Tax season is a beast. Honestly, nothing kills the buzz of a successful investment quite like the realization that Uncle Sam wants his cut. If you’ve held an asset—like a stock, a piece of real estate, or even a vintage car—for more than a year, you’re looking at long-term rates. But trying to estimate long term capital gains tax before you sell is a move that separates the amateurs from the pros. It’s the difference between a massive surprise bill and a calculated financial victory.

Most people think it’s a flat rate. It isn't. Not even close.

🔗 Read more: Quaker Oats Class Action Lawsuit: What Really Happened and Why It Matters

The reality is a messy, overlapping Venn diagram of your annual income, your filing status, and some weirdly specific thresholds that change almost every year. For 2024 and 2025, those thresholds have shifted again to account for inflation. If you’re not looking at the current numbers, your math is already wrong.

The Zero Percent Myth and the Reality of Income Brackets

You might have heard that some people pay 0% on their gains. That’s actually true. It’s not a loophole for the ultra-wealthy; it’s actually a benefit for those in the lower-income tiers. If your total taxable income—including the gain—is under a certain limit, you might owe nothing.

For 2024, if you’re filing as a single person and your total taxable income is below $47,025, that 0% rate is yours. Married filing jointly? You get that 0% rate up to $94,050. This is where people get tripped up. They think if they make $40,000 at their job and sell a stock for a $20,000 profit, the whole $20,000 is tax-free. Nope. The "stacking" rule means your gain sits on top of your regular income. Some of that gain might be taxed at 0%, while the rest pushes into the 15% bracket.

It’s a sliding scale. Basically, once you cross that $47,025 mark (for singles), the IRS takes 15%. Most of the American middle class lives in this 15% zone. It’s a wide range that goes all the way up to $518,900 for single filers in 2024. If you’re doing better than that, you’re hitting the 20% ceiling.

Why You Must Calculate Your Cost Basis First

You can't even begin to estimate long term capital gains tax without a rock-solid cost basis. This is where most DIY tax prep falls apart. The cost basis isn’t just what you paid for the asset. It’s the purchase price plus commissions, fees, and—in the case of real estate—certain improvements.

Real Estate: A Different Kind of Math

Let’s talk about that "fixer-upper" you sold. If you bought a house for $300,000 and sold it for $500,000, you don't necessarily have a $200,000 gain. Did you put $50,000 into a new roof and a kitchen remodel? That gets added to your basis. Now your basis is $350,000, and your taxable gain is only $150,000.

But wait. There's the Section 121 exclusion. If it was your primary residence for at least two of the five years before the sale, you can exclude up to $250,000 of gain (or $500,000 if married). Many people worry about capital gains on their home sale when they don't even owe a dime. On the flip side, if it was a rental property, you have to deal with "depreciation recapture." The IRS essentially says, "Hey, we let you take tax breaks for the wear and tear on that building for years, now we want some of that back." That's taxed at a flat 25%. It’s brutal.

Stocks and the Wash Sale Trap

With stocks, it’s usually simpler because your brokerage tracks it. But what if you’ve been reinvesting dividends? Each of those reinvestments is a new purchase with a new "lot" and a new basis. If you sell "Average Cost," you might be paying more than if you specifically identified the shares with the highest basis.

Also, be careful with the Wash Sale rule. If you sell a stock at a loss to offset a gain (tax-loss harvesting), but buy it back within 30 days, that loss is disallowed. You can't use it to lower your bill.

The Hidden 3.8% Tax Nobody Mentions

If you’re a high earner, the 20% cap isn’t actually the cap. There’s a sneaky little thing called the Net Investment Income Tax (NIIT). This came out of the Affordable Care Act. It adds an extra 3.8% on top of your capital gains if your Modified Adjusted Gross Income (MAGI) exceeds $200,000 for individuals or $250,000 for couples.

So, if you’re in the top bracket, your "20% tax" is actually 23.8%.

