You've finally got some extra cash sitting in your checking account. Maybe it was a holiday bonus, or you finally paid off that nagging credit card. Now comes the big question that keeps every DIY investor up at night: should you max out 401k or Roth IRA first?

Honestly, the "right" answer depends on who you ask. If you talk to a hardcore tax optimizer, they’ll start rambling about marginal brackets. A behaviorist might tell you to just "pick one" so you actually save the money. But if you want to be smart about your 2026 tax strategy, you need to look at the math and the rules, which just changed again.

Let's get one thing straight. This isn't just about picking a bucket. It's about how much the government gets to shave off the top of your hard-earned money both now and thirty years from now.

The 2026 Landscape: New Limits and New Rules

The IRS isn't exactly known for being generous, but they did bump the numbers for 2026. If you're under 50, you can now shove $24,500 into your 401(k). That’s a nice little jump from last year. For the Roth IRA, the limit is now $7,500.

🔗 Read more: Marion County Auditor Marion Ohio: What Most People Get Wrong

If you're older, it gets interesting. There’s this new "super catch-up" for people aged 60 to 63. You can put in an extra $11,250. But there’s a catch—literally. If you made more than $145,000 (adjusted for inflation, so check your 2025 W-2), the IRS now mandates that your catch-up contributions must be Roth. No more hiding that extra savings from the taxman today.

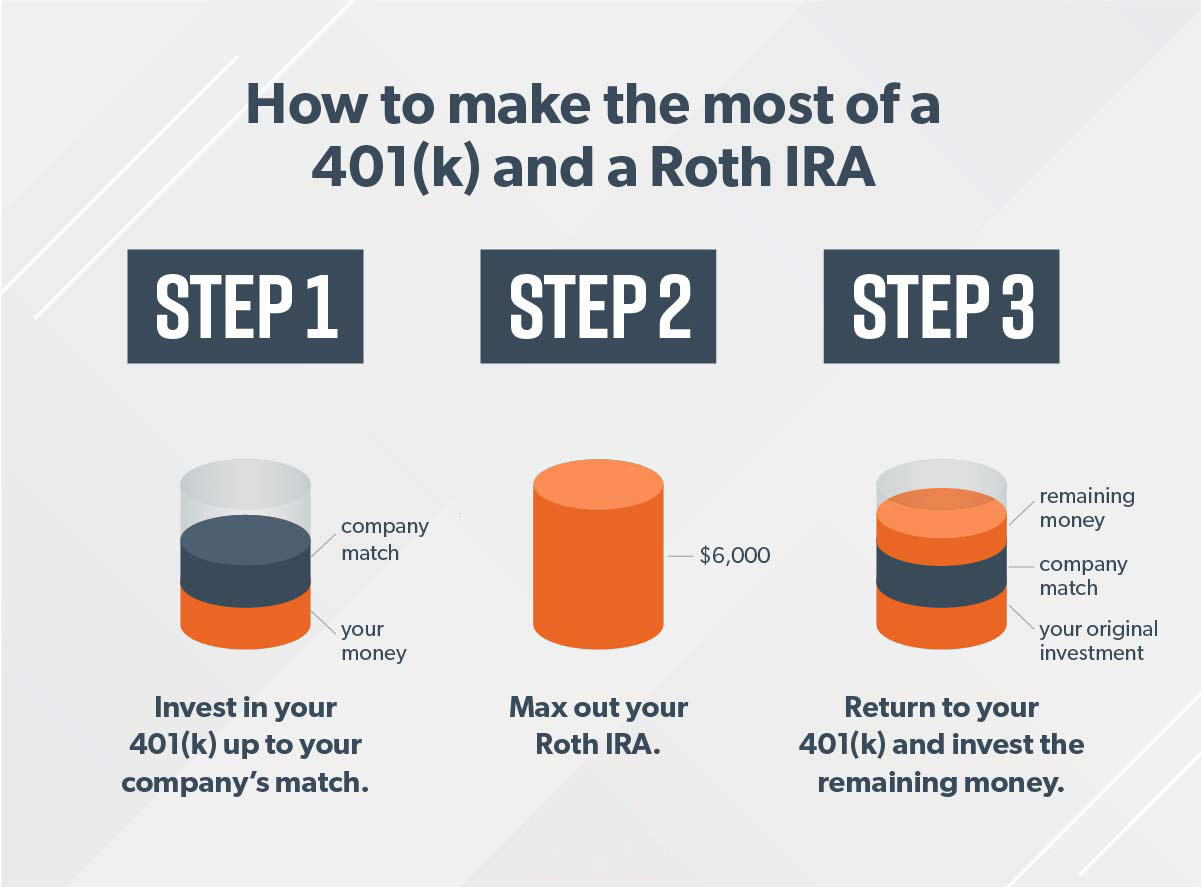

Why the 401(k) Match is Your Only Absolute Priority

Before we even debate the merits of a Roth vs. a Traditional 401(k), we have to talk about the match.

