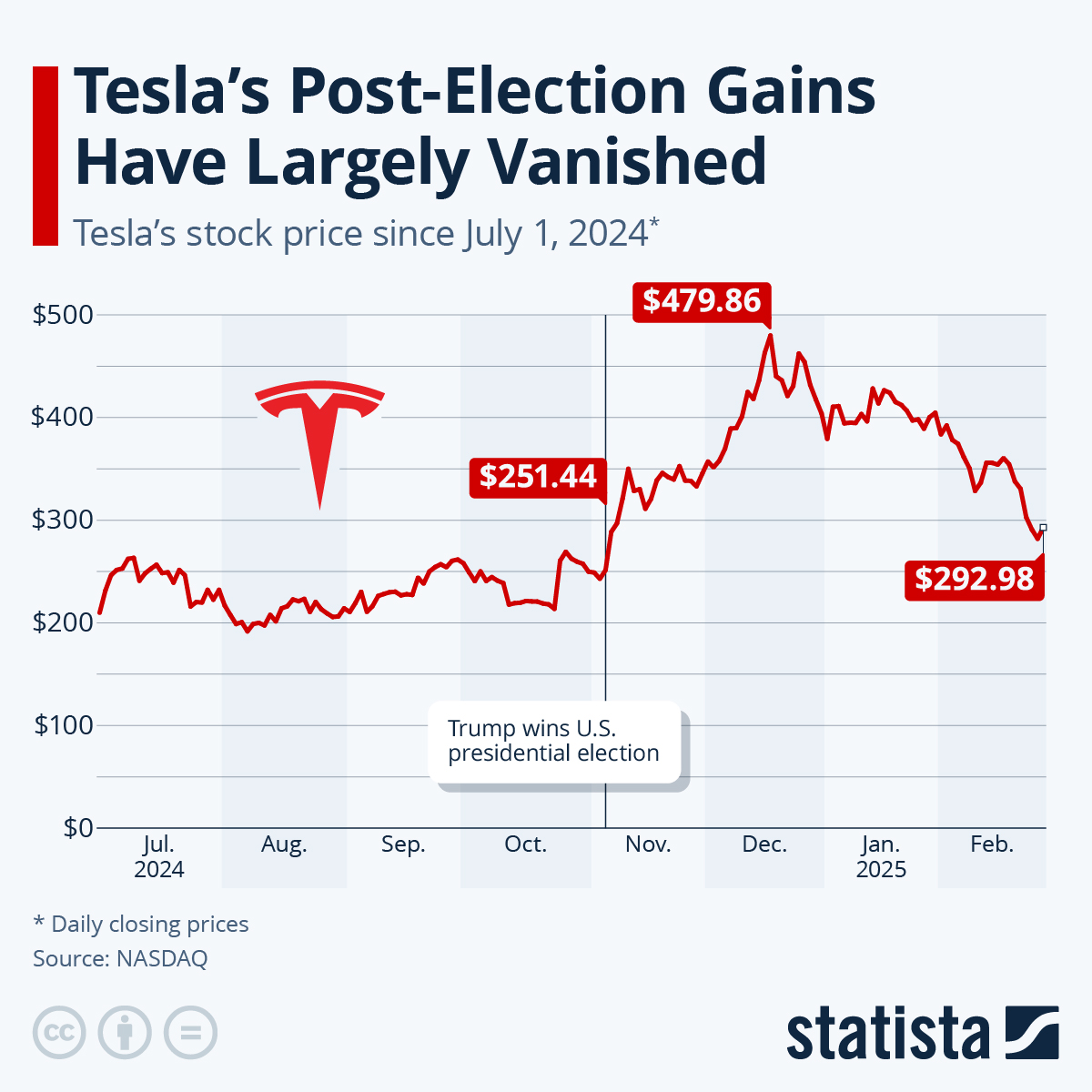

Honestly, trying to pin down the current Tesla share price is like trying to catch a greased pig in a thunderstorm. You look at your phone, it’s one number. You blink, it’s another.

As of right now—mid-January 2026—Tesla (TSLA) is hovering around $437.50.

It’s been a weirdly quiet week for a stock that usually moves with the drama of a soap opera. On Friday, January 16, the price slipped just a tiny bit, down about 0.24%. It opened at $439.50 and spent most of the day bouncing between a low of $435.26 and a high of $447.25. If you’re a day trader, maybe that gave you some juice, but for most of us, it’s just noise before the big storm.

That storm? The Q4 2025 earnings report. It’s coming on January 28.

Investors are basically holding their breath. Nobody wants to make a huge move until they see if Elon Musk can actually stabilize those shrinking profit margins. It's a classic "wait and see" moment.

Why the current Tesla share price feels like a standoff

We've entered this consolidation phase. Basically, the stock is stuck in a box.

Buyers are stepping in around the $420 mark to keep it from tanking, but sellers are dumping shares as soon as it nears $450. It’s a tug-of-war where neither side is winning.

