You’ve probably heard your parents or that one financially sorted uncle rave about the PPF. It’s been the darling of Indian middle-class savings for decades. Honestly, it’s easy to see why. But here’s the thing: most people just throw money into it blindly at the end of March. They don't actually see the math. Using a public provident fund india calculator isn't just about playing with sliders on a screen; it’s about realizing how much wealth you’re leaving on the table by being even a few days late with your deposit.

The Public Provident Fund (PPF) is a long-term investment scheme backed by the Government of India. It offers safety, decent returns, and massive tax benefits. But the magic—and the frustration—is in the compounding.

Why the Math Behind a Public Provident Fund India Calculator Is Weird

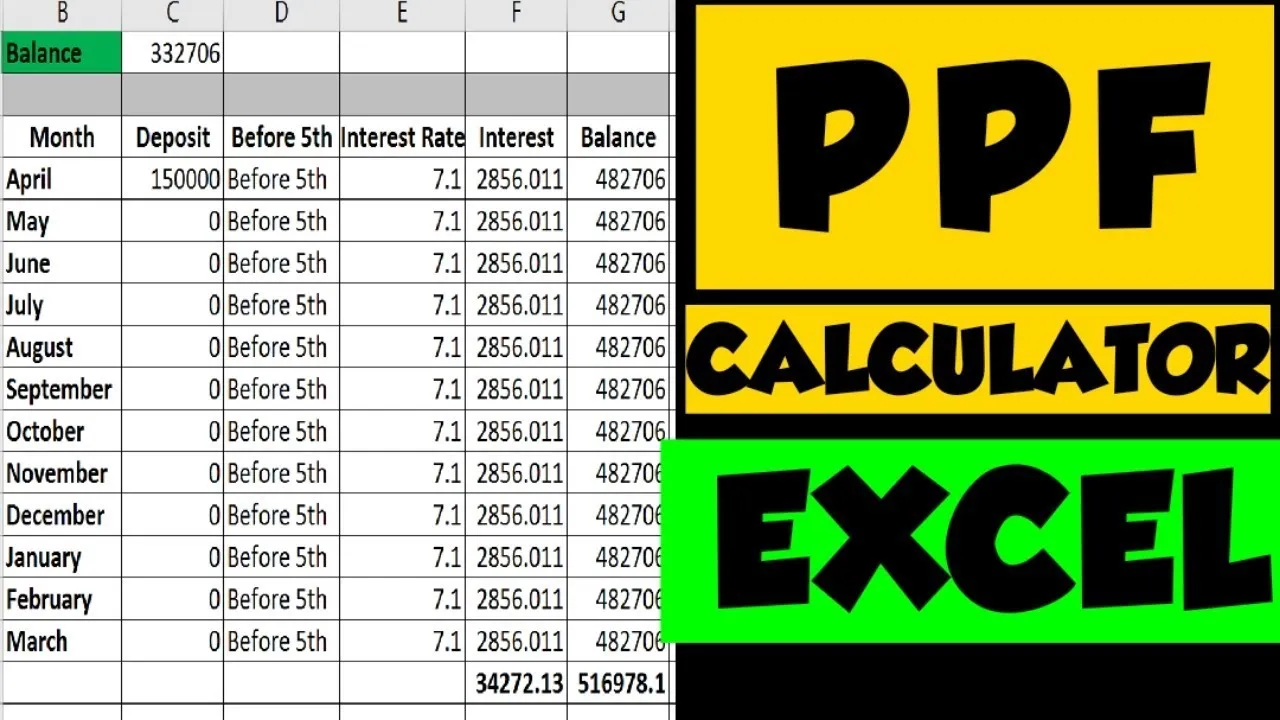

PPF interest isn't calculated like a standard bank savings account. If you don't know the "5th of the month" rule, you’re basically giving the government free money. The interest is calculated on the lowest balance in your account between the close of the 5th day and the end of the month.

🔗 Read more: 3rd quarter estimated tax due date 2024: Why the September Deadline Caught So Many People Off Guard

Let's say you deposit ₹1.5 lakh on April 6th. You just lost an entire month of interest on that huge sum. If you’d done it on April 4th, you’d be earning interest for the full month of April. Over a 15-year period, that one-day difference in dozens of deposits adds up to thousands of rupees. This is exactly why people get obsessed with a public provident fund india calculator. It visualizes the "what-ifs."

The 15-Year Lock-in Myth

Everyone says PPF is a 15-year commitment. That’s technically true, but the way the "years" are counted is kinda confusing. The 15-year tenure starts from the end of the financial year in which you opened the account. If you opened it in January 2024, the clock doesn't start until March 31, 2024. Your account actually matures on April 1, 2039. So, it's more like 16 years.

