Waiting for a paper check feels like living in the stone age. You've got bills hitting your account on the 1st, but your paycheck is currently sitting in a processing center three states away. It’s stressful. Honestly, if you're still walking to a physical branch or an ATM just to endorse a slip of paper, you're losing time. That’s why getting your direct deposit form PNC sorted out is probably the smartest ten-minute task you can do this week.

Most people think they need a specific, fancy document from the bank to make this happen. They spend twenty minutes digging through the PNC website or sitting on hold with customer service. Here’s the reality: you usually don't need a "special" form from the bank at all. Your employer just needs the numbers. But, if your HR department is old-school and insists on a signed document with a bank logo, PNC does provide a pre-filled PDF that makes you look like you have your life together.

Where to Actually Find the Form Without Losing Your Mind

If you log into the PNC mobile app, you’re not going to see a giant button that says "Direct Deposit Form" right on the home screen. That would be too easy. Instead, you've gotta dive into the account services section. Once you select your specific checking or savings account, look for "Account Options" or "Wallet Settings."

PNC basically gives you two ways to handle this. You can download a blank "Direct Deposit Sign-Up Form" directly from their public website—no login required for that one—or you can generate a pre-filled one through the Online Banking portal. The pre-filled version is a lifesaver because it automatically pulls your routing number and account number so you don't accidentally swap a 7 for a 1 and send your mortgage payment to a stranger in Ohio.

