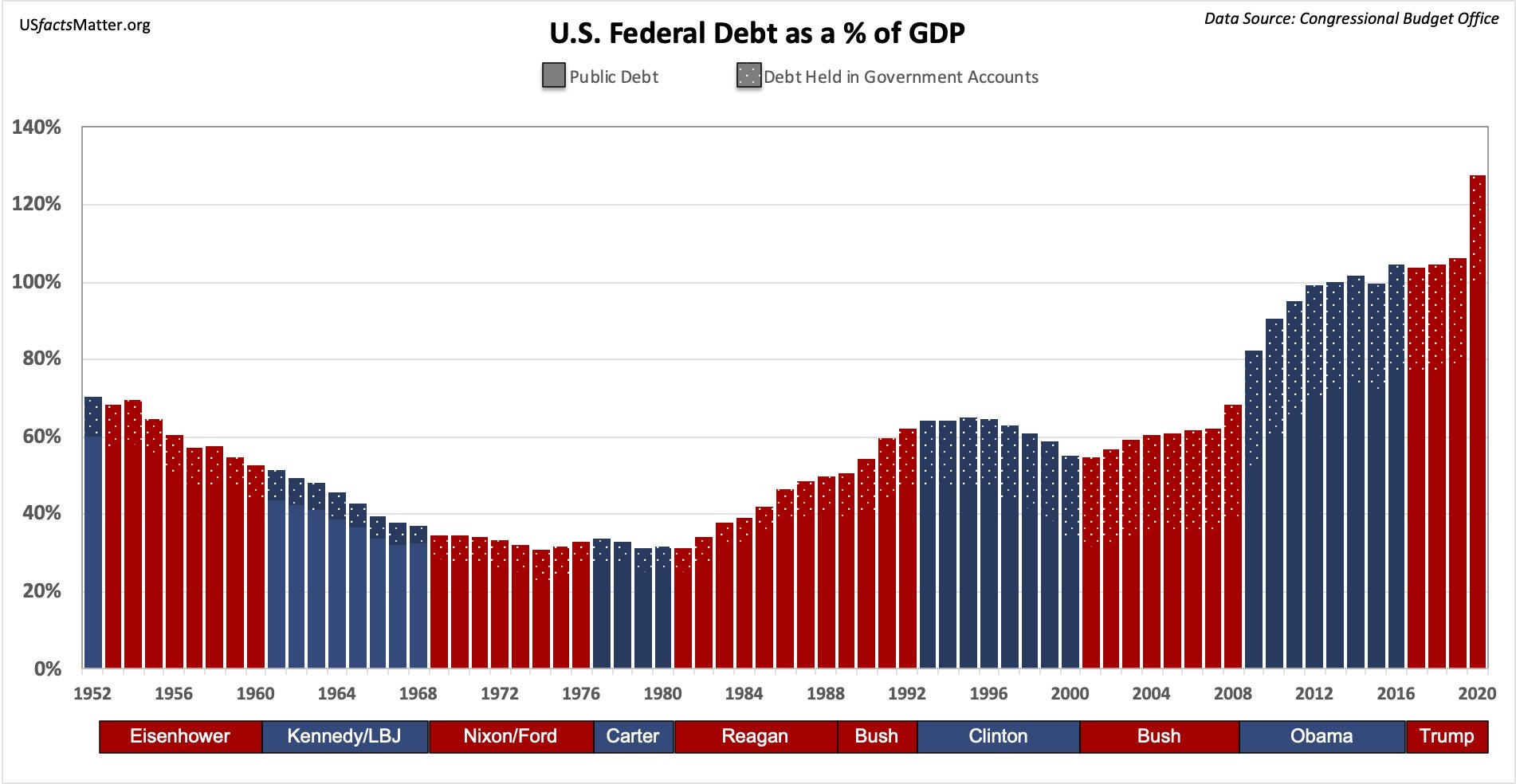

You’ve probably seen the "debt clock" ticking away in New York City or on some frantic news broadcast. It’s terrifying, honestly. The numbers move so fast you can’t even read them. But if we’re being real, that massive $38.43 trillion figure—the current total gross national debt—doesn't mean much to the average person until you start breaking it down into what it actually costs you.

Right now, as we move through January 2026, the debt per person in the US is roughly $112,966.

Think about that. If the government knocked on your door tomorrow and asked for your "fair share" of the national tab, you'd be handing over a six-figure check. And that's just the public side of the coin. It doesn't even touch your own credit cards, that lingering car loan, or the mortgage. When you combine what the government owes on your behalf with what you actually owe the bank, the picture gets a lot more complicated.

The Two Worlds of American Debt

There is a huge difference between the debt the government carries and the debt you're trying to pay off before the 15th of the month. People mix these up all the time.

💡 You might also like: CVS Anthem Village Henderson NV: What Most People Get Wrong

First, you have the National Debt. This is the federal government’s "credit card." As of early 2026, it sits at over $38 trillion. If you divide that by every man, woman, and child in the country, you get that $112k number. It’s grown by about $6,600 per person just in the last year. Basically, the government is spending about $6 billion more than it takes in every single day.

Then, there’s Consumer Debt. This is the stuff that actually keeps you up at night. According to recent data from the New York Fed and Experian, the average adult with a credit score owes about $63,300. If you look at it per household, that number spikes to over $105,000.