Cracking the Interest Rate Code

The Ministry of Finance reviews the interest rate every quarter. For a long time, it sat comfortably at 8% or higher. Lately, it’s been hovering around 7.1%. While that might sound low compared to the Nifty 50 or some aggressive mid-cap mutual fund, you have to look at the "Tax-Free" nature of it.

In India, PPF falls under the EEE category.

- Exempt on the investment (under Section 80C).

- Exempt on the interest earned.

- Exempt on the maturity amount.

If you are in the 30% tax bracket, a 7.1% tax-free return is equivalent to earning over 10% in a taxable Fixed Deposit. Most people forget that. When you plug numbers into a public provident fund india calculator, the final figure you see is exactly what hits your bank account. No TDS. No capital gains tax. Nothing.

The Power of the Extension Rule

Most people think the game ends at 15 years. It doesn't. You can extend your PPF account in blocks of 5 years, indefinitely.

There are two ways to do this:

- Extension with contribution: You keep putting money in and keep earning interest.

- Extension without contribution: You stop putting money in, but the existing corpus continues to earn interest.

If you started a PPF at age 25 and maxed it out at ₹1.5 lakh every year, by the time you're 40, you have a massive nest egg. If you extend it twice—taking you to age 50—the compounding goes nuclear. We’re talking about a corpus that can easily cross ₹1 crore depending on the prevailing interest rates over those decades.

Can You Withdraw Early?

Yes, but it's restrictive. You can’t touch the money for the first five years. From the seventh year onwards, you can take partial withdrawals. But there's a limit: you can only take 50% of the balance that was in the account at the end of the fourth year preceding the year of withdrawal, or the end of the preceding year, whichever is lower. It's a mouthful. Basically, the government wants you to keep the money in there. It’s a "forced" savings habit that actually works for people who lack financial discipline.

Common Mistakes That Ruin Your Returns

I see people making the same three mistakes constantly. First, they deposit money in small chunks throughout the year. If you have the cash, lump-summing it in the first week of April is the "pro move." It ensures you get interest on the full amount for all 12 months of the financial year.

🔗 Read more: The List of Dow Jones Companies Is Kinda Weird if You Think About It

Second, people forget the ₹1.5 lakh limit applies to you as an individual. If you open an account for your minor child, the combined investment in your account and the child’s account cannot exceed ₹1.5 lakh for tax deduction purposes. If you put in more, the excess amount won't earn any interest. It just sits there, bored.

Third, they ignore the nomination facility. If something happens to you, a PPF account without a nominee becomes a legal nightmare for your family. They’d have to produce succession certificates or letters of administration for a measly few lakhs. Just fill out the form. It takes two minutes.

Comparing PPF to the Alternatives

Is PPF better than the Voluntary Provident Fund (VPF) or the National Pension System (NPS)?

VPF often offers a slightly higher interest rate (usually around 8.15% to 8.25%), but it’s only available to salaried employees. NPS has the potential for much higher returns because it invests in equities, but it locks your money up until age 60 and forces you to buy an annuity with 40% of the corpus.

PPF is the middle ground. It’s flexible, available to everyone (including freelancers and the self-employed), and gives you the full amount in cash at maturity.

Actionable Steps for Your PPF Strategy

Don't just read about it. Do these three things today to maximize your account:

1. Check Your Last Deposit Date

Look at your passbook. If you’ve been depositing after the 5th of the month, change your automated standing instructions right now. Set it for the 1st or 2nd.

👉 See also: Why 1701 JFK Blvd Philadelphia PA 19103 is More Than Just a Commuter Landmark

2. Use a Calculator for "Scenario Stress Testing"

Open a public provident fund india calculator and run two scenarios. Scenario A: You invest ₹5,000 a month. Scenario B: You invest ₹1.5 lakh every April 1st. Look at the difference in the final maturity amount after 15 years. That gap is the "procrastination tax" you're paying.

3. Evaluate the 5-Year Extension

If your account is nearing its 15th year, don't just close it. If you don't need the money for a house downpayment or a wedding, file Form H to extend it with contributions. This keeps the EEE benefit alive. Once you close it and take the cash, putting that much money back into a tax-free instrument is nearly impossible.

4. Link Your Bank Account

Most banks like SBI, HDFC, or ICICI allow you to transfer funds to your PPF online. If you're still carrying a physical cheque to a post office, you're living in 1995. Digital transfers ensure your money starts earning interest the moment it leaves your savings account.

PPF isn't about getting rich overnight. It's about that slow, boring, unstoppable growth that makes you look like a genius twenty years from now.