You're staring at a screen. The price for that flight to Tokyo or Rome just jumped $200 while you were waiting for your paycheck to hit. It's frustrating. Honestly, it’s enough to make you want to close the laptop and give up on the trip entirely. But then you see that little button at checkout: book flight ticket now and pay later. It looks like a lifesaver, right? Maybe. It depends on whether you know how the math actually works behind the scenes.

Travel is expensive. We all know it.

Back in the day, you either had the cash or you put it on a high-interest credit card and prayed you could pay it off before the 24.99% APR ate your soul. Things have changed. Now, we have "Fly Now, Pay Later" (FNPL) providers like Affirm, Klarna, and Uplift. They’ve basically integrated themselves into the checkout flow of almost every major airline, from United to Lufthansa.

But here’s the thing: these services aren't all created equal. Some are basically interest-free short-term loans. Others are debt traps disguised as "convenience." If you’re going to use them, you’ve got to be smart.

The Reality of Point-of-Sale Loans in Travel

When you decide to book flight ticket now and pay later, you aren't actually paying the airline in installments. You’re taking out a loan. A third-party company pays the airline the full amount immediately, and you owe that third party the money back over three, six, or twelve months.

It’s a simple concept.

Most people think these are always interest-free because of how they’re marketed. That's a mistake. While some "Pay in 4" models (four payments over six weeks) often have 0% interest, longer-term loans for expensive international flights can carry APRs as high as 30%. That can sometimes be more expensive than a standard credit card.

Why the "Pay in 4" Model is the Sweet Spot

If you’re looking for the best deal, the "Pay in 4" structure is usually the winner. You put down 25% today. Then, you pay the rest every two weeks. Since most people get paid bi-weekly, it aligns perfectly with a budget.

There's usually no hard credit pull for these. Your credit score stays safe. It’s basically a handshake agreement backed by your debit card. However, if you miss a payment, the late fees can be brutal. And if you’re booking a $2,000 flight to Sydney, a "Pay in 4" might still mean $500 every two weeks. That's a heavy lift for a lot of people.

Long-term Financing: The 12-Month Trap

Then there are the longer loans. These are the ones offered by companies like Uplift (which was acquired by Upgrade) or Affirm. They specialize in the travel industry. You’ll see them right there on the payment page for American Airlines or Southwest.

✨ Don't miss: Why 234 W 42nd St New York NY 10036 is Still the Heart of Times Square

They offer you "low monthly payments."

It sounds great. "Only $80 a month for your vacation!" But read the fine print. If that $80 a month goes on for 18 months at 15% interest, you're paying significantly more for that seat than the person sitting next to you. You’re essentially paying for the flight long after the tan has faded and the memories are blurry.

Major Airlines and Their Partners

Not every airline uses the same provider. If you have a preference for one service—say, you already use Klarna for clothes—you might want to know which airline plays nice with them.

Delta Air Lines has a long-standing relationship with American Express. While they offer "Plan It" features for Amex cardholders, they’ve also integrated with other providers. United Airlines leans heavily on Uplift. If you book through United, you’ll see the Uplift option right next to the credit card field. Southwest Airlines also uses Uplift, making those domestic hops even easier to finance.

Alaska Airlines and JetBlue have similar setups. It’s become an industry standard.

