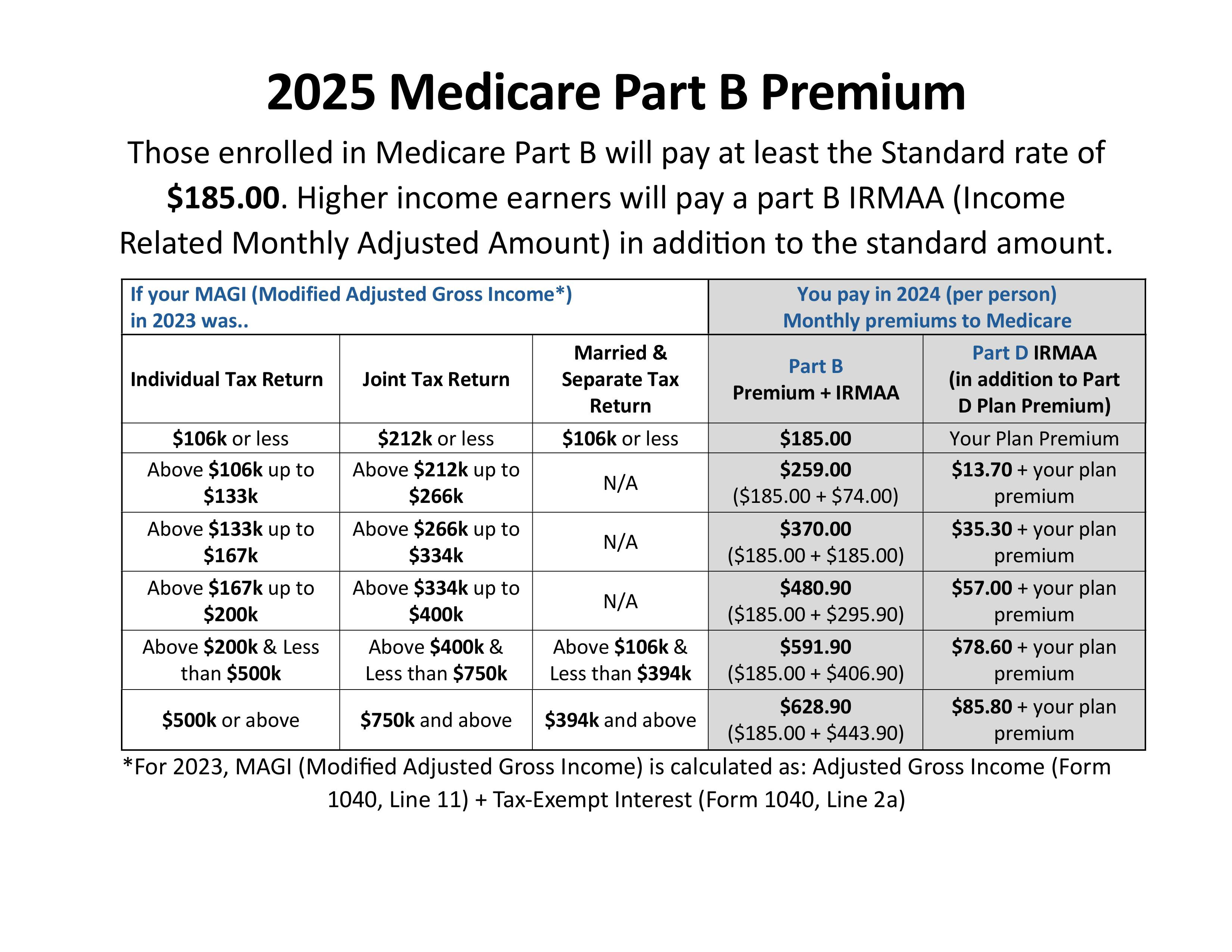

Medicare is a maze. Most people get through Part A and Part B and think they’re done, but then they hit the pharmacy counter and realize they’ve missed a massive piece of the puzzle. That’s usually when the question "what is Medicare Part D" starts feeling a lot more urgent. Basically, Part D is the federal government’s way of handling your prescription drugs. It isn't something you get automatically from Social Security, and it definitely isn't free.

Think of it as an add-on. You buy it from private insurance companies like UnitedHealthcare, Aetna, or Blue Cross Blue Shield. The government sets the rules, but the corporations run the show. If you don't sign up when you’re first eligible, the government actually hits you with a late enrollment penalty that lasts for the rest of your life. It’s a "pay now or pay much more later" kind of situation.

How the Money Actually Moves

Most people assume insurance is simple: you pay a premium, you get your meds. Medicare Part D is way more chaotic than that. You have four distinct phases of coverage, and depending on how many prescriptions you take, you might cycle through all of them in a single year.

First, there’s the deductible. In 2026, the maximum deductible is capped at a specific amount by the Centers for Medicare & Medicaid Services (CMS), but many plans offer a $0 deductible to lure you in. Once you've paid that, you enter Initial Coverage. Here, you pay a copay—maybe $10 for a generic or $47 for a brand name—and the plan covers the rest.

Then things get weird.

Have you heard of the "Donut Hole"? For years, this was the most hated part of Medicare. You’d hit a certain limit in spending, and suddenly you were responsible for a huge chunk of the drug costs yourself. However, thanks to the Inflation Reduction Act, the landscape has shifted. The dreaded coverage gap is effectively being phased out and replaced by a hard cap on out-of-pocket spending. This is a massive win for seniors on high-cost specialty drugs for things like cancer or rheumatoid arthritis.

The $2,000 Cap is the Real Game Changer

Starting recently, there is a $2,000 out-of-pocket maximum. This is the biggest shift in Medicare Part D since its inception in 2006. Before this, if you were on a drug that cost $10,000 a month, you could still end up paying thousands of dollars every year even with "good" insurance. Now, once you hit that $2,000 mark, you are done. Your plan and the government pick up the rest of the tab for the calendar year.

