560).

- The remaining $33,500 is taxed at 22% ($7,370).

- Total tax: $13,170.

Your marginal rate is 22%. But your effective rate? It’s $13,170 divided by $100,000. That’s 13.17%. You’re actually paying less than 14 cents on the dollar, even though you "feel" like you're in a much higher bracket. Understanding this helps you breathe a little easier when you see those big percentage numbers in the headlines.

Actionable Steps to Lower Your Bill Right Now

The current irs tax rates are set, but your taxable income isn't. You have more control than you think.

- Max out your 401(k) or 403(b): For 2026, you can put away $24,500 ($32,500 if you're 50+). This money comes right off your taxable income. It's like an instant deduction.

- Check the new car interest deduction: If you bought a new U.S.-assembled vehicle for personal use, you might be able to deduct up to $10,000 in interest. This is a temporary perk from the OBBBA, so use it while it lasts.

- Look at the SALT cap: The limit for State and Local Tax deductions jumped to $40,000 for married couples. If you live in a high-tax state like California or New York, this could finally make it worth itemizing instead of taking the standard deduction.

- Harvest your losses: If you have stocks that are down, sell them to offset your gains. You can even use up to $3,000 of "extra" losses to reduce your ordinary income.

The 2026 tax year is actually looking pretty good for most middle-class families. With the higher standard deductions and the permanent 12% and 22% brackets, the "tax cliff" everyone was worried about has been avoided for now. Just make sure you aren't leaving money on the table by ignoring those new 65+ deductions or the car interest breaks.

👉 See also: Derek Stevens Circa Net Worth: Why the Casino Mogul is Worth More Than the Billions He Spent

Next Steps for You:

Check your last pay stub. Look at your "Year to Date" federal withholding. Compare that to the 13-15% effective rate we calculated earlier. If you're withholding way more than that, you might want to adjust your W-4 so you get that money in your paycheck now instead of waiting for a refund next year.