Tax season is basically a national fever dream. You spend weeks gathering crumpled receipts and digital 1099s, all while wondering if that free income tax refund calculator you found online is actually telling the truth. Most people just want to know if they can afford that couch they’ve been eyeing or if they’re going to owe the IRS a small fortune.

It's a gamble.

Honestly, most online calculators are just math engines. They take what you give them, run it through the current tax brackets, and spit out a number. But the IRS tax code is over 6,000 pages long. A simple web tool can't always catch the nuance of your specific life. If you’ve got a side hustle, three kids, and a solar panel habit, your "estimated refund" might be a total fantasy.

The Math Behind the Free Income Tax Refund Calculator

How do these things even work? At the core, they’re looking at your Adjusted Gross Income (AGI). That’s the big number. It’s your total pay minus specific "above-the-line" deductions like student loan interest or IRA contributions.

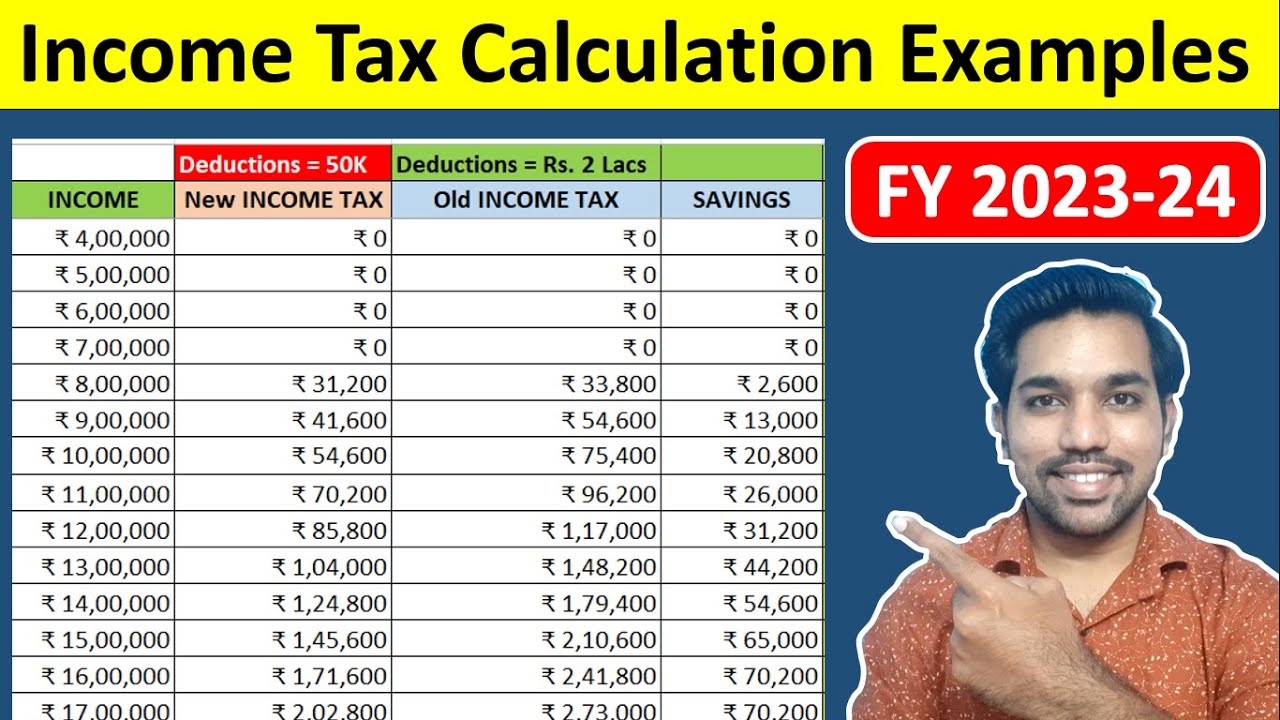

Then comes the Standard Deduction. For the 2025 tax year (filing in 2026), these numbers jumped again to keep up with inflation. If you’re single, it’s $15,000. Married filing jointly? You’re looking at $30,000. A good calculator automatically applies this. But here is where people trip up: they don't realize that the "refund" isn't free money from the government. It’s a return of your own overpayments. You gave the government an interest-free loan all year. Using a free income tax refund calculator is just checking to see how much of your own cash you’re finally getting back.

