Tax season is usually just a giant headache. Most of us spend the year ignoring the IRS until that first W-2 or 1099 hits the mailbox in January, and then it’s a mad scramble to figure out if we’re getting a refund or if we need to sell a kidney. Honestly, getting a solid estimate of total tax liability for 2024 shouldn’t be that stressful, but the tax code is written in a way that feels like it’s designed to confuse humans.

You’ve probably heard people use "tax liability" and "taxes owed" interchangeably. They aren't the same. Your total tax liability is the total amount of tax you owe the government based on your income, capital gains, and self-employment earnings before you account for the payments you already made through withholding. If your employer took out $10,000 and your liability is $12,000, you owe two grand. Simple math, right? Well, sort of.

🔗 Read more: Why the Bank of America Mobile App Actually Matters for Your Money

Why 2024 Tax Brackets Are Changing Your Math

The IRS isn't always the villain. Because of high inflation over the last couple of years, they actually bumped up the tax brackets and standard deductions for the 2024 tax year. This is a big deal. It means you can earn more money before hitting a higher tax percentage.

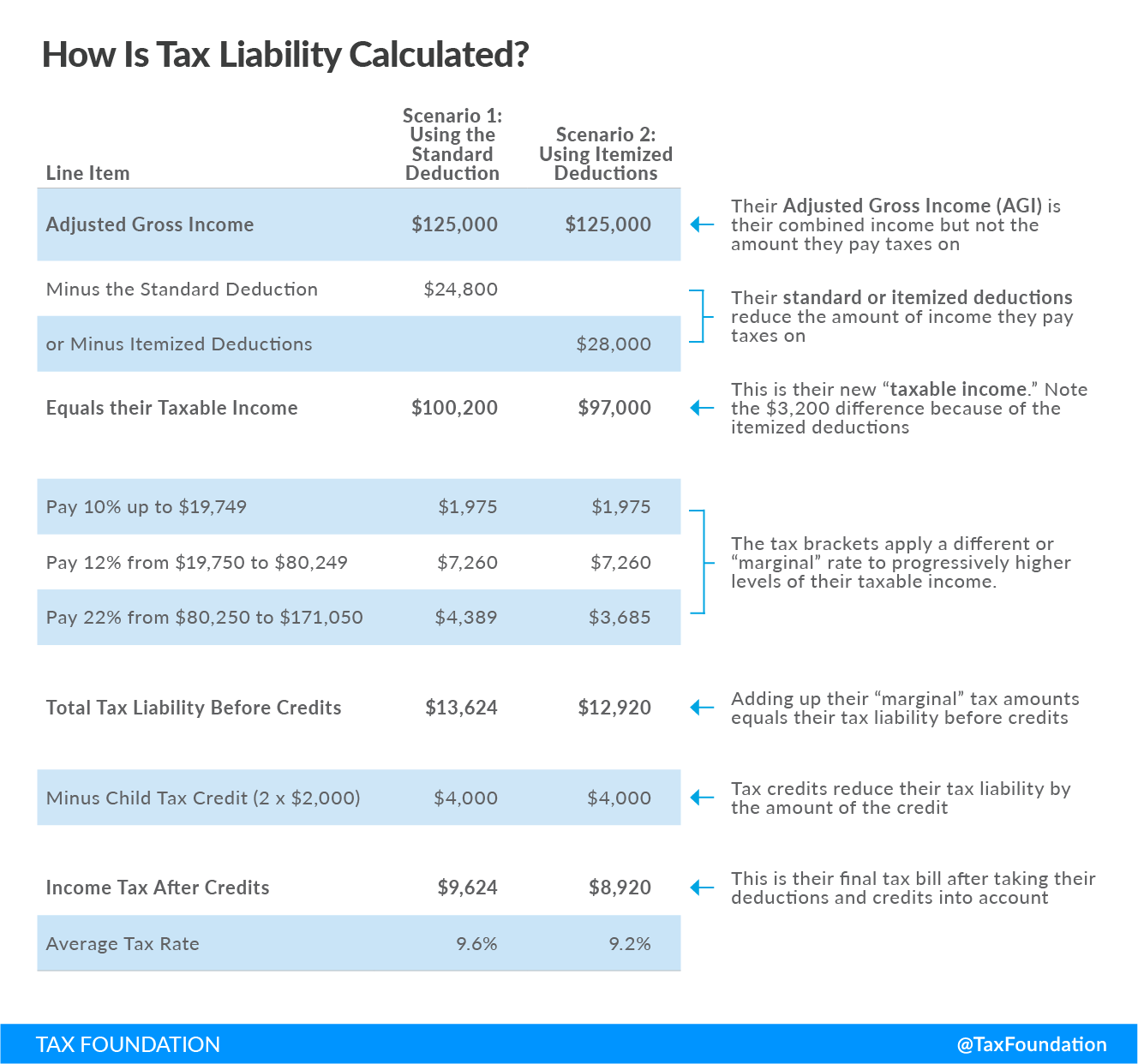

For the 2024 tax year (the return you file in early 2025), the standard deduction jumped to $14,600 for individuals and $29,200 for married couples filing jointly. That is a significant chunk of change that the government just ignores before they even start calculating what you owe. If you’re trying to calculate an estimate of total tax liability for 2024, start by lopping that number off your gross income.

The Percentages That Matter

We have a progressive tax system. This means you don't pay one flat rate on everything. It’s a ladder. You pay 10% on the first chunk, 12% on the next, and so on. For 2024, those brackets are 10%, 12%, 22%, 24%, 32%, 35%, and 37%.