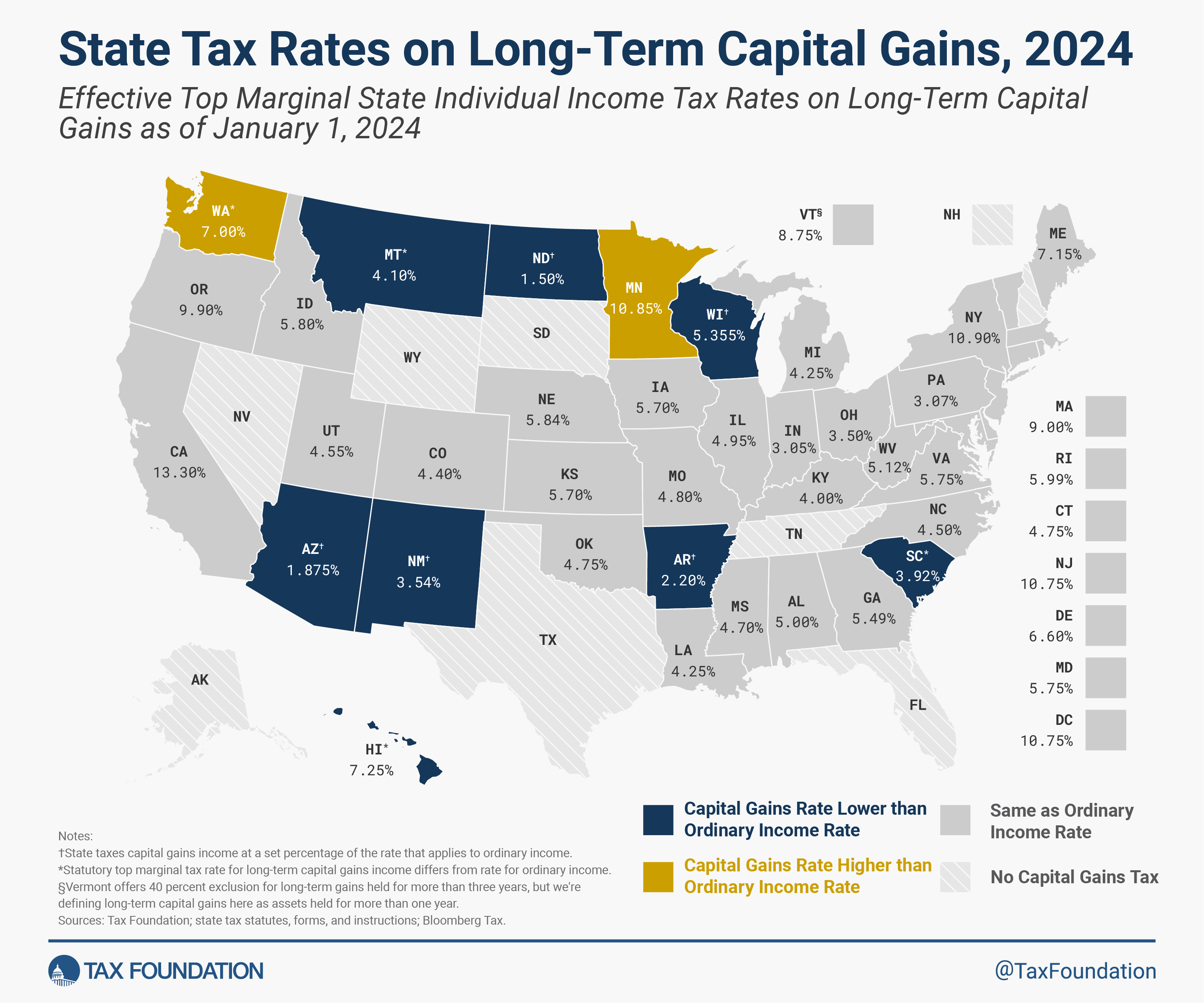

And don't forget the state. Unless you live in a place like Florida, Texas, or Washington (though Washington now has its own specific high-earner capital gains tax), your state wants a piece too. California, for instance, treats capital gains as regular income. That can add another 1% to 13.3% to your total bill. Suddenly, your "long-term" advantage doesn't feel so advantageous.

