Checking the Marksans Pharma share price lately feels like watching a slow-motion recovery. If you’ve been tracking the ticker—MARK on the NSE—you’ve likely seen it hovering around the ₹172.58 mark as of January 16, 2026. Honestly, it’s been a bit of a rollercoaster for the small-cap pharma darling. After hitting a 52-week high of ₹276.40, the stock took a massive 30% hit over the last year.

Retail investors are asking: is this a falling knife or a golden entry point?

The market sentiment is weirdly split. On one hand, you have the technicals looking a bit weak. The stock is trading below its 200-day moving average, which is usually a "stay away" signal for the chart-reading crowd. But then you look at the fundamental story coming out of the Mumbai headquarters, and it’s a completely different vibe. Marksans isn't just surviving; it's expanding its footprint in the most regulated markets in the world.

The Reality Behind the Marksans Pharma Share Price Dip

Why did the price slide? Basically, the first quarter of fiscal 2026 was a "one-off" mess. Pricing pressures in the UK—one of their biggest territories—and a shift in the product mix squeezed the margins. When the market sees margins dip from nearly 60% to the lower 50s, people panic. They sell first and ask questions later.

But here is the thing.

Management, led by Mark Saldanha, isn't sweating it. In the recent Q2 FY26 earnings call, they pointed to a 16% sequential revenue growth. That's a solid rebound. The US market, which accounts for over 50% of their revenue, grew by 27% year-on-year. They are launching new products in digestive health and pain management like there’s no tomorrow.

What the Numbers Actually Tell Us

If you ignore the noisy price action and look at the "hard" data, the picture clears up.

✨ Don't miss: 300 US to NZ dollar: What You’ll Actually Get After Fees and Spreads

- Current Market Cap: Approximately ₹7,805 crore.

- P/E Ratio: Sitting around 22.1x.

- Revenue Target: They’re eyeing ₹3,000 crore within the year, with a massive goal of ₹5,000 crore by 2030.

The P/E is actually quite "middle-of-the-road" compared to the Indian pharma sector median of 25x. It’s not dirt cheap, but it’s certainly not the "overvalued" trap some bears claim it is. Most of the revenue—about 96%—comes from regulated markets like the US, UK, and Australia. That’s a high-quality revenue stream that most small-caps would kill for.

Why the Smart Money is Watching the Goa Expansion

The real catalyst for the Marksans Pharma share price in 2026 isn't the quarterly profit; it's the CAPEX. The company is doubling its manufacturing capacity in India. We are talking about going from 8 billion units to 16 billion units.

They’re spending about ₹100 crore this year on the Goa plant alone.

Specifically, they are expanding tablet capacity by 2.5x and soft gels by 3x. For those who don't know, soft gels are higher-margin products. They are harder to make and face less competition than your run-of-the-mill tablets.

The USFDA "Zero Observations" Win

In this industry, the USFDA is the ultimate judge. Recently, their Unit 2 facility in Verna, Goa, got a clean bill of health—zero Form 483 observations. If you’ve followed pharma stocks for more than a week, you know how rare and valuable that is. It means no regulatory hurdles are blocking their path to the US market for at least the next few years.

Analyst Forecasts: Where is the Stock Heading?

Wall Street and Dalal Street analysts are surprisingly bullish despite the recent price drop. The consensus 1-year price target is ₹237.66. Some analysts are even more aggressive, pushing the target to ₹258.

If the stock is at ₹172 today, that’s a potential upside of over 30%.

- Bull Case: Revenue growth recovers to 15-20%, the UK pricing stabilizing, and the US OTC (over-the-counter) market share increases.

- Bear Case: The working capital cycle stays high at 150 days, and the "falling comet" price trend continues to scare off new buyers.

Honestly, the high working capital is the one red flag I'd watch. It means their money is tied up in inventory and receivables for a long time. It’s not a deal-breaker, but it does limit how fast they can grow without taking on more debt.

Actionable Insights for Investors

If you're looking at the Marksans Pharma share price as a long-term play, you've got to look past the month-to-month volatility.

- Watch the ₹162-₹165 Support: This has historically been a floor. If it breaks this, we might see more pain. If it holds, it’s a classic consolidation.

