You're sitting at your kitchen table, staring at a bill that looks like it belongs to a small corporation rather than a three-bedroom house in Westchester or a condo in Brooklyn. It’s a classic New York moment. Whether you’re a first-time buyer or a long-time resident, the math behind how much is the property tax in New York often feels like a riddle wrapped in an enigma, then buried under a mountain of local ordinances.

Honestly, there is no single "New York rate." If you move ten miles in any direction, your bill might double or drop by half. The system is famously fragmented. You've got different rules for New York City than for the rest of the state, and then you've got a patchwork of school districts, counties, and "special districts" (for things like libraries or even fire hydrants) that all want a piece of your equity.

Why Your Neighbor Pays Less Than You

It feels personal, but it’s usually just the "class" system. In New York City, properties are split into four distinct classes. If you own a one-to-three-family home, you're in Class 1. For the 2025-2026 fiscal year, the provisional tax rate for Class 1 is roughly 20.630%.

Wait. Don't panic.

📖 Related: How Do I Make a Peach Pie That Actually Holds Together?

That 20% isn't applied to what you could sell your house for today. It’s applied to the "assessed value," which in NYC is only 6% of the market value. So, if the city thinks your house is worth $600,000, they assess it at $36,000. Then they hit that $36,000 with the 20.630% rate.

But here’s where it gets kinda weird. NYC has "assessment caps." By law, the assessed value of a Class 1 home can't go up more than 6% in one year or 20% over five years. If the market in your neighborhood explodes and your home value doubles, your tax bill won't follow—at least not right away. This is why a person who bought their house in the 90s might be paying $3,000 a year, while the person who just bought the identical house next door is paying $8,000. It’s a "welcome to the neighborhood" tax, basically.

The Upstate and Suburb Reality Check

Outside the five boroughs, the "6% assessment" rule goes out the window. Most of New York State uses a "Uniform Percentage of Value." This means the town decides to assess everyone at, say, 50% or 100% of market value.

If you live in places like Rochester, Buffalo, or parts of Westchester, your effective tax rate—the actual percentage of your home's value you pay every year—is much higher than in NYC. While a Manhattanite might pay an effective rate of about 0.9%, someone in Monroe County might be looking at 3% or higher.

Actually, New York State often ranks in the top five nationally for property tax burden, but that's largely driven by Upstate and the suburbs. School taxes are the real killer. In many New York towns, school taxes account for about 60% to 70% of the total bill. You aren't just paying for the roads; you're funding the local high school’s new turf field.

Breaking Down the 2026 Numbers

As of January 2026, the New York City Department of Finance has been tracking a steady climb in market values, particularly in Brooklyn and Queens. If you’re looking for a ballpark of how much is the property tax in New York right now, here’s the rough breakdown of the latest provisional rates for the 2025-2026 tax year:

