Ever feel like you're running a race where the finish line keeps moving? You're not alone. Most of us look at our bank accounts and wonder if everyone else has some secret cheat code for wealth. To find out where you actually stand, you have to look at median household income in the u.s., which is basically the "middle point" of the American wallet.

The Census Bureau just dropped some fresh numbers, and honestly, they're a bit of a mixed bag. In 2024, the real median household income sat at $83,730. That sounds like a decent chunk of change, right? But here's the kicker: after you adjust for the inflation madness we've all been living through, that number is essentially flat compared to the year before. We’re working harder, but the "real" value of our paychecks is just sort of treading water.

Why the "Median" Matters More Than the "Average"

If you're talking to a neighbor about money, they might mention the "average" income. Take my advice: ignore that number. Averages are easily skewed by billionaires. If Jeff Bezos walks into a dive bar, the average person in that room is suddenly a multi-millionaire on paper. But that doesn't help the guy at the end of the bar trying to pay his tab.

The median is different. It’s the literal middle. If you lined up every single household in America from the poorest to the richest, the household right in the center—the 65 millionth one—is the median. Half of the country makes more, half makes less. It’s a much more "honest" look at what life is like for the typical American family.

👉 See also: Martha Stewart Stock Value: Why You Can’t Actually Buy MSO Anymore

The Real Numbers by the Slice

Data isn't just one big blob. Depending on who you are and where you live, that $83,730 figure might feel like a fortune or a total joke.

- Asian households are currently leading the pack with a median income around $112,000.

- Non-Hispanic White households come in next, hovering near $92,530.

- Hispanic households saw a nice bump recently, climbing to about $70,950.

- Black households have had a tougher run, with the median sitting at $56,020, which actually dipped slightly in recent reports.

Education is still the biggest lever you can pull. If you've got a professional degree, you’re looking at weekly earnings around $1,912. Compare that to someone without a high school diploma pulling in $750 a week. That’s a massive gap that adds up to tens of thousands of dollars every single year.

