You open your banking app on Friday morning. There it is. The direct deposit hit, but the number looks... small. It’s always smaller than you expect, isn't it? You know your salary. You know the hourly rate you agreed to when you signed that offer letter in the HR manager's office. Yet, the gap between that "sticker price" and the cash in your pocket feels like a magic trick where you're the one losing the rabbit.

Understanding how do you calculate your net pay isn't just about being good at math. Honestly, it’s about defensive financial driving. If you don't know where the money is going, you can't catch the errors that—believe it or not—happen more often than payroll companies like to admit.

The Brutal Reality of Gross vs. Net

Gross pay is the dream. Net pay is the reality.

Gross pay is that big, beautiful number before the government, your health insurance provider, and your future self (via the 401k) take their cut. To get to the net, you have to peel back layers of deductions like an onion that makes you cry.

Most people think it’s just taxes. It’s not. It’s a combination of statutory withholdings—things the law says must come out—and voluntary deductions that you chose during open enrollment. If you're wondering how do you calculate your net pay accurately, you have to start with the Gross and then subtract three specific "buckets" of money.

Bucket One: The Taxman's Cut

Federal income tax is the big one. This is dictated by the W-4 form you filled out when you started. If you haven't looked at that form since 2020, it’s probably wrong. The IRS redesigned the W-4 a few years back to remove "allowances," and if you're still cruising on an old version, your withholding might be way off.

Then there’s FICA. This stands for the Federal Insurance Contributions Act. It’s a flat-ish rate. You’re paying $6.2%$ for Social Security and $1.45%$ for Medicare. Your employer matches this, by the way. If you’re self-employed? You’re paying both halves. That’s the "self-employment tax" that catches freelancers off guard every April.

Don't forget state and local taxes. Some of you live in Florida or Texas and pay zero state income tax. Lucky you. If you’re in California or New York, that’s another massive chunk gone before you even see a dime.

