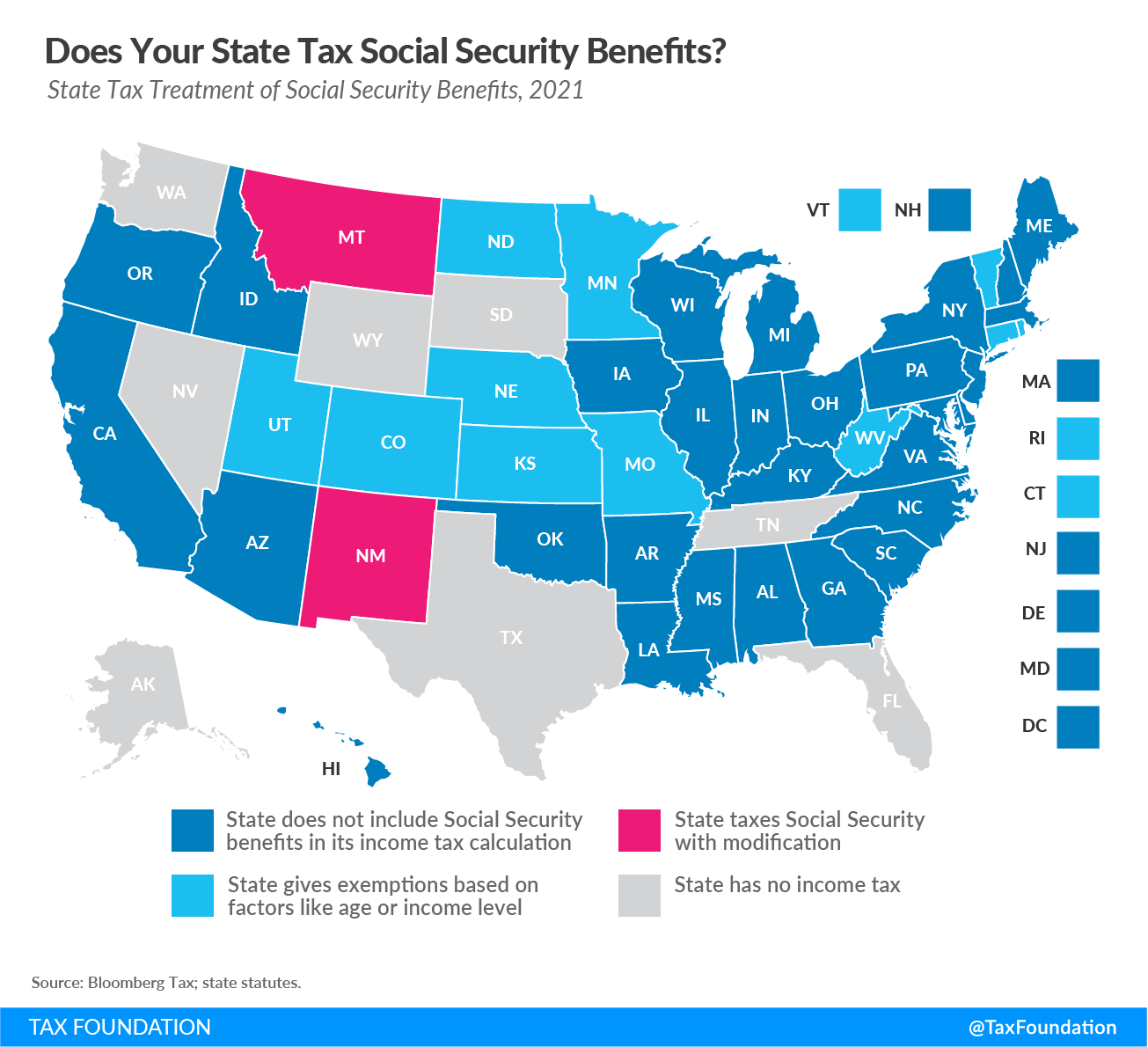

It is a crisp morning in the Hudson Valley, and you're sitting there with a cup of coffee, looking at your retirement statement. You see the federal government taking its bite out of your Social Security check, and you start to wonder. Does the Empire State do the same? New York has a reputation for being, well, expensive. High property taxes, high sales taxes, and those legendary income tax brackets. But here is the shocker that usually makes people double-check their screens: New York State does not tax Social Security benefits. Period.

Whether you are pulling in a modest monthly check or you’ve maxed out your lifetime earnings, the state of New York treats that Social Security income as completely off-limits. Honestly, it’s one of the most generous parts of the state’s tax code. While the IRS might be hovering over 50% or even 85% of your benefits depending on your "combined income," Albany just stays out of it.

