Let’s be real. Nobody actually wants to spend their Saturday morning staring at a dashboard on StudentAid.gov. It’s dense. It’s confusing. Honestly, it’s enough to make you want to close your laptop and pretend your debt doesn't exist. But ignoring a federal student loan repayment plan is basically leaving money on the table, or worse, letting interest eat your future bank account alive.

The system has changed more in the last three years than it did in the previous thirty. We’ve seen the rise and fall of various forgiveness programs, the birth of the SAVE plan, and a mountain of legal challenges that have left even the smartest people scratching their heads. If you feel out of the loop, you’re definitely not alone.

Most people think choosing a plan is a "one and done" deal. You pick it, you set up autopay, and you forget it until the heat death of the universe. That is a massive mistake. Your life changes. Your income fluctuates. The government changes the rules every time there’s a new administration. Understanding the nuance of these plans is the difference between a $0 monthly payment and a $600 nightmare.

The SAVE Plan Chaos and Why It Still Matters

So, let's talk about the elephant in the room: the Saving on a Valuable Education (SAVE) plan. It replaced REPAYE and was supposed to be the "holy grail" of income-driven repayment. Then, the courts stepped in. Currently, there’s a massive legal tug-of-war happening, and if you’re enrolled, you might be in an interest-free administrative forbearance.

It’s weird.

One day it’s the law of the land, the next day a judge in Missouri or Kansas says "hold on." But the core mechanics of why SAVE was created still tell us a lot about where the Department of Education wants things to go. Under SAVE, the amount of income protected from repayment was raised to 225% of the Federal Poverty Line. For a single person, that means if you make roughly $33,885 or less, your payment is $0. Period.

Even better? The interest subsidy. This was the real game-changer. On older plans, if your payment didn't cover the monthly interest, your balance grew. You’d owe $50,000, pay for five years, and suddenly owe $55,000. It felt like running up a down escalator. SAVE was designed to stop that. If you owe $100 in interest but your payment is $30, the government just... deletes the other $70.

While the courts hash out the future of SAVE, the lesson remains: federal student loan repayment plan selection is now a political football. You have to stay agile. If SAVE gets struck down permanently, millions will likely be shifted back to the older IBR (Income-Based Repayment) or ICR (Income-Contingent Repayment) models.

📖 Related: Rowan University Tuition and Fees: What Most People Get Wrong

Is the Standard 10-Year Plan a Trap?

When you graduate, the government defaults you into the Standard Repayment Plan. Ten years. Fixed payments. It sounds clean. Simple.

It’s also often the most expensive way to live your life in your 20s.

Sure, you pay the least amount of interest over time because you’re aggressive. That’s the math. But math doesn't care about your rent in Austin or your car insurance or that wedding you have to travel for in October. For a lot of people, the Standard Plan is a debt-to-income ratio killer. If you’re trying to buy a house, a high fixed student loan payment can tank your mortgage application.

Compare that to an Income-Driven Repayment (IDR) plan. These look at what you actually make, not what you owe.

Here is how the math usually shakes out:

- Standard 10-Year: High monthly cost, low total interest, no forgiveness.

- Graduated Repayment: Starts low, increases every two years. Good if you're a resident or a junior associate expecting a massive jump in pay, but dangerous if your career plateaus.

- Extended Repayment: Pushes the term to 25 years. Lower payments, but you will pay a fortune in interest. It’s basically the "I need to breathe right now" option.

The Public Service Loan Forgiveness (PSLF) Secret

If you work for a 501(c)(3) non-profit, the government, a public school, or even certain tribal organizations, you shouldn't just be looking for a plan—you should be looking for an exit strategy.

PSLF is real, and after a disastrous start years ago where 99% of people were rejected, it actually works now. The Department of Education has processed billions in discharges. The catch? You must be on an IDR plan. If you stay on the Standard 10-Year plan while working for a non-profit, you’ll pay off the loan in 10 years anyway, leaving $0 to be forgiven.

You need to match the right federal student loan repayment plan with your employer. This requires certifying your employment every single year. Don't wait until year ten. That’s how paperwork nightmares are born. Use the PSLF Help Tool on the federal website. It’s the only way to be sure your employer actually qualifies.

When to Consider Consolidating (and When Not To)

Consolidation is often confused with refinancing. They aren't the same.

Refinancing happens with private banks like SoFi or Laurel Road. Once you do that, your federal loans are gone. You lose the death and disability discharge, the IDR options, and the possibility of forgiveness. Never refinance federal loans unless you have a massive income, incredible credit, and zero interest in government protections.

Consolidation, however, is a federal process. It takes your various loans (Stafford, Perkins, PLUS) and rolls them into one Direct Consolidation Loan.

Why bother?

Well, if you have older FFEL loans held by commercial lenders, they don’t qualify for SAVE or PSLF. You have to consolidate them into the Direct Loan program to get the good stuff. But be careful. Under old rules, consolidating wiped out your progress toward forgiveness. Thankfully, the "IDR Account Adjustment" fixed a lot of that, but that window is closing.

The "Tax Bomb" No One Mentions

Here is a bit of honesty: if you are on a 20 or 25-year IDR plan, and you get your balance forgiven at the end, the IRS might come knocking.

Historically, forgiven debt is treated as taxable income. If the government forgives $100,000 of your debt in 2040, they might act like you earned an extra $100,000 that year. You’d owe a massive tax bill.

Currently, thanks to the American Rescue Plan, federal student loan forgiveness is tax-free at the federal level through the end of 2025. Will Congress extend that? Maybe. Will they let it expire? Also maybe. This is the "nuance" that most "Ultimate Guides" won't tell you. You have to plan for the possibility of a tax bill two decades from now. Some states, like Mississippi or Indiana, might even try to tax it at the state level even if the feds don't.

