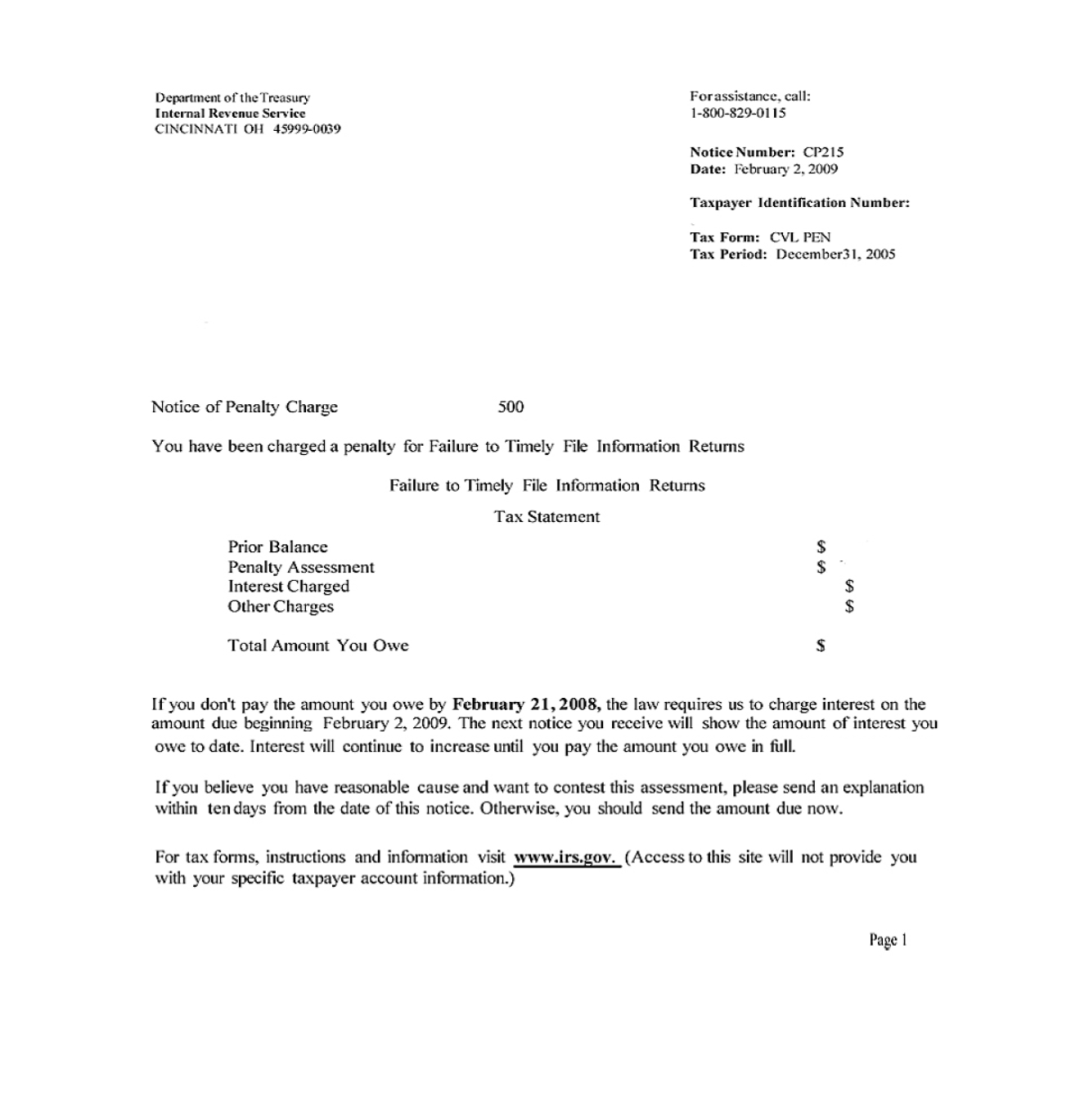

Getting a notice from the IRS is enough to make anyone's stomach drop. You open the envelope, see a mountain of interest and penalties, and suddenly that tax bill is 25% higher than you expected. It's frustrating. But here is the thing: the IRS actually has a "get out of jail free" card that they don't exactly advertise on billboards. It is called IRS first time penalty abatement.

Most people think the IRS is a cold, unfeeling machine. Honestly? Sometimes it is. But the First-Time Abate (FTA) policy is an administrative waiver designed specifically for people who are usually "good" taxpayers but had a bad year. If you have a clean track record, the IRS will often wipe the slate clean for one year—no excuses required.

Starting in 2026, things are changing. The IRS is moving toward automatic penalty abatement for those who qualify, but you shouldn't just sit around and wait for it. If you have a penalty hanging over your head right now, you need to know how the system works before you pay a dime you don't actually owe.

The Secret Handshake of Tax Relief

Basically, the FTA is a "clean compliance" reward. The IRS isn't looking for a sob story here. They don't care if your dog ate your W-2 or if you were feeling "stressed." That stuff falls under Reasonable Cause, which is a whole different (and much harder) battle. For an IRS first time penalty abatement, the criteria are surprisingly black and white.