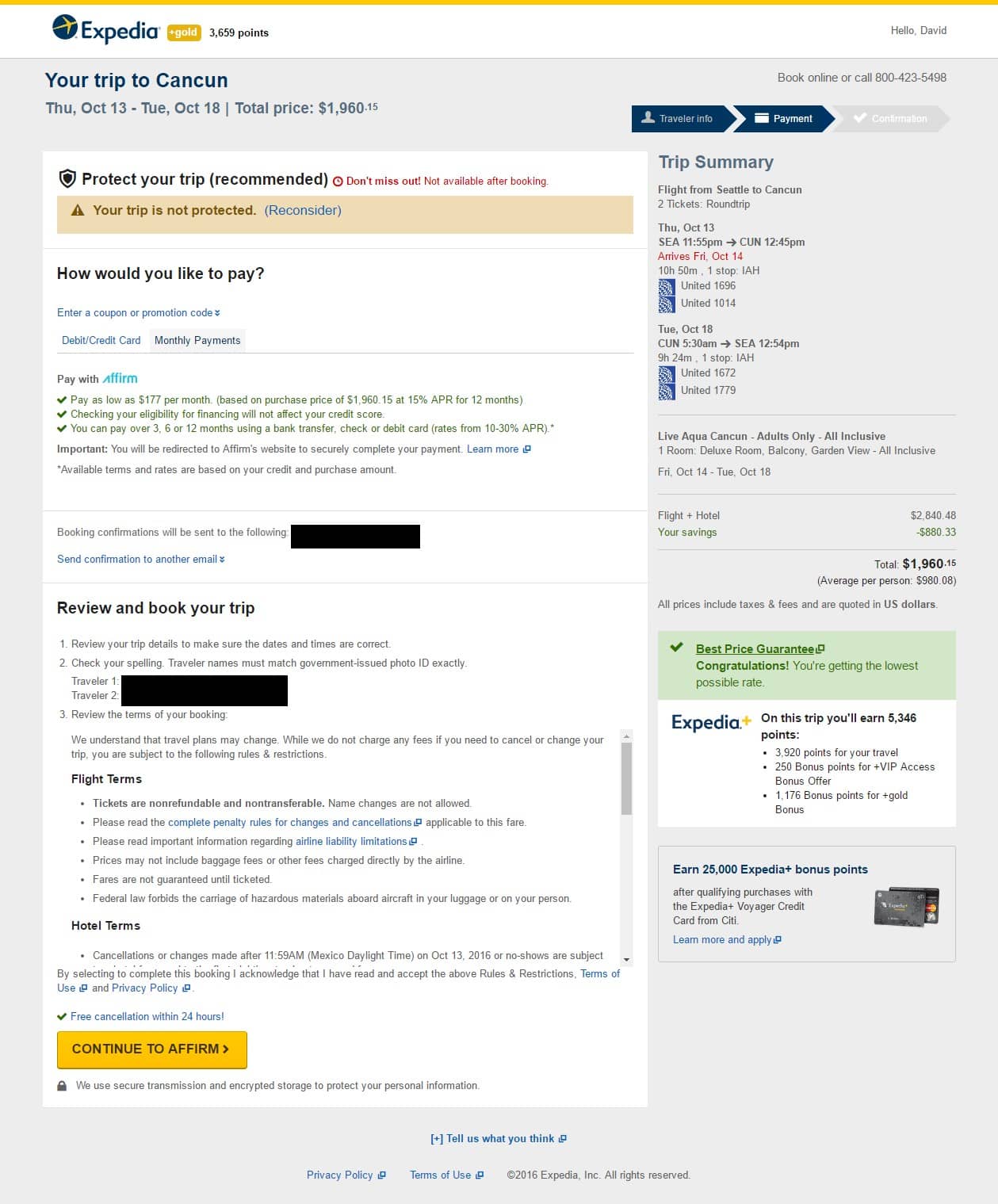

Expedia and Third-Party Sites

Sometimes it’s easier to go through an OTA (Online Travel Agency). Expedia and Priceline are massive fans of the "pay later" model. Expedia uses Affirm. The benefit here is that you can often bundle your hotel and car rental into one single "pay later" loan.

One bill. One APR. One headache.

But be careful. When you book through a third party, changing your flight becomes a nightmare. If the airline cancels the flight, getting your money back to the loan provider is a bureaucratic slog that involves three different customer service departments. It’s often better to book directly with the airline if you can.

The Credit Score Impact Nobody Mentions

"Will this hurt my credit?"

🔗 Read more: Nassau Bahamas on Map: What Most People Get Wrong

That’s the number one question. Most FNPL providers do a "soft" credit check. This doesn't affect your score. It’s just a quick peek to see if you’re a total risk.

However, some of the longer-term loans (those 6-12 month ones) might report to credit bureaus. If you pay on time, it can actually help your score by building a history of on-time payments. But if you're already struggling with debt, adding another installment loan can skew your debt-to-income ratio.

Lenders see that.

If you're planning on buying a house or a car in the next year, maybe don't stack up three different "pay later" flight loans. It looks messy on a credit report.

When Does it Actually Make Sense?

I’m not saying you should never book flight ticket now and pay later. There are times when it is genuinely the smartest move you can make.