- Class 1 (Small Homes): 20.630%

- Class 2 (Condos/Co-ops/Rentals): 12.340%

- Class 4 (Commercial): 10.774%

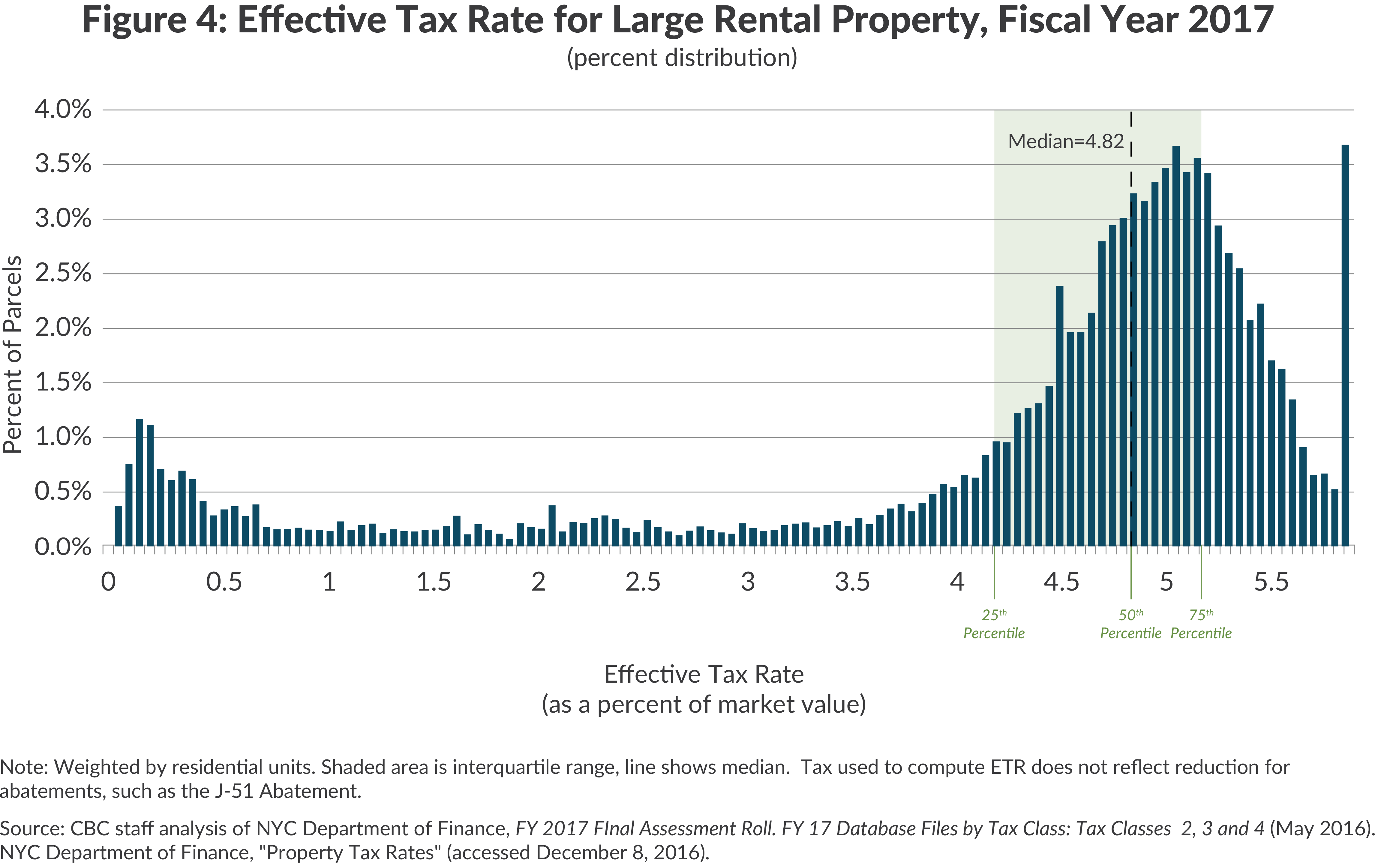

Keep in mind that for Class 2 properties (those big apartment buildings), the assessment isn't 6%—it's 45%. However, the city uses a complicated "rental income" model to value condos and co-ops, which often results in them being undervalued compared to what they actually sell for. It's a mess. Even the experts at the Tax Foundation or the Empire Center for Public Policy regularly point out that the system is arguably "broken" because it treats similar properties so differently.

STAR: Your Only Real Shield

If you live in your home (it’s your primary residence), you need to know about STAR (School Tax Relief). It’s the most common way to shave a few hundred—or a few thousand—dollars off that bill.

There are two versions. Basic STAR is for pretty much everyone whose income is under $500,000 (for the credit) or $250,000 (for the exemption). Then there’s Enhanced STAR for seniors (65+) with lower incomes.

For the 2026-2027 school year, the income limit for Enhanced STAR has bumped up to $110,750. If you qualify, the state basically ignores a huge chunk of your home’s value—around $88,500 of it—when calculating school taxes.

And a quick tip: if you're a new homeowner, you don't get the "exemption" (a discount on the bill) anymore. You get the "credit," which is a check or direct deposit sent to you by the state. It's the same amount of money, just a different way of getting it. Sorta like a tax-season surprise.

💡 You might also like: Why Before After Chemical Peel Pictures Don't Always Tell the Whole Story

The Hidden Factors: Abatements and Exemptions

Beyond STAR, there are "abatements." These are different from exemptions. An exemption lowers your assessed value. An abatement is a direct discount on the tax dollar amount.

Common ones include:

- Senior Citizen Homeowners’ Exemption (SCHE): For those 65+ with limited income.

- Veterans Exemption: If you served, especially in a combat zone, you can get a serious haircut on your bill.

- Good Samaritan/First Responder: Some local jurisdictions offer small breaks for volunteer firefighters or ambulance workers.

What Most People Get Wrong

People often think that if the city raises their "Market Value" on the notice of assessment, their taxes will automatically jump by the same percentage. That’s not how it works.

The city or town first decides how much money it needs to run (the tax levy). Then they look at the total value of all the property in the area. Your tax rate is just the math required to bridge that gap. If everyone’s property value goes up by 10%, but the city’s budget only goes up by 2%, your tax rate might actually go down.

Also, if you're in NYC, don't forget the 2.5% constitutional tax cap. The city is limited in how much it can collect relative to the total value of all the property in the five boroughs.

Actionable Steps for the Tax-Weary

Stop just paying the bill and hoping for the best. You have tools.

👉 See also: Air Force One Black: What Most People Get Wrong

First, check your "Notice of Property Value." In NYC, these come out in January. Look at the "Market Value" they’ve assigned you. If they think your house is worth $900,000 and you know for a fact you couldn't sell it for $750,000, you need to challenge it. The deadline to file an appeal with the NYC Tax Commission is usually March 15th for Class 1 properties.

Second, verify your exemptions. Go to the NY State Department of Taxation and Finance website or the NYC Department of Finance portal. Search your address. If it doesn't say "STAR" or "Veteran" and you qualify, you're literally leaving money on the table.

Third, watch the school board meetings. Since school taxes are the biggest chunk of the pie for those outside the city, the budget votes in May are your only real chance to influence the "how much" of your property tax.

Property taxes in New York are a beast, but they aren't totally untamable. You just have to know which "class" you're in and make sure you're getting every discount the law allows.

Verify your current property record on the NYC Department of Finance website (or your local county assessor's portal) to ensure your "Taxable Value" reflects any exemptions you are legally entitled to for the upcoming 2026 cycle.