- Monitor the Feb 5 Board Meeting: They are scheduled to approve the December 31, 2025, quarterly results then. This will be the "proof of the pudding" for the recovery story.

- Evaluate the OTC Strategy: Marksans wants to be a top 5 private-label OTC player in the US. Keep an eye on their "digestive health" segment performance—it's their current growth engine.

Investing in small-cap pharma is never for the faint of heart. You’ve got currency fluctuations, raw material costs, and regulatory risks. But with a clean USFDA record and a massive capacity expansion coming online, Marksans is playing a much larger game than its current share price suggests.

The Next Steps for Your Portfolio

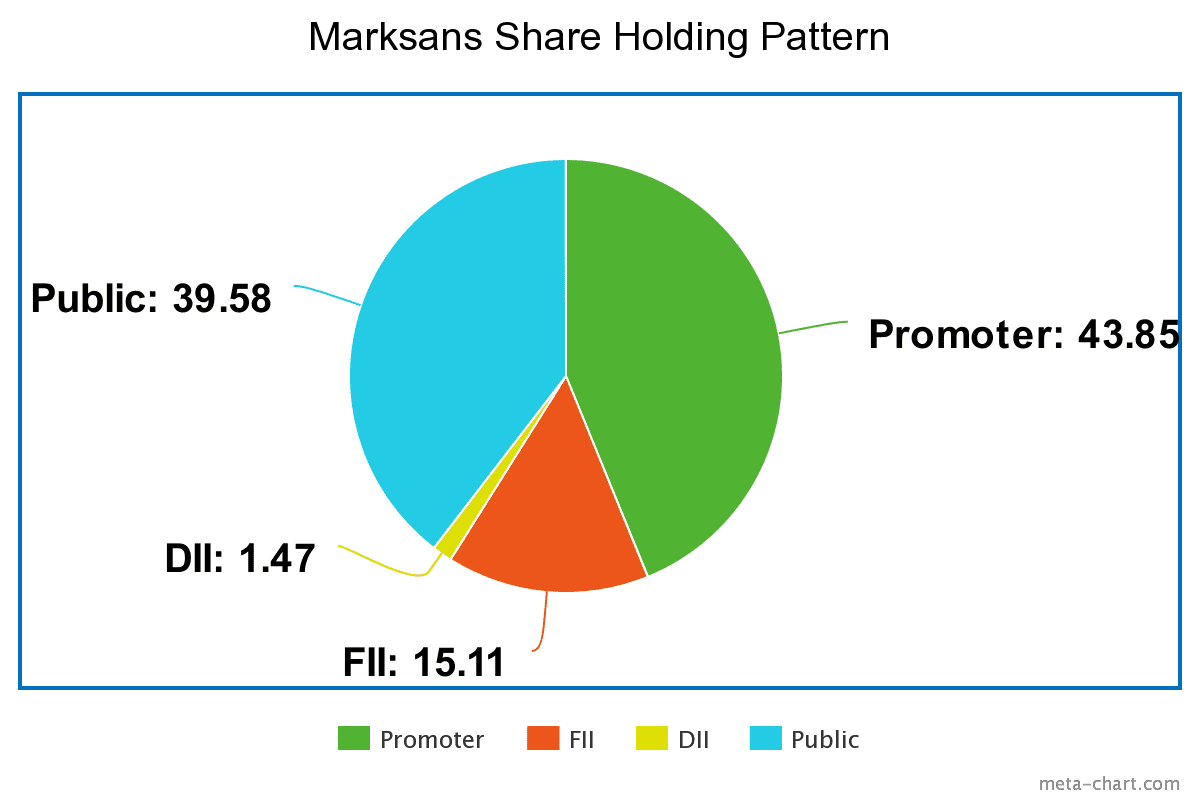

Stop just staring at the daily percentage change. Instead, track the EBITDA margins in the upcoming Q3 report. If they climb back toward 22%, the market will likely re-rate the stock. Also, check if FII (Foreign Institutional Investor) holding increases. Currently, it's around 8.12%. If the big fish start buying again, the retail crowd usually follows suit within weeks.

Check your risk appetite before jumping in. If you can't handle a 10% swing in a week, this isn't the stock for you. But if you’re looking for a manufacturing powerhouse trading at a discount to its historical highs, the current dip is worth a very close look.