If you’ve been watching the dirt fly—or lack thereof—in the commercial construction world lately, the Dodge Momentum Index October 2025 data tells a story that isn't exactly what the headlines promised six months ago. We all expected a massive surge. Rates dropped, inflation cooled, and yet, the "wall of capital" everyone talked about is more like a slow-moving tide.

The Dodge Momentum Index (DMI) basically tracks non-residential building projects the moment they enter the planning stage. It’s a lead indicator. It tells us what the skyline will look like in 12 to 18 months. In October 2025, the index showed a nuanced tug-of-war between a ravenous data center market and a retail sector that’s honestly just trying to find its footing again.

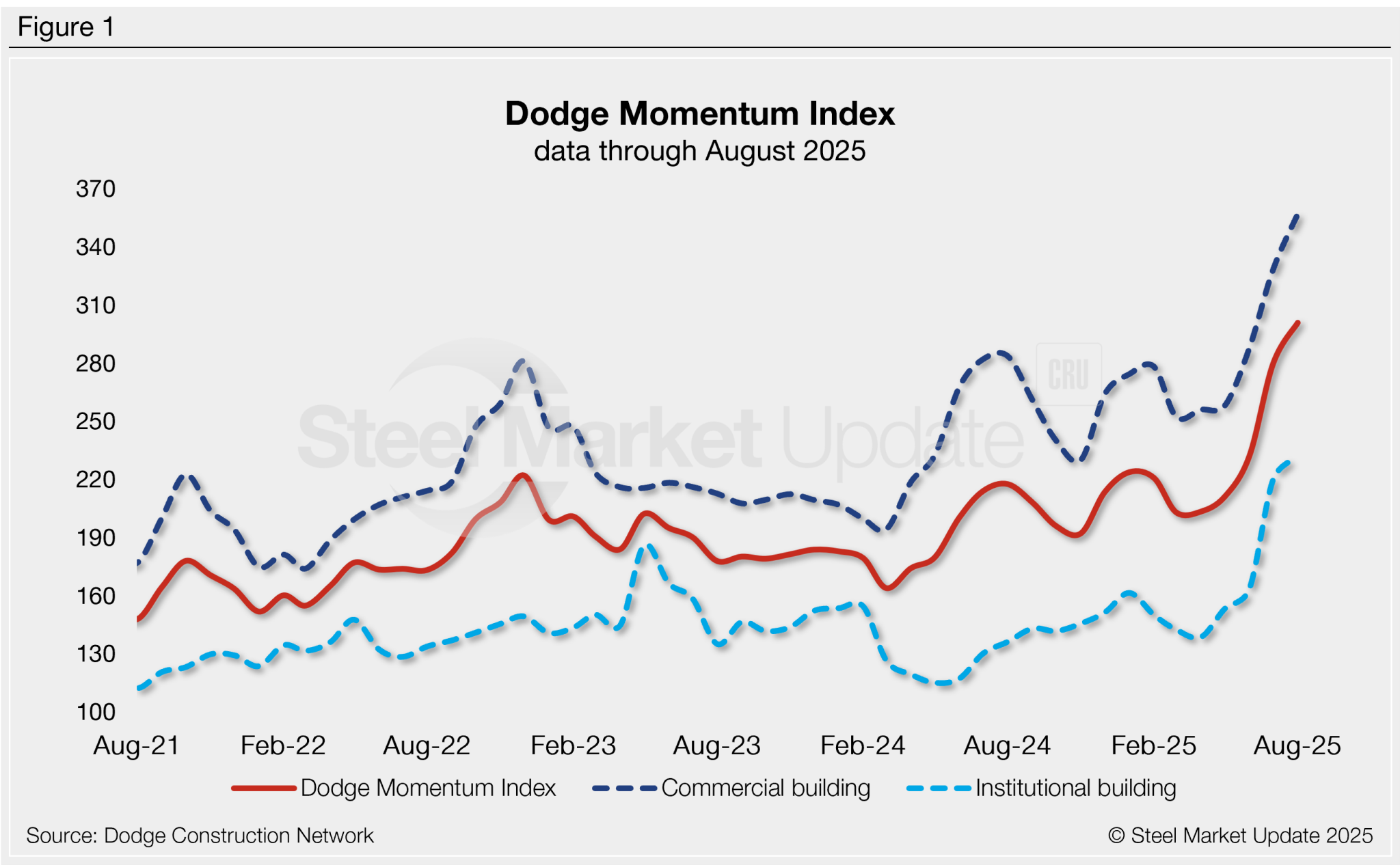

Breaking Down the October Numbers

The headline figure for the Dodge Momentum Index October 2025 came in at 212.4, a slight but meaningful nudge upward from September’s revised figures. To put that in perspective, we are seeing a marketplace that is stabilizing after the erratic spikes of 2023 and 2024.

👉 See also: World Market Center Las Vegas: Why This Massive Hub Still Rules Global Design

The institutional side of the house—think hospitals, schools, and government buildings—actually carried a lot of the weight this time around. It rose about 4%. Meanwhile, the commercial side, which includes warehouses and offices, felt a bit flatter, gaining less than 1%. It's a bit of a head-scratcher if you only look at the surface. You’d think with the current tech boom, commercial would be skyrocketing.

But here’s the thing.

The way Dodge Construction Network tracks these "commercial" projects includes a massive amount of warehouse space. And we are currently coming off a multi-year binge of Amazon-led fulfillment center construction. That’s cooling. We don’t need a new million-square-foot shed every fifty miles anymore. Instead, the "momentum" is moving toward hyper-specialized facilities.