So, if you’re a typical American, you’re essentially "on the hook" for your $63k in personal loans and your $112k share of the national debt. That’s a $175,000 burden per person.

Where is all this money going?

It’s not just one thing. It's a "death by a thousand cuts" situation. For the government, it's mostly Social Security, Medicare, and the interest on the debt itself. In fact, interest is now the second-largest federal expense. We are paying over $1 trillion a year just in interest. That's money not going to roads, schools, or tech.

For you? It’s usually the big three:

- Mortgages: This is the elephant in the room, making up about 70% of all household debt. The average balance is hanging around $268,000 for those who have one.

- Auto Loans: We love our trucks and SUVs. Average auto debt is holding steady at $1.66 trillion nationally.

- Credit Cards: This is where the "pinch" is felt most. Total credit card debt hit $1.23 trillion recently. The average person carries a balance of about $6,500.

Your Age Changes Everything

Debt isn't "one size fits all." Depending on when you were born, your debt per person in the US looks wildly different.

Gen X (Ages 46-61) are currently the "Debt Kings," but not in a good way. They owe the most—averaging roughly $158,105 per person. Why? They’re in the "sandwich" years. They’re paying for their kids' college, their own mortgages, and sometimes even helping out aging parents.

Millennials (Ages 30-45) are right behind them at about $132,280. This group is finally getting into the housing market (at much higher interest rates than their parents) and still wrestling with student loans. Speaking of student loans, those balances rose by $15 billion in late 2025 alone.

Gen Z is the one to watch. Their debt is lower—around $34,328—but it's growing the fastest. Their balances jumped nearly 8% in a year. They’re just starting to get their first "real" credit cards and car notes.

The Stagflation Lite Problem of 2026

Experts from places like RBC Economics are calling this era "Stagflation Lite." Basically, growth is a bit slow, but prices (and interest rates) are still high enough to hurt.

We saw the longest government shutdown in history kick off this fiscal year, which didn't help consumer confidence. Plus, there’s been a massive surge in customs duties—up over 280% due to new tariffs. While that brings in revenue for the government, it often trickles down to higher prices for you at the store. When things cost more, people put more on their credit cards. It's a vicious cycle.

Delinquency rates are the "canary in the coal mine." Right now, about 4.5% of all debt is in some stage of delinquency. Credit cards are the worst, with over 8% of balances being 30+ days past due. People are starting to struggle with the "sticky" inflation that just won't go away.

Why Does the National Debt Matter to You?

You might think, "I'm never going to pay back the national debt, so why care?"

Fair point. But it affects you in ways you don't see. When the government owes $38 trillion, they have to pay high interest to the people who buy their bonds. To pay that interest, they might:

✨ Don't miss: Why the Bowling Green General Motors Plant is Still the Most Important Factory in America

- Raise Taxes: We've already seen individual income and payroll tax collections rise by $69 billion this year.

- Keep Interest Rates High: To fight the inflation caused by overspending, the Fed keeps rates up. This means your next car loan or mortgage will cost way more.

- Cut Services: Eventually, there's less money for things like the 2.8% cost-of-living adjustment (COLA) for Social Security that just went into effect.

What You Can Actually Do

You can't fix the $38 trillion federal hole. But you can fix your portion of the debt per person in the US.

Honestly, the "snowball method" is still the gold standard for a reason. You list your debts from smallest to largest and attack the small ones first. It gives you that dopamine hit when a balance hits zero. If you're a Gen Xer with $150k in debt, you might need a more aggressive "avalanche" approach—targeting the highest interest rates first to stop the bleeding.

Watch out for HELOCs (Home Equity Lines of Credit). They’ve become popular again because home values are high, but they’re risky. If you can't pay it back, the bank takes the house. HELOC limits rose by $8 billion recently, meaning people are tapping into their homes to pay for other things. That’s a dangerous game in a 2026 economy.

Moving Forward

The numbers are big. They're scary. But they are also just data points.

📖 Related: J. Milton and Associates: What Most People Get Wrong About Miami’s Real Estate Dynasty

Knowing that the average debt per person in the US is $112k (public) and $63k (private) gives you a benchmark. If you're below that, you're actually doing better than the "average" American. If you're above it, it’s time to look at where those leaks are.

Start by checking your "debt-to-income" ratio. In places like Hawaii, people owe $2.04 for every $1 they earn. In New York, it's closer to $0.89. If your debt is more than double your annual income, you're in the "red zone."

Practical Next Steps:

- Calculate your personal Debt-to-Income (DTI) ratio: Take your total monthly debt payments and divide them by your gross monthly income. If you're over 43%, most lenders won't even look at you for a new loan.

- Audit your "Revolving" Debt: This is the stuff that never goes away. If your credit card balance is $6,500 (the national average), paying just the minimum will take you decades. Double your minimum payment starting this month.

- Check for "Zombie" Subscriptions: In a 2026 world of digital services, the average person wastes $400 a year on stuff they don't use. That's a car payment or a significant credit card chunk.

- Target the "Interest Trap": With national interest rates hovering around 3.3% for the government but 20%+ for your credit cards, focus every extra penny on the high-interest debt first. This is the only way to beat the "Stagflation Lite" trend.