The Reality of Does NYS Tax Social Security Benefits

If you've been living in New York for a while, you know the drill. You pay for the convenience of the city or the beauty of the Finger Lakes. But when it comes to your Social Security, the state allows a full subtraction. This applies to everyone. It doesn't matter if you’re a billionaire in a Manhattan penthouse or a retiree in a quiet Buffalo suburb.

How does it work on the actual paperwork? Basically, when you fill out your New York State return (Form IT-201), you start with your federal adjusted gross income (AGI). Since the feds often include a portion of your Social Security in that number, New York lets you pull it right back out. You use a "subtraction modification." It’s a fancy way of saying you get to ignore that income for state tax purposes.

This isn't just for retirement benefits, either.

🔗 Read more: 200 Euros to USD: Why the Mid-Market Rate Is Lying to You

- Disability benefits through Social Security? Tax-free in NY.

- Survivor benefits for a spouse? Tax-free in NY.

- Supplemental Security Income (SSI)? Never taxed federally, and certainly not by the state.

It is a rare win for the taxpayer in a state that usually wants a piece of everything.

Wait, What About My Other Retirement Income?

Now, this is where people get tripped up. Just because Social Security is safe doesn't mean your 401(k) or your private pension is in the clear. New York isn't that relaxed.

If you are 59.5 or older, New York gives you a "Pension and Annuity Exclusion." This is a big one. You can exclude up to $20,000 of your qualified retirement income from your state taxes every year. That includes money from an IRA, a 401(k), or a private employer pension.

If you're married and filing jointly, and you both have retirement income, you both get that $20,000 exclusion. That’s $40,000 total. You basically get to shield a decent chunk of change before the state tax man even looks at you.

But there’s a catch with the "public" stuff. If you have a pension from New York State, a local NY government, or the federal government (including military pensions), that money is completely exempt from New York State and local taxes. No $20,000 limit. No age requirement of 59.5. It’s just... gone. You don't pay state tax on it.

It’s a bit of a tiered system:

- Social Security: 100% Tax-Free for everyone.

- NY Public Pensions: 100% Tax-Free for everyone.

- Private Pensions/IRAs: First $20,000 Tax-Free (if you're 59.5+).

Why the IRS Still Bothers You

It's frustrating. You see "tax-free" in New York, but your bank account still looks a little light. That is because the federal government uses a different playbook. As of 2026, the federal thresholds for taxing Social Security haven't changed in decades. They aren't adjusted for inflation.

Basically, if your "combined income" (which is your AGI + nontaxable interest + half your Social Security) is over $25,000 for a single filer or $32,000 for a couple, the IRS starts taking a cut. In 2026, with the cost-of-living adjustments (COLA) pushing benefit amounts higher, more people than ever are hitting these "tax torpedo" thresholds.

You might pay federal tax on up to 85% of your benefits. But when you file that NYS return, remember that those federal rules don't migrate north to Albany. You get that money back in the eyes of the state.

The 2026 Landscape and Moving Out

Kinda makes you want to stay in New York, right? Well, maybe.

While the income tax situation for retirees is actually pretty solid, New York still ranks as one of the most expensive states for other things. Property taxes in places like Westchester or Nassau County are enough to make anyone’s eyes water. And the sales tax is no joke either.

People often talk about "Florida or bust" because Florida has no state income tax at all. But if you're a New Yorker whose primary income is Social Security and a small pension under $20,000, your state income tax bill is already basically zero. You have to weigh the property tax savings against the lifestyle you want.

Also, keep in mind that if you move, these benefits don't always follow you. If you receive a New York State government pension, it remains tax-free in New York even if you live in another state—but that other state (like North Carolina or Georgia) might decide to tax it themselves.

Actionable Steps for New York Retirees

Don't just take the "tax-free" news and sit on it. You can actually optimize this.

First, check your withholding. If you’re paying New York State tax on your Social Security right now because of how your payroll or pension company is set up, you are essentially giving the state an interest-free loan. You don't owe them that money. Adjust your state withholding to reflect the fact that your Social Security is exempt.

Second, timing matters for that $20,000 exclusion. If you turn 59.5 in the middle of the year, you can only exclude the money you received after your birthday. Planning your big IRA withdrawals for the later half of the year you turn 60 can save you thousands in state taxes.

Third, look at the STAR program. Since you're likely staying in NY for the tax-free Social Security, make sure you're enrolled in the School Tax Relief (STAR) program. If you're 65 or older and meet the income requirements, you might qualify for Enhanced STAR, which provides a much larger reduction in your school property taxes.

Finally, keep an eye on the Senior Citizen Homeowners' Exemption (SCHE). If your income is below certain levels (often around $58,000 depending on the municipality), you could get a 5% to 50% reduction in your property’s assessed value.

New York is a complex place to grow old, but the tax code is surprisingly kind to your Social Security check. Just make sure you aren't leaving money on the table by overpaying on the stuff the state doesn't even want.