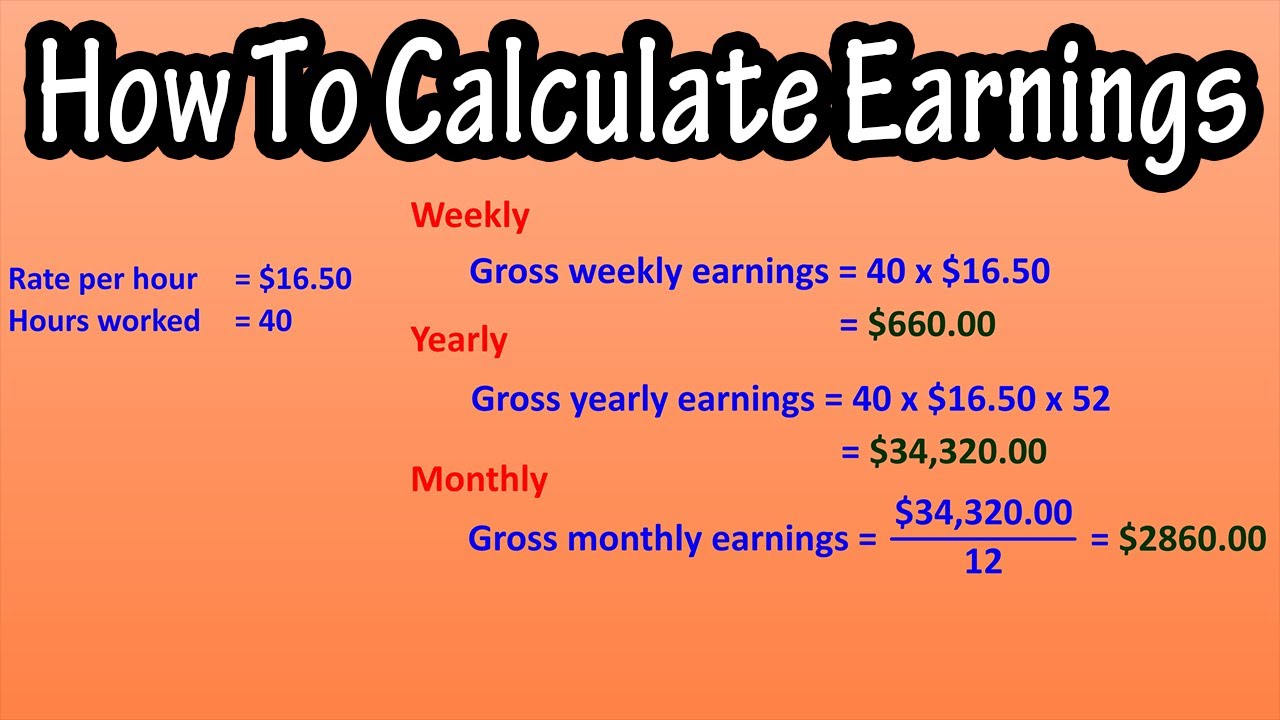

The Math Behind the Madness

Let's look at an illustrative example. Say you earn $5,000$ a month gross.

First, you subtract your pre-tax deductions. These are your best friends because they lower your taxable income. If you put $500$ into a traditional 401k and pay $200$ for health insurance, the government only taxes you as if you made $4,300$.

How do you calculate your net pay from here? You take that $4,300$ and apply your tax bracket rates.

After federal, state, and FICA taxes are gone, you might be left with $3,400$. But wait. Did you sign up for a Life Insurance policy through work? Is there a $20$ fee for the company gym? These are post-tax deductions. They come out after the tax has been calculated.

📖 Related: Women in Leadership Statistics: What the Data Actually Says About the Glass Ceiling in 2026

Finally, you reach the "Take-Home Pay."

Why Your W-4 Is Probably Messing Everything Up

Many people treat their tax refund like a "savings account" from the government. That’s a mistake. A huge refund means you gave the government an interest-free loan all year. If you want more net pay now, you need to adjust your W-4.

The Tax Foundation notes that most Americans over-withhold. If you have kids (Child Tax Credit) or you’re Head of Household, but your payroll department thinks you’re "Single/Standard Deduction," your net pay will be significantly lower than it should be.

The "Hidden" Deductions You Forgot About

It’s not just the big stuff.

- Garnishments: If you owe child support or student loans in default, the court can take money directly.

- FSA/HSA: These are pre-tax powerhouses. If you aren't using them, you're essentially paying more in taxes than necessary.

- Union Dues: If you're in a trade or certain public sectors, these are often non-negotiable.

Real World Nuance: The Pay Period Factor

The "how" changes based on frequency.

If you're paid bi-weekly (26 times a year), two months out of the year you get a "magic" third paycheck. On those months, your net pay feels huge because many of your fixed deductions (like health insurance) might have already been covered by the first two checks.

Monthly pay is different. It’s a slog. You have to budget that one lump sum for 30 or 31 days.

👉 See also: Sam Walton: Made in America and Why the Legend Still Matters

Steps to Take Right Now

Stop guessing.

First, get your last three pay stubs. Look at the "Year to Date" (YTD) column. Is the federal tax withholding at least $10%$ to $15%$ of your gross? If it’s lower and you aren't in a low-income bracket, you might owe money at the end of the year.

Second, use the IRS Tax Withholding Estimator. It is the only "official" way to ensure your net pay is optimized.

Third, check your "voluntary" deductions. Are you still paying for that "Accidental Death and Dismemberment" policy you signed up for during orientation five years ago? If you don't need it, cancel it. That’s instant net pay growth.

Finally, verify your state's specific rules. Some states have "SUI/SDI" (State Unemployment Insurance or State Disability Insurance) that takes a tiny sliver—usually less than $1%$—but it adds up over a year.

Calculating your net pay is ultimately about control. You work hard for the gross; you should at least know where the "missing" pieces are landing. Check your stub this week. Not just the bottom line, but every single line item above it. You might be surprised by what you find.