✨ Don't miss: Other Words for Director: Why Context Changes Everything

Parent PLUS Loans: The Hardest Level of the Game

If you’re a parent who took out loans for your kid, I’m sorry. You have the fewest options.

Parent PLUS loans aren't eligible for the best IDR plans directly. They are stuck in the "Standard" or "Extended" plans unless you do the "Double Consolidation Loophole." It’s a complex process of consolidating some loans, then others, then consolidating the consolidations to trick the system into seeing the debt as a standard consolidation loan rather than a Parent PLUS loan.

It’s legal. It’s also tedious. But it can drop a payment from $1,200 to $200. If you’re a parent nearing retirement, this isn't just a tip—it’s a survival strategy.

Actionable Steps to Take Right Now

Stop guessing. Start acting.

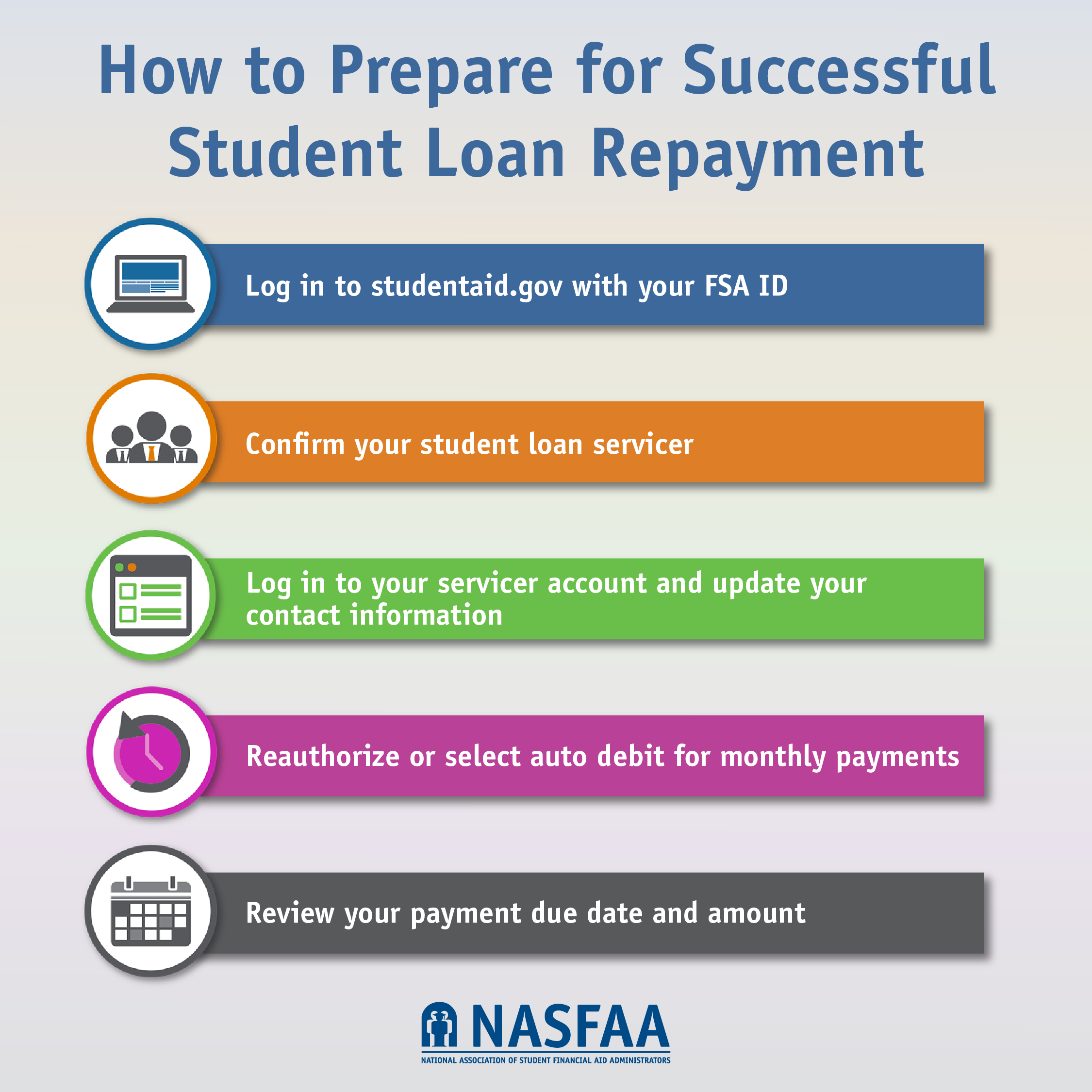

First, log into StudentAid.gov. Look at your loan types. If you see "FFELP" or "Perkins," you are likely missing out on the newest repayment benefits.

Second, use the Loan Simulator tool. It’s actually decent. You can plug in your tax filing status (Married Filing Jointly vs. Separately makes a huge difference in your payment amount) and see your projected monthly cost across every plan.

📖 Related: Exchange Rate Peso Mexicano US Dollar: Why the Super Peso is Back in 2026

Third, re-certify your income early. You don't have to wait for the deadline. If you lost your job or took a pay cut, you can report that change immediately to lower your payment.

Finally, check your contact info. Loan servicers change constantly. If Mohela or Nelnet is trying to reach you about a transition and you’re using an old college Gmail account you haven't checked in years, you’re going to miss critical deadlines.

The goal isn't just to pay back the money. The goal is to manage your federal student loan repayment plan so it fits your life, not the other way around. Keep your documentation, watch the news for court rulings, and never assume the servicer has your best interests at heart. They are call centers; you are the manager of your own financial future.