The algorithm usually follows a specific path:

💡 You might also like: Uang 40 Juta Hilang dan Skenario Nyata yang Sering Menimpa Nasabah

- Gross Income - Adjustments = AGI.

- AGI - Standard (or Itemized) Deduction = Taxable Income.

- Taxable Income applied to Brackets = Tax Liability.

- Tax Liability - Credits (like the Child Tax Credit) = Final Bill.

- Final Bill vs. Withholding = Refund or Amount Owed.

If you don't know your exact withholding from your W-2, the estimate is useless. Total guesswork.

Why Your Estimate Often Misses the Mark

The biggest culprit is the 1099-NEC. If you did any freelance work, you probably didn't pay taxes on that money yet. Most basic calculators forget to ask about Self-Employment Tax. That’s a 15.3% hit right off the top for Social Security and Medicare. It catches people off guard every single year. You think you’re getting $2,000 back because your day job withheld plenty, but then your $10,000 DoorDash side gig eats the entire refund.

Then there’s the "Clawback" effect.

Certain credits, like the Premium Tax Credit for health insurance, are based on your estimated income. If you made more money than you told the Marketplace, you might have to pay back some of those insurance subsidies. A standard free income tax refund calculator rarely accounts for Form 8962. It’s a nasty surprise that can turn a $3,000 refund into a $200 bill in seconds.

The Impact of State Taxes

People forget that federal and state are two different beasts. You might have a massive federal refund coming, but you owe your state hundreds. Some calculators bundle them; many don't. If you live in a high-tax state like California or New York, the interaction between federal deductions and state taxes is incredibly complex. Since the SALT (State and Local Tax) deduction limit is still a factor, your "itemized" dreams might be crushed by that $10,000 cap.

Credits vs. Deductions: The Secret Sauce

A lot of users get these confused. A deduction lowers the income you’re taxed on. A credit lowers your tax bill dollar-for-dollar.

If you’re using a free income tax refund calculator, look for one that asks deep questions about:

- The Child Tax Credit (CTC): Is it fully refundable this year? The rules shift constantly depending on what Congress decided at the 11th hour.

- Earned Income Tax Credit (EITC): This is one of the most powerful tools for low-to-moderate earners, but the math is notoriously difficult.

- Education Credits: If you’re paying tuition, the American Opportunity Tax Credit (AOTC) can put up to $2,500 back in your pocket.

If the tool doesn't ask about your kids' ages or your tuition payments, it’s not an expert tool. It’s a toy.

Trusting the Tech

Is it safe to put your data into these things? Generally, yes, if you stick to the big names like Intuit (TurboTax), H&R Block, or FreeTaxUSA. They use the same encryption as banks. But be wary of "no-name" calculators on random blogs. They might just be lead-generation tools designed to sell your email to debt relief companies.

Also, watch out for "phantom" refunds. Some shady sites will show you a massive number just to get you to click through to their paid filing service. Once you actually start the return, that "refund" evaporates as the real math kicks in.

✨ Don't miss: 801 South Figueroa Street: Why This Tower Is Still the Anchor of Downtown LA

How to Get the Most Accurate Result

Don't guess.

If you want a free income tax refund calculator to actually work, you need your last pay stub of the year. Look for the "Year to Date" (YTD) Federal Tax Withheld. That is the most important number. Without it, the calculator is just throwing darts in the dark.

You also need to account for interest from your savings account. With rates being higher lately, that 1099-INT from your bank might actually show a few hundred dollars in taxable income you forgot about. It adds up.

Steps to Take Right Now

Stop staring at the "estimated" number and start organizing.

First, grab your W-2s and any 1099s. If they haven't arrived yet, use your final 2025 pay stubs. Second, check your filing status. If you're "Head of Household" instead of "Single," your standard deduction jumps significantly. That alone can swing your refund by thousands. Third, look at your retirement contributions. If you haven't maxed out your traditional IRA, you often have until April 15th to contribute and lower last year's taxable income.

👉 See also: Why 4 Columbus Circle NYC Is Still the Most Interesting Corner of Midtown

Finally, don't wait until April. If the free income tax refund calculator shows you owe money, you want to know that in January so you have three months to save up. If you're getting a refund, file early. The IRS usually starts processing in late January, and the sooner you're in the queue, the sooner that money hits your account.

Verify your withholding for next year while you're at it. If your refund is massive (over $5,000), you're essentially letting the government hold your money for free. Adjust your W-4 at work to bring home more in your paycheck every month instead. It's your money. You should probably be the one earning interest on it.