The Data Center Dominance

Let’s talk about the elephant in the room: AI.

In October 2025, data center planning remained the primary engine for the commercial component of the index. These aren't just buildings; they are massive power-grid-taxing vaults. Sarah Martin, the associate director of forecasting at Dodge, has pointed out throughout this year that without data centers, the commercial planning numbers would look pretty grim.

It's a weirdly lopsided economy.

If you're an electrical contractor or a cooling systems specialist, the Dodge Momentum Index October 2025 looks like a gold mine. If you’re a traditional office developer? Not so much. The "Flight to Quality" is still a real thing, but new office starts are increasingly rare, appearing only in "super-prime" locations in cities like Miami, Austin, or parts of Nashville.

Institutional Resilience and Public Spending

While the private sector is being picky, the public sector is finally putting those infrastructure bills to work. We saw a flurry of healthcare projects hit the planning phase in October.

Why now?

Because the planning cycle for a major hospital is long. Extremely long. The projects we see entering the Dodge Momentum Index October 2025 were likely conceived during the height of the pandemic’s stress on the system. It takes years to get the permits and the financing lined up for a $500 million medical campus. We’re seeing those finally cross the finish line into the "official planning" stage.

Education also saw a bump. It’s not just new schools; it’s massive renovations. K-12 districts are upgrading HVAC and security systems across the board. It’s consistent work. It’s boring, maybe, compared to a glass-walled skyscraper, but it’s what’s keeping the index from dipping.

Understanding the Lag

There is always a gap.

The DMI leads actual construction spending by a year or more. So, when we see this October growth, we aren't seeing cranes on the horizon today. We’re seeing the intentions of developers who are betting on the economy of 2026 and 2027.

They seem... cautiously optimistic?

If they were terrified, the index would be plummeting. Instead, it’s grinding higher. It’s a "grind-up" market. Honestly, that’s probably healthier than the boom-bust cycles we’ve seen in the past decade. It gives the supply chain a chance to breathe. Copper prices and lumber costs are still volatile, and a slower planning pace allows contractors to price jobs without losing their shirts.

Regional Variations: Not All Dirt is Equal

If you look at where these October projects are located, the "Smile States" are still winning. The Southeast and the Southwest dominate the planning activity.

- Texas is still a juggernaut for both data centers and healthcare.

- Arizona has a massive pipeline of semi-conductor related industrial planning (though this sometimes blurs the line between industrial and commercial).

- The Northeast is seeing a surprising amount of "adaptive reuse" planning. Think old malls being turned into outpatient clinics.

One thing that surprised some analysts about the Dodge Momentum Index October 2025 was the uptick in the Midwest. It turns out, when you need massive amounts of water and relatively cheap land for data centers, places like Ohio and Iowa start looking really attractive.

What This Means for Your Business

If you’re a developer, architect, or sub-contractor, you’ve got to read between the lines of these Dodge reports.

👉 See also: The Foundry Lake Havasu: What This Real Estate Shift Means for the Neighborhood

Stop waiting for the "General Commercial" market to return to 2019 levels. It’s not happening. The office market has fundamentally changed. The warehouse market has matured. The growth—the real momentum—is in the niche.

You should be looking at:

- Healthcare Infrastructure: Specifically outpatient and specialized surgery centers.

- AI-Ready Data Centers: These require totally different power and cooling specs than the ones built five years ago.

- Public-Private Partnerships: Especially in the education sector.

The Dodge Momentum Index October 2025 confirms that the "easy money" phase of construction is over. Now, it’s about the "smart money" phase. Developers are only moving forward with projects that have a guaranteed, high-yield tenant or a desperate public need.

The Financing Reality

We can't talk about October 2025 without mentioning the banks.

Lending standards stayed tight through the fall. Even as the Fed toyed with the dial, regional banks—the lifeblood of commercial construction—remained skittish. This created a bottleneck. There are likely thousands of projects that should be in the index but aren't because they can't get that final 20% of financing.

This creates a "shadow pipeline."

Once the banking sector feels more comfortable, we might see a sudden, vertical spike in the DMI. But for now, we’re seeing the projects that are "too good to fail"—the ones with bulletproof balance sheets.

Moving Forward into 2026

As we wrap up the analysis of the Dodge Momentum Index October 2025, the takeaway is clear: stability is the new growth. We aren't seeing a crash. We aren't seeing a rocket ship. We are seeing a mature, cautious industry that is slowly pivoting away from retail/office and toward tech/health.

Keep an eye on the November and December numbers to see if this institutional growth holds. If the public sector keeps spending while the private sector picks up the slack in data centers, 2026 is going to be a very busy year for anyone with a hard hat.

Actionable Insights for Construction Professionals:

- Diversify into Institutional: If your portfolio is 90% retail or light industrial, start bidding on municipal or healthcare renovations. The DMI shows this is where the sustained volume is.

- Audit Your Tech Capabilities: Data center projects entering the planning phase now require BIM (Building Information Modeling) and LEED certifications that are more stringent than ever.

- Watch Interest Rates, but Don't Rely on Them: The October data proves that projects are moving forward despite higher-than-average rates. Build your pro-formas based on current reality, not a "hoped-for" rate cut.

- Focus on the "Mid-Sized" Gap: While "mega-projects" (over $500 million) get the headlines, the DMI shows a healthy flow of $25–$50 million projects in the education and medical sectors. These often have less competition and better margins.