💡 You might also like: US Dollar Exchange Rate in BD: Why It’s Finally Moving Differently in 2026

The reason for the jitters isn't just one thing. It’s a messy cocktail of lithium prices, cooling EV demand, and the fact that Tesla is no longer the undisputed king of the mountain. Did you catch the news that they recently lost their "EV Crown" to global competitors? That sort of thing stings, and it's reflected in the price.

Even though the stock is up significantly from its 2024 lows, it’s still struggling to regain that absolute "moon mission" momentum we saw a few years back.

The Margin Problem (Simply Put)

For a long time, Tesla made way more money per car than anyone else. Like, a lot more.

Then came the price wars.

To keep moving metal, Tesla slashed prices throughout 2024 and 2025. It worked for volume, but it killed the profit-per-vehicle. Now, Wall Street is obsessed with one thing: Gross Margins. If the upcoming earnings show that margins are finally stabilizing, the current Tesla share price might finally break out of this $430-$440 range.

If they keep slipping? Well, the "bears" are already sharpening their claws, with some analysts like GLJ Research suggesting the valuation is still way too high for a car company that's seeing revenue growth slow down.

What's actually propping up the price right now?

If Tesla were just a car company, the price would probably be much lower. But it isn't—or at least, the market doesn't treat it that way.

The $1.4 trillion market cap is built on "What Ifs."

- Optimus: Musk is promising mass production of the Optimus humanoid robot by the end of 2026. He says it could eventually make Tesla worth $10 trillion. Whether you believe him or think it’s vaporware, that hope is baked into the current Tesla share price.

- The Cybercab: We’re supposed to see the first driverless "Cybercab" units roll off the line in April 2026. No steering wheel. No pedals. It sounds cool, but the regulatory hurdles are massive.

- Energy Storage: This is the quiet hero. Tesla’s Megapacks and solar business are actually growing quite fast, providing a nice cushion when car sales get "squishy."

The Analyst Divide

You’ve got guys like Dan Ives at Wedbush who are still banging the drum for a $600 price target. He thinks the AI and FSD (Full Self-Driving) story is just getting started.

Then you have the crowd over at JPMorgan or Wells Fargo who look at the P/E ratio (Price-to-Earnings)—which is currently sitting at a whopping 292—and think the whole thing is a bubble waiting for a pin.

Most people are somewhere in the middle. The consensus rating right now is a "Hold." It’s not exactly a ringing endorsement, but it’s not a "run for the hills" signal either.

👉 See also: How Did the Stock Market Close: The AI Rally Returns

Real-world factors you might have missed

It's not all about robots and software. Some very boring things are moving the current Tesla share price lately.

Take the "Low-Voltage Connector Standard" (LVCS). Tesla just announced they’re shrinking the number of electrical connectors in their cars from over 200 down to just six. It sounds like a snooze-fest, right? But for manufacturing, that’s huge. It makes the cars cheaper and faster to build.

Also, watch the lithium market.

Analysts are predicting a lithium deficit starting later this year. Since Tesla is vertically integrated and has its own lithium refining capacity in Texas, a spike in raw material costs might actually hurt their competitors more than it hurts them. It’s a weird "bad news is good news" situation for the stock.

Your next steps as an investor or observer

If you’re looking at the current Tesla share price and wondering whether to jump in or bail out, don't just stare at the daily ticker. It’ll drive you crazy.

💡 You might also like: Public Square Stock Price: What Most People Get Wrong

- Watch the January 28 Earnings: This is the "make or break" date for the quarter. Look specifically for "Automotive Gross Margin excluding credits." If it’s above 17-18%, the market will likely cheer.

- Check the RSI: The Relative Strength Index is currently around 41. That means the stock isn't "oversold" yet, but it’s definitely not "overbought." It’s in no-man's-land.

- Follow the Fed: Tesla is sensitive to interest rates. If the Federal Reserve hints at more cuts in 2026, tech and growth stocks like TSLA usually get a tailwind.

- Ignore the Hype (and the Hate): Both the Musk superfans and the "Tesla is going to zero" crowd are usually wrong. Look at the delivery numbers and the cash flow. Everything else is just a story.

Keep an eye on the $415 support level. If the price breaks below that, we could see a quick slide toward $380. On the flip side, a clean break above $450 could mean the bulls are back in charge for the spring.

Whatever happens, it’s going to be a bumpy ride. It always is with this one.

Actionable Insight: Before the Q4 earnings call on January 28, review your portfolio's exposure to the "Magnificent Seven." Tesla's high P/E ratio makes it significantly more volatile than peers like Apple or Microsoft. If you are holding TSLA for the long term, focus on the progress of the "Cybercab" production timeline rather than the weekly price fluctuations. Managers of large ETFs are currently watching the $420 level as a key psychological floor; a daily close below this could trigger automated sell-offs.