Most middle-class earners live in the 12% to 22% range. If you're a single filer making $60,000, you aren't paying 22% on the whole $60k. You’re paying 10% on the first $11,600, then 12% on the income up to $47,150, and only then do you pay 22% on the remaining sliver. People get this wrong all the time. They think a raise will "put them in a higher bracket" and they'll take home less money. That is a total myth. You only pay the higher rate on the dollars inside that specific bracket.

Credits vs. Deductions: The Real Difference-Makers

If you want to lower your estimate of total tax liability for 2024, you need to know the difference between a deduction and a credit. A deduction, like the standard deduction or mortgage interest, lowers the amount of income the IRS looks at. A credit is way better. A credit is a dollar-for-dollar reduction in the actual tax you owe.

Take the Child Tax Credit. For 2024, it’s generally $2,000 per qualifying child. If your total tax liability is $5,000 and you have two kids, your bill just dropped to $1,000. That’s powerful. There’s also the Earned Income Tax Credit (EITC) for lower-to-moderate-income workers, which can be worth thousands depending on your family size.

💡 You might also like: Why the Vaca Muerta Imagine Projects are Changing Argentina’s Energy Future

Then there are the "green" credits. If you bought an electric vehicle in 2024 or put solar panels on your roof, you’re looking at some of the biggest tax breaks available. The Clean Vehicle Credit can be up to $7,500. That doesn't just lower your taxable income; it wipes out $7,500 of the debt you owe Uncle Sam.

Self-Employment and the "Hidden" Tax

If you’re a freelancer or a side-hustler, your estimate of total tax liability for 2024 is going to look a lot different than someone with a 9-to-5. When you work for a boss, they pay half of your Social Security and Medicare taxes. When you are the boss, you pay both halves. This is the Self-Employment Tax, and it sits at 15.3%.

It catches people off guard every single year.

You might calculate that you owe $5,000 in federal income tax, but then you realize you owe another $4,000 in self-employment tax. Suddenly, your "total liability" has nearly doubled. To avoid a massive shock, you should be setting aside at least 25-30% of every check you get from a client. It hurts, but it’s better than a surprise bill from the IRS that you can't pay.

Capital Gains: The Silent Partner

Did you sell some stock this year? Maybe some Bitcoin? If you held it for more than a year, you get the "long-term capital gains" rate, which is usually 0%, 15%, or 20% depending on your total income. Most people fall into the 15% camp. If you sold it in less than a year, it’s taxed just like your regular paycheck. This is why "day trading" is often a tax nightmare compared to "buy and hold" investing.

Calculating Your Estimate of Total Tax Liability for 2024

To get a real number, you have to be honest about your "Adjusted Gross Income" (AGI). This is your total income minus things like student loan interest payments, IRA contributions, or health savings account (HSA) contributions.

- Add up all income: Salary, bonuses, freelance gigs, interest from your savings account.

- Subtract "Above-the-line" deductions: HSA contributions are huge here.

- Subtract your Standard Deduction: $14,600 (Single) or $29,200 (Married).

- Apply the Tax Brackets: Calculate the 10%, 12%, etc., based on what’s left.

- Add Self-Employment Tax: If applicable.

- Subtract Tax Credits: Child tax credit, EV credits, energy-efficient home credits.

What’s left is your estimate of total tax liability for 2024.

Don't Forget the States

We’ve been talking about federal taxes, but unless you live in a place like Florida, Texas, or Washington, your state wants its cut too. State tax rates vary wildly. California can go up to 13.3%, while states like Pennsylvania have a flat rate around 3.07%. Your total tax liability to the government as a whole is the sum of both.

Common Pitfalls to Avoid

The biggest mistake people make is forgetting about "phantom" income. This is stuff like gambling winnings, forgiven debt, or even prizes you won on a game show. The IRS considers almost everything income. If you won $1,000 at a casino, that goes into the bucket.

Another big one? Not adjusting your withholding. If you got married, had a kid, or bought a house in 2024, your 2023 tax return is a bad map for your 2024 journey. You need to look at your most recent pay stub. Look at the "Fed Tax YTD" (Year to Date) line. If that number isn't on track to hit your estimated liability by December 31st, you’re going to owe money in April.

Actionable Steps for the Remainder of the Year

You still have time to influence your estimate of total tax liability for 2024 before the year ends. Tax planning isn't just for rich people with lawyers; it's for anyone who wants to keep more of their paycheck.

- Max out your 401(k) or 403(b): Contributions to traditional employer-sponsored plans lower your taxable income dollar-for-dollar. If you can swing an extra $500 before the final paycheck of December, do it.

- Fund your HSA: If you have a high-deductible health plan, the HSA is the "triple threat" of tax savings. The money goes in tax-free, grows tax-free, and comes out tax-free for medical expenses.

- Harvest your losses: If you have stocks that are currently in the red, you can sell them to offset the gains you made on other investments. You can even use up to $3,000 of investment losses to offset your regular salary income.

- Keep your receipts: If you are self-employed, every business-related expense is a deduction. That new laptop, the portion of your internet bill used for work, and even the miles you drove to meet a client—it all adds up to a lower tax bill.

- Check your withholding: Use the IRS Tax Withholding Estimator tool online. It’s free. It’ll tell you exactly how to fill out a new W-4 for your employer so you don't end up with a massive bill or a massive refund (which is basically just giving the government an interest-free loan).

Tax liability is a moving target. By keeping an eye on your brackets and taking advantage of credits, you can turn a scary number into something manageable.