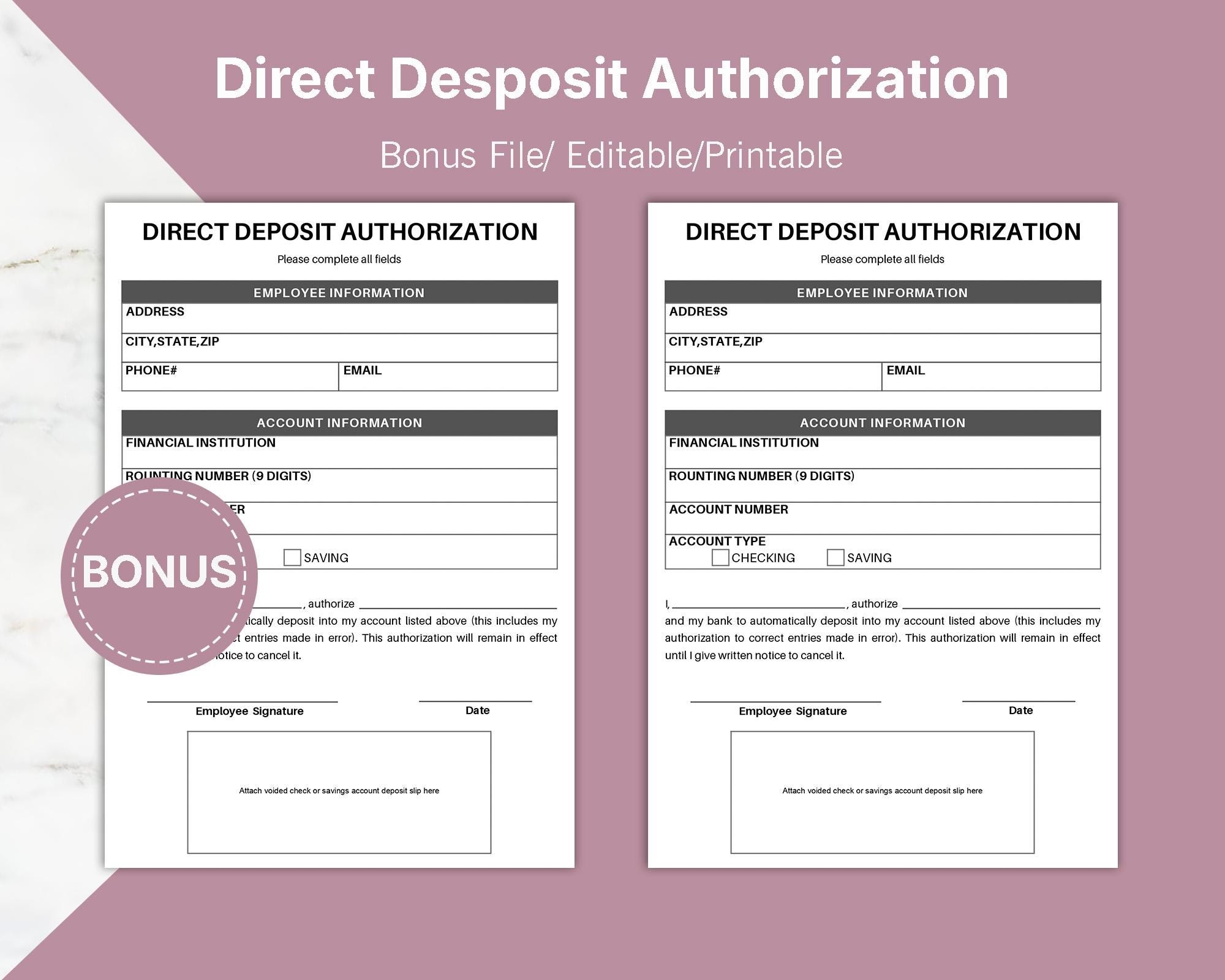

If you’re the type who prefers the paper route, you can just go to the PNC website, search for "Direct Deposit" in their help bar, and it’ll spit out a PDF. It’s a standard form. It asks for your name, your address, the bank’s name (PNC Bank, N.A.), and the type of account.

The Routing Number Trap

Here is where people mess up. PNC is a massive regional bank, and they’ve swallowed up a lot of smaller banks over the years (remember the BBVA merger?). Because of that, there isn't just one PNC routing number.

You cannot just Google "PNC routing number" and use the first nine-digit string you see. If you do that, your money might bounce back to your employer, and then you’re stuck waiting another two weeks for a manual override. Your routing number depends on where you opened the account. The safest bet? Look at the bottom left corner of your checks if you have them. If you don't have checks, look at your digital "Account Details" in the app. It will explicitly list the ACH routing number. Use that one. Don't guess.

Why Your Employer Might Reject Your Form

Sometimes you hand over the direct deposit form PNC provided, and HR kicks it back. Why? Usually, it's because they want a "voided check."

In 2026, nobody uses checks. It feels ridiculous to pay $25 for a book of 50 checks just so you can ruin one and give it to a payroll clerk. If you don't have a check, don't buy them. Most employers will accept a "Bank Authorization Letter" or a "Direct Deposit Authorization Letter" instead. You can print this directly from your PNC online dashboard. It’s an official document on bank letterhead that confirms you are, in fact, the owner of the account. It serves the exact same purpose as a voided check but costs you zero dollars.

Also, double-check your "Account Type." If you tell HR it’s a checking account but it’s actually a specialized savings or a "Virtual Wallet" Growth account, the transaction might fail depending on how your employer’s payroll software (like ADP or Workday) handles ACH transfers.

The Virtual Wallet Nuance

PNC is famous for its "Virtual Wallet" setup. This isn't just one account; it’s usually three: Spend, Reserve, and Growth.

- Spend: This is your primary checking. This is where 99% of people should direct their deposit.

- Reserve: This is for short-term goals.

- Growth: This is the long-term savings side.

Each of these has a different account number. If you want to split your pay—say, 80% to Spend and 20% to Growth—you’ll need to provide both account numbers to your employer. Most payroll systems allow for "partial deposits." It’s a great way to automate your savings before you ever have the chance to spend the money on takeout.

💡 You might also like: What Does Bulk Mean? The Messy Reality of Buying and Building Big

How Long Does the Switch Actually Take?

Don't expect your next paycheck to hit your PNC account tomorrow just because you handed in the form today. Payroll cycles are stubborn. Most companies require about one to two pay periods to "test" the connection. This is often called a "pre-note" process. The payroll system sends a $0.00 transaction to PNC just to make sure the pipes are connected properly.

If the pre-note clears, your next full check will go through. Keep an eye on your old account or be prepared to get one last paper check in the mail.

Moving Beyond the Form: Real-World Steps

Filling out the direct deposit form PNC offers is just the first move. To actually make this work for your financial health, you need to be proactive.

Verify the Routing Number: Log in to the PNC mobile app, tap on your "Spend" account, and click "Account Details." Copy that routing number exactly.

👉 See also: B and R Corvallis Oregon: The Truth About Fixing Your Car Without Getting Ripped Off

Download the Official PDF: If your HR needs a formal document, grab the PNC Direct Deposit PDF from their "Tools & Resources" page. It’s cleaner than a handwritten note.

Set Up Alerts: Once you submit the form, go into your PNC settings and turn on "Large Deposit" alerts. You’ll get a push notification the second your employer hits the "send" button on your pay.

Check for Fees: Some PNC accounts waive monthly maintenance fees if you have a certain amount of direct deposit coming in every month (like $500 or $2,000 depending on the account tier). Ensure your deposit meets that threshold so you aren't paying the bank to hold your own money.

Update Your Overdraft Protection: Once your direct deposit is landing in your PNC account, make sure your "Reserve" account is linked for overdraft protection. It’s a safety net that uses your own money instead of charging you a $36 fee for a $4 latte.

Direct deposit isn't just about convenience; it's about security. Paper checks get stolen. They get lost in the rain. They sit in mailboxes. Digital transfers are encrypted and, frankly, much harder to mess up once the initial paperwork is done correctly. Get the right numbers, give them to the right person, and stop worrying about the mailman.