If your boss offers a 401(k) match, that is literally free money. 100% return on investment instantly. You don't pass that up. Ever. Even if the 401(k) investment options are terrible. Even if the fees are high.

Step one: Contribute exactly enough to get the full match. After that? That’s where the real debate begins. Once you’ve captured the "free" money, the decision to continue to max out 401k or Roth IRA becomes a game of tax "now vs. later."

🔗 Read more: Syracuse Car Dealer Lawsuit: What Really Happened with Those Junk Fees

The Case for the Roth IRA: Control and Flexibility

Most people love the Roth IRA because it feels like a secret weapon.

First, there's the flexibility. Unlike a 401(k), you can usually pull your contributions (not the earnings) out of a Roth IRA at any time for any reason without a penalty. It’s a terrible idea to treat your retirement as an emergency fund, but knowing you could helps some people sleep better.

Then there's the investment choice. Most 401(k) plans give you a "menu" of maybe 15 to 20 mutual funds. Some are okay; some are overpriced junk. With a Roth IRA at a place like Fidelity or Vanguard, you can buy literally anything—individual stocks, low-cost ETFs, even REITs.

The Income Trap

Here is the "gotcha" for the Roth IRA: you might be too "rich" to use it. For 2026, if you're single and your Modified Adjusted Gross Income (MAGI) starts creeping toward $153,000, your ability to contribute starts to phase out. For married couples filing jointly, that "no-go" zone starts at $242,000.

If you're above those limits, you're looking at a "Backdoor Roth," which is a legal maneuver involving a non-deductible Traditional IRA. It's a bit of a headache, but worth it for the tax-free growth.

When Maxing Out the 401(k) Actually Wins

There's a specific type of person who should ignore the Roth IRA until they've hit that $24,500 401(k) limit: the high-earner in a high-tax state.

If you live in California or New York and you're in the 32% or 35% federal tax bracket, every dollar you put into a Traditional 401(k) lowers your taxable income today. You’re essentially "betting" that when you retire, your tax rate will be lower than it is now. For many professionals, that’s a very safe bet.

📖 Related: Finding an Employer's EIN: Why It’s Usually Easier Than You Think

Let’s look at an illustrative example.

Imagine you earn $200,000. If you put $24,500 into a Traditional 401(k), you aren't just saving for the future; you're "hiding" $24,500 from the IRS today. At a 32% bracket, that's nearly $7,840 in tax savings this year. You can take that $7,840 and... well, put it in a Roth IRA.

See what we did there?

The "Order of Operations" That Actually Works

If you're feeling stuck, stop trying to do everything at once. Most financial experts, including the folks over at the Bogleheads community, suggest a specific "waterfall" for your cash:

- 401(k) up to the match: Don't leave money on the table.

- HSA (Health Savings Account): If you have a high-deductible plan, this is actually the best account in existence. It’s "triple tax-advantaged"—tax-free in, tax-free growth, and tax-free out for medical bills. In 2026, the limit is $4,400 for individuals and $8,750 for families.

- Roth IRA: Max this out ($7,500) for the flexibility and the tax-free growth.

- Back to the 401(k): Put the rest here until you hit the $24,500 cap.

- Taxable Brokerage: If you still have money left over, you're doing great. Put it in a regular brokerage account.

Misconceptions That Kill Wealth

One huge myth is that you can only have one or the other. You can absolutely do both. In fact, for most people, having a mix of "Pre-tax" (Traditional 401k) and "Post-tax" (Roth IRA) is the ultimate retirement strategy. It’s called tax diversification.

Why? Because nobody knows what tax rates will look like in 2050. If the government decides to hike taxes across the board, you’ll be glad you have a giant pile of Roth money they can't touch. If taxes stay low, your Traditional 401(k) withdrawals won't hurt as much.

Another mistake: waiting until the end of the year.

Time in the market beats timing the market. If you wait until December 2026 to max out 401k or Roth IRA, you missed out on 11 months of potential growth. Automation is your best friend here. Set it and forget it.

The Action Plan

Don't let analysis paralysis stop you. If you're still undecided, here is exactly what to do next:

- Check your 401(k) portal today. Look for the "Employer Match" section. If you aren't contributing at least that percentage, change it right now.

- Evaluate your tax bracket. If you're in the 12% or 22% bracket, prioritize the Roth IRA after you get your 401(k) match. If you're in the 32% bracket or higher, lean harder into the Traditional 401(k) to save on taxes today.

- Open a Roth IRA if you don't have one. It takes ten minutes at any major brokerage. Even if you only put $50 a month in for now, you’re starting the "five-year clock" the IRS requires for tax-free earnings withdrawals.

- Review your HSA eligibility. If your health plan qualifies, max this out before you even think about the Roth IRA. It's the only account that's more powerful than a Roth.

The goal isn't to find the "perfect" strategy. It's to get as much money into tax-advantaged accounts as possible before the calendar flips to 2027. Your future self won't care which bucket you chose first, as long as the buckets are full.