How to Estimate Long Term Capital Gains Tax Without a Calculator

You don't need fancy software for a rough "back of the napkin" estimate. Here is how I’d do it if a friend asked:

First, find your "Net Gain."

Selling Price - (Purchase Price + Costs of Sale) = Net Gain.

Second, figure out where that gain sits on your income "ladder."

Look at your regular salary. Does it already put you over $47,025 (single)? If yes, you’re at least in the 15% bracket. If your salary is already over $518,900, you’re in the 20% bracket.

Third, multiply the gain by the rate.

If you have a $50,000 gain and you’re in the 15% bracket, expect to pay $7,500.

Fourth, check for state taxes.

If your state tax rate is 5%, add another $2,500.

Total estimate: $10,000.

It’s a gut-punch, but knowing it ahead of time allows you to set that money aside in a high-yield savings account so it earns you interest before you hand it over to the government.

Strategies to Lower the Bill Before the Year Ends

Tax planning isn't just for the 1%. You have moves you can make.

Tax-Loss Harvesting is the big one. If you have a dog of a stock that’s down $10,000, selling it can offset $10,000 of your gains. If your losses exceed your gains, you can even use $3,000 of the excess to offset your regular "W-2" income.

Charitable Donations are another route. Instead of giving cash to a charity, give them the actual appreciated stock. If you give a stock worth $10,000 that you bought for $2,000, the charity gets the full $10,000, you get a tax deduction for the full $10,000, and nobody ever pays the capital gains tax on that $8,000 growth. It’s one of the cleanest wins in the tax code.

Holding Periods matter more than you think. I've seen people sell an asset at 364 days. They paid their ordinary income tax rate (which could be 37%) instead of the long-term rate (which might be 15%). One single day difference could cost you tens of thousands of dollars. Always double-check your trade dates.

State-Specific Weirdness

States are getting aggressive. For a long time, state capital gains taxes were just a percentage of the federal amount or followed the federal rules. Recently, states like Washington have implemented standalone capital gains taxes targeting high-value sales (specifically stocks and bonds, excluding real estate).

Massachusetts recently added a "millionaire's tax" surtax. If you sell a business or a high-value property in a state with these rules, your estimate long term capital gains tax could be significantly higher than a standard online calculator suggests. You have to check the local department of revenue site for the state where you reside, not just where the asset is located.

Actionable Steps for Your Next Move

Knowing the numbers is only half the battle. To actually protect your wealth, you need a workflow.

- Audit your holding period: Log into your brokerage and look at the "Tax Lot" screen. Ensure everything you plan to sell is marked "Long-Term." If it’s "Short-Term," wait.

- Calculate your 2024 MAGI: You need to know if you're hitting that 3.8% NIIT threshold. If you’re close, consider contributing more to a 401(k) or traditional IRA to lower your MAGI.

- Look for offsets: Do you have "carryover losses" from previous years? Check last year's Tax Form 1040, Schedule D. You might have a "hidden" tax shield waiting to be used.

- Set aside the cash: Do not reinvest 100% of your proceeds. If you sell $100,000 of stock for a $50,000 profit, put at least $7,500 to $12,000 in a separate account immediately.

- Consult a pro for complex assets: If you are selling a partnership interest (K-1), a business, or a rental property with depreciation, an online article isn't enough. These involve "recapture" rules that can tax your gains at up to 25% or 28% (for collectibles).

Tax laws aren't static. They change with every new piece of legislation out of D.C. While the current 0/15/20 structure is the law of the land for now, always verify the specific income thresholds for the year you are actually filing, as they are adjusted for inflation every January. Keeping a pulse on these shifts is the only way to truly master your financial outcome.