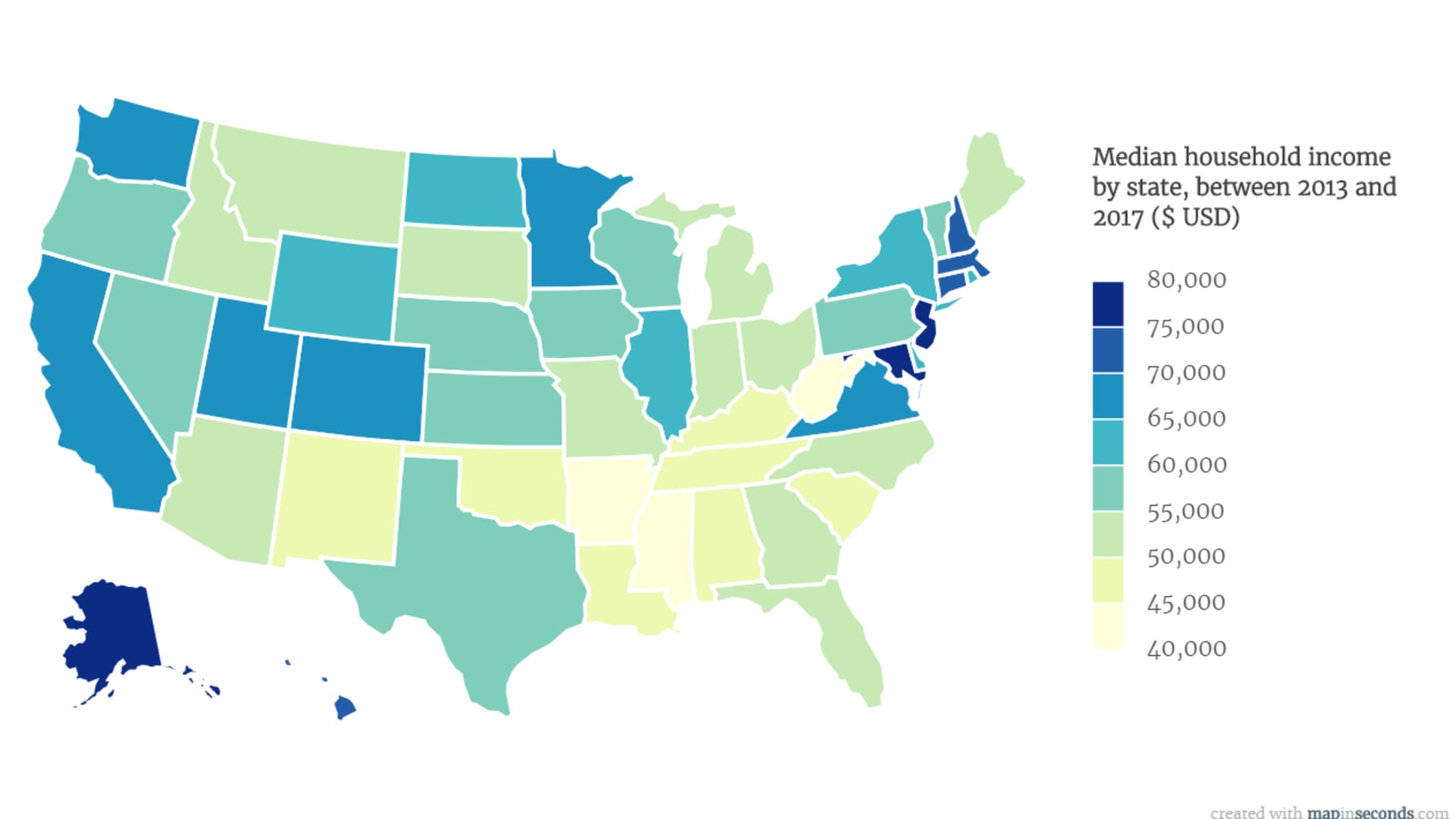

The Geography of Your Paycheck

Where you park your car at night has a massive impact on your bottom line. We’ve all heard that California and New York are expensive, but the income side of the equation is wild.

Maryland and Massachusetts are consistently battling for the top spot, with median incomes often crossing the $100,000 threshold. On the flip side, if you're in Mississippi or West Virginia, the median is closer to $55,000 or $60,000.

The Top Tiers by State (2025-2026 Trends)

- Maryland: $101,652

- Massachusetts: $101,341

- New Jersey: $101,050

- California: $100,149

It’s not all sunshine and rainbows in high-income states, though. You’ve gotta factor in the "cost of existing." Making six figures in San Francisco often feels like making $50k in a smaller Midwest town once you see the rent prices.

The Affordability Squeeze of 2026

We're seeing a weird phenomenon this year. Lawrence Yun, the Chief Economist at the National Association of Realtors, noted that home prices are finally moderating a bit—growing maybe 2% to 3%. In theory, wage growth is finally starting to outpace that.

But talk to anyone on the street and they’ll tell you the same thing: housing is still the monster in the room. Even if your income goes up 4%, if your rent or mortgage eats 40% of your take-home pay, you aren't feeling "richer."

Liana Fox and the team at the Census Bureau have been pointing out that while "money income" looks stable, "post-tax" income tells a different story. When you factor in the sunsetting of various tax credits and the rising cost of insurance (which is skyrocketing in places like Florida and Texas due to climate risks), the "typical" household is feeling a significant pinch.

What You Can Actually Do With This Information

Knowing the median household income in the u.s. isn't just for trivia night. It's a benchmark for your own life. If you’re significantly below the median for your career field or your state, it might be time for a "check-in" with your employer or a pivot in your strategy.

✨ Don't miss: Portland General Electric Share Price: What Most People Get Wrong

Audit your "Real" Income: Don't just look at your gross salary. Subtract your fixed costs—housing, transit, and that ever-climbing insurance premium. If that "disposable" number isn't growing year-over-year, you’re technically falling behind even if you got a 3% raise.

Location Arbitrage: With remote work still being a thing for many, moving from a high-cost/high-median state to a mid-range state while keeping a similar salary is the fastest way to jump into the "upper-income" bracket.

Skill Stacking: The data is clear: the gap between a high school diploma and a Bachelor's degree is about $600 a week. If you’re stuck in the lower-median brackets, certifications or specialized trade training are the most reliable ladders out.

Stop comparing yourself to the influencers on your feed. Most of that is fake anyway. Compare yourself to the median. It’s the most grounded way to understand where you sit in the Great American Economy.

Next Steps for Your Finances:

- Check the specific median income for your Metropolitan Statistical Area (MSA) using the Census Bureau’s "Data Mapper" tool to see local cost-of-living adjustments.

- Review your tax withholdings for 2026; many households are seeing "bracket creep" where raises push them into higher tax tiers without increasing their actual buying power.

- If your household income is between two-thirds and double the national median ($56k to $168k roughly), you are officially "Middle Class" by Pew Research standards—use this to evaluate if your current savings rate matches your peers.