📖 Related: Why Converting 200 UK Pounds to US Dollars Is More Complicated Than You Think

You've got to hit three specific marks. First, you must have a clean three-year history. This means for the three years leading up to your "problem" year, you didn't have any significant penalties on the same type of tax return. If you're looking for relief on your 2024 taxes, the IRS will peek at 2021, 2022, and 2023. If those look good, you’re halfway there.

Second, you have to be current on your filings. You can't ask for a favor while you still have unfiled returns sitting on your desk. The IRS expects you to be "compliant," which means every required return must be in their system.

Third, you have to have paid or arranged to pay the underlying tax. You don't necessarily have to be debt-free. If you are on an installment agreement and you’re making your payments on time, you still qualify. The IRS just wants to see that you aren't ignoring the debt entirely.

Which Penalties Actually Disappear?

Not every fine is eligible. The IRS is picky. The FTA waiver only applies to three specific types of "standard" penalties:

- Failure to File: That nasty 5% per month charge for being late with the paperwork.

- Failure to Pay: The 0.5% monthly fee for not sending the cash.

- Failure to Deposit: This one is for business owners who messed up their payroll tax deposits.

If you’re looking at an accuracy-related penalty (because you "accidentally" claimed your cat as a dependent) or an estimated tax penalty, the FTA won't help you. Those require different strategies.

The 2026 Automatic Shift: A Double-Edged Sword

For years, the National Taxpayer Advocate—shoutout to Erin Collins—has been screaming into the void that the IRS should just apply these waivers automatically. Why make people beg for something they already qualify for? In late 2025, the IRS finally confirmed that in 2026, they are rolling out a system to trigger these abatements without you having to pick up the phone.

Sounds great, right?

👉 See also: OTR Off The Flame: What the Tire Industry Isn't Telling You About Heat

Well, sort of. The "catch" is that the FTA is a one-time deal. Once you use it, you can't use it again for another three years of clean history. If the IRS automatically applies it to a tiny $150 penalty this year, and next year you hit a snag that results in a $5,000 penalty, you’ve wasted your "mulligan."

You have to be strategic. Sometimes it is better to pay a small penalty and save your FTA for a bigger disaster down the road.

How to Actually Get the Money Back

If the IRS hasn't automatically fixed your account, you have to take the wheel. You can call them. Honestly, for individuals, a phone call to the number on your notice is often the fastest way. Tell the agent: "I’d like to request First Time Abatement for the failure to file/pay penalty based on my clean compliance history." If the person on the other end sounds confused, ask them to check the Reasonable Cause Assistant (RCA). That’s the software the IRS uses to see if you qualify.

For businesses or larger amounts, go with Form 843, Claim for Refund and Request for Abatement.

🔗 Read more: Venture Capital Fund News: Why the "Dry Powder" Myth Is Finally Breaking

A Quick Reality Check on Interest

Here is a bit of bad news: the IRS almost never abates interest just because they feel like it. Interest is statutory. However, if the penalty is removed, the interest associated with that penalty is also removed. It’s a domino effect. If you get a $2,000 penalty wiped out, the few hundred bucks of interest attached to it vanishes too.

Common Blunders That Kill Your Chances

People mess this up all the time. Don't be the person who writes a ten-page letter about their life struggles when applying for FTA. The IRS agent doesn't need to know about your divorce for an FTA request; they just need to see that you filed your 1040s for the last three years.

Another mistake? Requesting abatement before you pay the tax. The failure-to-pay penalty keeps growing every month. If you abate it today but don't pay the bill for six months, the penalty will just start accruing again from the day after the abatement. Wait until the tax is paid in full or you’re safely on a payment plan before you ask for the waiver.

Actionable Steps for Your Tax Debt

If you’re staring at a balance right now, here is exactly what you should do:

- Check your transcripts. Go to the IRS website and pull your "Account Transcript" for the last three years. Look for any "Penalty" codes. If you see $0.00 or "None," you’re a prime candidate for FTA.

- File everything. If you have a missing return from 2022, fix it now. The IRS won't even talk to you about abatement until your filing record is "current."

- Set up a payment plan. Even a $50-a-month agreement makes you "compliant" in the eyes of the IRS for the purpose of this waiver.

- Call or Mail. If the penalty is under $1,000, try the phone first. If it's higher, or if you're an S-Corp/Partnership, use Form 843 and mail it via Certified Mail with Return Receipt.

- Audit the IRS response. When you get the letter saying the penalty is removed, check the new balance. Make sure they also backed out the interest that was calculated on those specific penalties.

The IRS first time penalty abatement is one of the few times the tax code actually works in favor of the "regular" person. It's a reward for being a decent citizen for three years straight. If you qualify, don't leave that money on the table.

Next Steps: Review your most recent IRS notice to identify the specific penalty codes (like 1040 Failure to Pay) and verify your last three years of filing status on your IRS Online Account before requesting the waiver.