Lightning capital of the world. That isn't just a catchy nickname for Florida; it’s a terrifying reality for your electronics. If you live in the Sunshine State, you’ve heard that specific, house-shaking crack that happens right as the lights flicker. You hope everything turns back on. Sometimes it doesn't. Most people think a $20 power strip from a big-box store is a shield. It’s not. It’s basically a placebo when a massive spike hits the lines. That is where Florida Power and Light surge protection programs, specifically FPL Home SurgeShield, come into the conversation.

Florida experiences more than 1.2 million lightning strikes a year. Think about that. Every single one of those strikes is a potential death sentence for your refrigerator, your dryer, or that brand-new OLED TV. Surge protection isn't just about the "big hit," though. It’s the small, silent surges—the ones caused by birds on a wire or a neighbor's AC kicking on—that slowly bake your circuit boards over time.

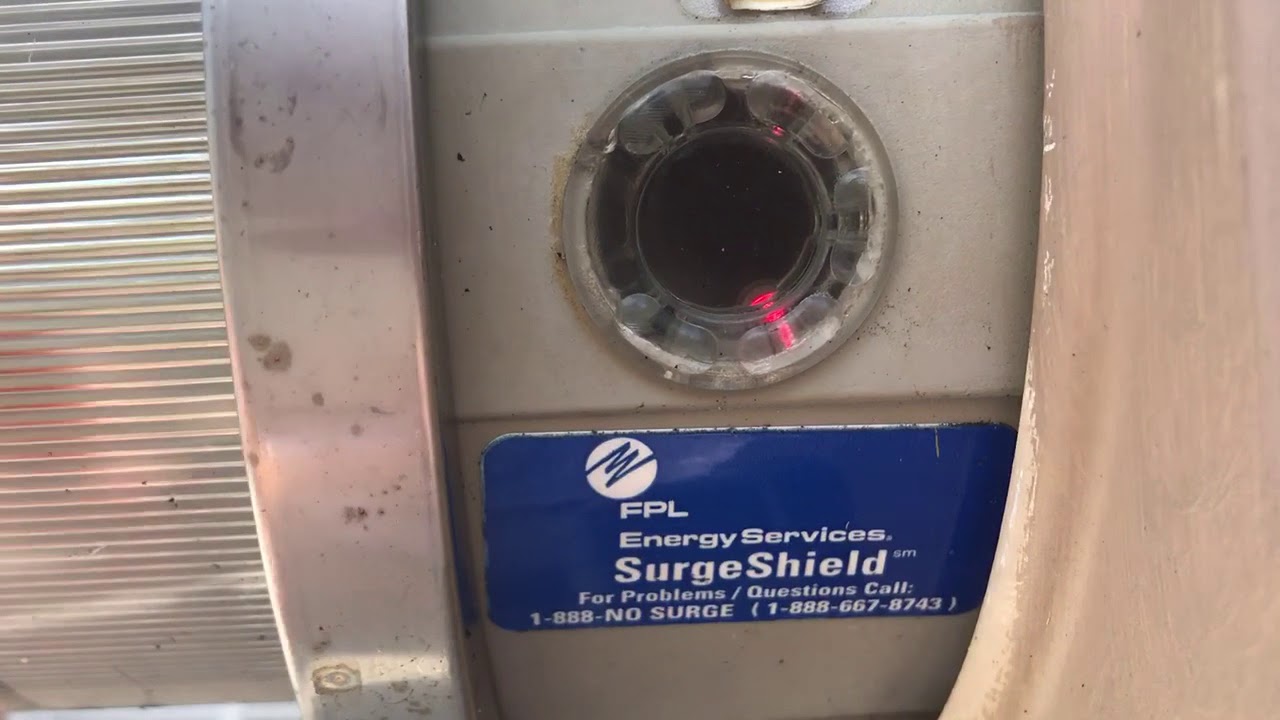

The Lowdown on FPL Home SurgeShield

Most folks get confused about who actually runs this. To be clear, FPL Home is an unregulated subsidiary of Florida Power & Light. They offer a product called SurgeShield. It’s a device installed directly at your electric meter. This is "primary" protection. It catches the surge before it ever enters your home's internal wiring.

It’s a different beast than the surge protector you plug into the wall. Wall units are "secondary" protection. If a massive spike comes down the utility line, a wall unit is often too slow or too weak to stop it. The SurgeShield device uses heavy-duty Metal Oxide Varistors (MOVs) to shunt that excess voltage into the ground.

What it Actually Covers (And What it Won't)

Let's get real about the fine print. People often sign up for Florida Power and Light surge protection thinking it’s an insurance policy for every gadget they own. It isn't. SurgeShield specifically targets "white goods." We are talking about your big-ticket appliances:

- Refrigerators and freezers

- Washers and dryers

- Dishwashers

- Water heaters

- Ceiling fans

- Range/Ovens

But here is the kicker. It generally does not cover things with "sensitive electronics" as the primary function if they aren't hardwired or fall into specific categories. Your laptop? Probably not covered by the base meter-based protection. Your $3,000 gaming rig? Nope. For those, you need the "Electronics Surge Protection" add-on. It’s a separate monthly fee. Honestly, it’s a bit of a shell game if you don't read the terms. You’ve got to know which bucket your device falls into before you try to file a claim.

The $5,000 Limit

There is a cap. Most of these plans cover up to $5,000 per occurrence. If a massive surge fries your $4,000 sub-zero fridge and your $1,500 dishwasher at the same time, you are doing math you won't like. It’s $5,000 per covered appliance per year in many versions of the contract, but always check your specific tier. For a standard household, $5,000 is a decent safety net. For a high-end smart home? It’s a drop in the bucket.