- Emergency Travel: If a family member is sick or there’s a sudden crisis, you can’t wait for a paycheck. FNPL is a godsend here.

- The "Last Seat" Scenario: If you see a fare error or a massive sale that you know will be gone in three hours, locking it in now and paying it off over six weeks is a valid strategy.

- 0% Offers: If you qualify for a 0% APR promotion, it’s literally free money. Why pay $1,000 upfront when you can keep that cash in a high-yield savings account and pay the loan off gradually?

Misconceptions and Red Flags

A lot of people think that if they use a pay-later service, they get extra protection if the airline goes bust.

False.

In fact, you might have fewer protections. Credit cards have robust "chargeback" rights under federal law (like the Fair Credit Billing Act). If an airline refuses to refund a cancelled flight, your credit card company can claw that money back.

With a "pay later" loan, you're in a gray area. You still owe the loan provider the money even if the airline is jerking you around. You have to keep making payments while you fight the airline for a refund. It’s a mess.

Look Out for Compound Interest

Some "travel loans" don't use simple interest. They use compound interest. This means you’re paying interest on the interest. Most reputable providers like Affirm use simple interest, which is much more transparent. Always check the "Truth in Lending" disclosure before you click "confirm."

🔗 Read more: Exactly how far from Savannah to Charleston is the drive?

If they don't show you the total cost of the loan in dollars—not just the monthly payment—run away.

Alternatives That Might Be Better

Before you jump into a loan, consider a few other paths.

PayPal Pay in 4 is available on many travel sites and is generally very reliable. If you already have a PayPal account, it’s a one-click process.

Credit Card "Plan" Features: Chase has "My Chase Plan" and Amex has "Plan It." These allow you to take a large purchase (like a flight) and break it into monthly payments for a fixed fee instead of interest. Often, the fee is lower than the APR you’d get from a random finance company. Plus, you still earn your travel points.

The "Old School" Way: If the flight is six months away, just put that "monthly payment" into a separate savings account yourself. If you can't trust yourself to save it, then okay, maybe the loan is the discipline you need. But you're paying for that lack of discipline.

How to Do It Right: A Step-by-Step Approach

If you've weighed the risks and you're ready to book flight ticket now and pay later, follow these steps to ensure you don't get burned.

First, compare the total cost. Look at the flight price on the airline’s site. Then, go all the way to the payment screen and select the pay-later option. Look at the "Total of Payments" number. If the flight is $500 and the total of payments is $580, ask yourself if that flight is really worth $580.

Second, check your existing credit card. See if you have a 0% intro APR offer or a "split pay" feature. This is almost always better because you get the points and the purchase protection.

Third, set up autopay. Most of these services require it anyway, but make sure the money is actually in your bank account on the due date. Bounced payment fees can wipe out any savings you got from a cheap flight.

Finally, read the refund policy. This is the big one. Know exactly what happens if you have to cancel. Does the refund go to you or the lender? Usually, it goes to the lender to pay off the balance, but it can take weeks to process.

Actionable Insights for the Savvy Traveler

- Prioritize 0% APR: Only use FNPL for luxury travel if you get a 0% interest rate. If you're paying 20% interest to go to Vegas, you're losing the game.

- Use Debit for the Down Payment: Most services won't let you use a credit card to pay off your "pay later" loan (no double-dipping on debt). Have the cash ready for the first installment.

- Watch the "Hard Pull": If a provider asks for your Social Security number, there's a higher chance of a hard credit inquiry. Most "Pay in 4" services only need your name, address, and DOB.

- Direct is Best: Try to use the airline's official partner (like United/Uplift) rather than a third-party travel site's partner. It makes the customer service trail much shorter.

- Keep Your Receipts: Save every email. If there’s a dispute, you’ll need the loan agreement and the airline’s booking confirmation to prove what you’re owed.

Booking a flight should be exciting, not a source of financial dread. These "pay later" tools are just that—tools. In the hands of a careful traveler, they help manage cash flow and catch great deals. In the hands of an impulsive spender, they’re a recipe for a "debt hangover" that lasts long after you've unpacked your suitcase.

Be the careful traveler. Check the APR, understand the refund policy, and only commit to payments you know you can hit without sweating. That’s how you actually enjoy the trip.