Why Florida is Different

In most states, surges are an occasional annoyance. In Florida, they are a statistical certainty. The soil in Florida is often sandy and porous, which actually makes for poor grounding. When lightning hits the ground or a pole, the energy looks for the path of least resistance. Often, that’s your copper wiring.

👉 See also: Why Use a Sentence with the Word Meager Instead of Just Saying Small

I’ve seen instances where a surge traveled through a cable line, hopped to the HDMI port, and fried the motherboard of a TV while leaving the power cord perfectly intact. The Florida Power and Light surge protection at the meter won't stop a surge coming through your Comcast or AT&T line. This is a massive blind spot most homeowners ignore. You need "point-of-use" protection for data lines too.

The Monthly Fee vs. Buying Your Own

SurgeShield costs about $10 or $11 a month. It just shows up on your FPL bill. It’s easy. You don't have to pay an electrician $300 to $500 to install a whole-home surge protector in your breaker panel.

But... do the math.

Over five years, you’ve paid over $600. You could have bought a high-end Siemens or Eaton whole-home surge protector for $150 and paid an electrician $200 to swap it in. You’d own the hardware.

So why do people go with FPL? It’s the warranty. When you buy your own device, getting the manufacturer to actually pay out a "connected equipment warranty" is like pulling teeth. They want you to mail in the fried device. They want proof of professional installation. They want the moon. With FPL’s program, the claims process is generally much smoother because they own the equipment at the meter. They can see the grid data from the time of the surge. It’s a convenience tax. You’re paying for the lack of a headache later.

Installation Realities

You don't even have to be home for the installation. Since the meter is outside, an FPL-contracted technician just pulls the meter, snaps the SurgeShield bypass in, and puts the meter back. It takes ten minutes. Your clocks will blink, and your oven will need a reset. That’s it.

Does it work on Solar?

This is a common question. If you have a solar array with a net-metering setup, you need to talk to the FPL Home reps specifically. Sometimes the physical configuration of the solar disconnects and the bidirectional meters makes the standard SurgeShield install tricky. Most of the time it’s fine, but don't assume.

Small Surges: The Silent Killer

Everyone worries about the big bolt of lightning. But the "transient surges" are what actually kill your stuff. Every time your AC compressor kicks on, it sends a tiny spike through your home’s internal grid. Over three years, those thousands of tiny spikes degrade the capacitors in your electronics.

📖 Related: Inaugural Balls 2025 Fashion: What Most People Get Wrong

A meter-based Florida Power and Light surge protection device doesn't stop these internal surges. It only looks outward. It’s a gatekeeper at the front door, but it doesn't care what’s happening inside the house. To truly protect your gear, you need a "tiered" approach:

- The Meter Protector (Stage 1): Catches the big stuff from the grid.

- The Breaker Panel Protector (Stage 2): Catches internal surges from your AC/Pool Pump.

- Point-of-Use Strips (Stage 3): High-quality (not cheap) strips for your sensitive tech.

Identifying a "Real" Surge Protector

Don't get fooled by "Power Strips." If it doesn't have a Joule rating, it’s just an extension cord with extra outlets. A real surge protector will have a UL 1449 rating. If you see that, it means it has been tested to actually divert a specific amount of energy.

When looking at the FPL program, look at the "Clamping Voltage." This is the temperature at which the device says "Enough!" and sends the power to the ground. Lower is better. If the clamping voltage is 400V, your electronics have to survive a 399V hit before the protector even wakes up. Most modern electronics hate anything over 150V.

The Claim Process Nightmare (And How to Avoid It)

If you get hit, you can't just call and say "My fridge died, give me money."

You usually need:

- A paid invoice from a licensed repair person stating the damage was "consistent with a power surge."

- The make, model, and serial number of the appliance.

- Proof that the device was actually plugged in and the SurgeShield was active.

Keep your receipts. If you have a repairman out, specifically ask them to write "power surge damage" on the work order. Without those three words, your claim will likely be denied. It sounds cynical, but it’s how the insurance side of these programs operates.

Is It Worth It?

If you are a renter? Probably not.

If you are a homeowner with an old electrical panel? Definitely.

If you have a brand-new home with a modern Square D surge-breaker already installed? You might be doubling up for no reason.

👉 See also: Vuori Black Friday Sale: What Most People Get Wrong About These Discounts

Honestly, for most Floridians, the $10 a month is peace of mind. It’s the cost of two coffees to know that if a transformer blows down the street, your $2,000 French-door fridge isn't going to become a very expensive paperweight.

Actionable Steps for Your Home

Stop relying on luck. Florida weather is too aggressive for "hope" to be a strategy.

First, walk around your house and count your major appliances. If you have more than $5,000 worth of "white goods," the FPL SurgeShield is a solid base layer. Call FPL Home or check your online portal to see if you're already enrolled—many people are and don't even know it.

Second, buy high-quality, UL-rated surge strips for your TVs and computers. Look for a Joule rating of at least 2,000 or higher. Anything less is basically useless for a Florida storm.

Third, check your "Grounding Rod." Go outside to your electrical meter. There should be a thick copper wire running into the dirt. If that wire is loose, corroded, or missing, no surge protector in the world will save you. The energy has nowhere to go. If it looks sketchy, call an electrician immediately. A surge protector without a good ground is like a car without brakes—it looks the part but won't stop the crash.

Verify your insurance policy as well. Some homeowners' insurance policies have a "Power Surge" rider that covers everything for a few extra dollars a year. Often, this is cheaper and more comprehensive than any utility program. Compare the two. If your deductible is $1,000, the FPL program is better because it often has a $0 deductible for repairs.

Decide today. Don't wait for the sky to turn that weird shade of Florida green. Once the thunder starts, it's already too late to plug things in.