It's a relief. Honestly, it’s about time.

Choosing a Plan Without Losing Your Mind

You can't just pick the plan with the lowest monthly premium and call it a day. That is the fastest way to get scammed by the math. Every Part D plan has a formulary. This is just a fancy word for a list of drugs they actually agree to cover.

If your specific blood pressure medication isn't on that list, the plan won't pay a dime.

Drugs are organized into "Tiers."

📖 Related: Old Man Big Tits: Why Male Chest Growth Happens and What to Do About It

- Tier 1 is usually "preferred generics" (the cheap stuff).

- Tier 2 is "non-preferred generics."

- Tier 3 is "preferred brands."

- Tier 4 and 5 are where it gets expensive—specialty drugs and biologics.

Always, always check your specific medications against the plan's formulary before signing up. You can do this on Medicare.gov using their plan finder tool. It’s one of the few government websites that actually works pretty well. You put in your drugs and your zip code, and it spits out the total annual cost (premium + copays). That "Total Annual Cost" number is the only one you should care about.

The Penalty That Never Goes Away

Let's talk about the Part D Late Enrollment Penalty. It’s mean. If you go 63 days or more without "creditable" prescription drug coverage after your Initial Enrollment Period ends, Medicare adds a penalty to your premium.

How much? It's 1% of the "national base beneficiary premium" for every month you were uncovered.

If you go three years without a plan because "I don't take any pills anyway," you'll pay an extra 36% on your premium every single month for as long as you have Medicare. It doesn't matter if you're 65 or 95. The lesson here is simple: even if you take zero medications, buy the cheapest "naked" plan available just to keep your spot in line and avoid the fine.

Extra Help and Low-Income Subsidies

Not everyone has to struggle with these costs. There’s a program called Extra Help (officially the Low-Income Subsidy). If your income and resources are below a certain threshold, the government helps pay for your Part D premiums, deductibles, and copays.

🔗 Read more: Why COVID Razor Blade Throat Is the Symptom Everyone Is Searching For

Many people qualify for this and have no idea. If you’re eligible, you won't face the late enrollment penalty, and you won't have a coverage gap. It basically turns Medicare Part D into a much more manageable system. You can apply through the Social Security Administration. It's worth the paperwork.

The Truth About Medicare Advantage (Part C)

A lot of people ask, "Wait, I have a Medicare Advantage plan, do I need Part D?"

Usually, no. Most Medicare Advantage plans (Part C) bundle hospital, medical, and drug coverage together into one package. These are called MAPDs. If you have one of these, you can't also buy a standalone Part D plan. If you try to, Medicare might actually kick you out of your Advantage plan and put you back on Original Medicare.

It’s a bit of a "one or the other" choice. If you prefer Original Medicare with a Medigap supplement, you must buy a separate Part D plan. If you like the all-in-one HMO or PPO style of Medicare Advantage, the drug coverage is almost certainly already in there.

What Medicare Part D Doesn't Cover

It’s not a magic wand. Part D is specifically for outpatient prescription drugs you get at a pharmacy. It generally won't cover:

- Drugs used for weight loss (though this is a massive area of legal and political debate right now with drugs like Wegovy).

- Fertility drugs.

- Cosmetic drugs (like Botox for wrinkles, though it might be covered for migraines under Part B).

- Over-the-counter (OTC) meds like aspirin or cough syrup.

- Erectile dysfunction drugs (usually).

For things like vaccinations, it’s a split. Some shots, like the flu or pneumonia vaccines, are covered by Part B. Others, like the Shingles vaccine (Shingrix), are covered by Part D. Since 2023, most Part D plans must provide recommended adult vaccines at zero cost to you. That was a huge change that saved people about $200 per Shingles series.

👉 See also: Winn Army Community Hospital Emergency Room: What to Know Before You Go

How to Handle the "Plan Catch-22"

Every year, between October 15 and December 7, you get a chance to change your plan. This is called the Annual Election Period. Use it.

Insurance companies change their formularies every single year. Your drug might be Tier 1 this year and Tier 3 next year. Or they might stop covering it entirely. If you just let your plan "auto-renew" without checking, you could be in for a nasty surprise at the pharmacy in January.

Check the "Annual Notice of Change" (ANOC) that your plan mails you in September. It’s a boring document, but it tells you exactly what is changing for the upcoming year.

Your Immediate Action Plan

Don't wait until you're standing at the CVS counter to figure this out. If you're approaching 65 or already on Medicare, follow these steps to secure your drug coverage:

- Audit your medicine cabinet. List every prescription, the dosage, and how often you refill it.

- Use the Medicare Plan Finder. Go to Medicare.gov and enter your list. Look for the "Total Annual Cost," not just the monthly premium.

- Check for "Preferred Pharmacies." Most Part D plans have a network. If you go to a pharmacy outside that network, you might pay double. Ensure your favorite local pharmacy is "preferred" by the plan you choose.

- Confirm your "Creditable Coverage." If you’re still working and have insurance through an employer, ask your HR department for a "Notice of Creditable Coverage." Keep this in a safe place. You’ll need it to prove you don't owe a late penalty when you eventually switch to Medicare.

- Apply for Extra Help. If your monthly income is limited, visit the Social Security website to see if you qualify for the Low-Income Subsidy. It can save you thousands.

Prescription drug costs are one of the biggest threats to a retirement budget. Understanding what Medicare Part D is—and more importantly, how to manipulate the rules in your favor—is the best way to keep your savings intact. Stay proactive. The rules change almost every year, and staying informed is the only way to avoid overpaying for the medications you need to stay healthy.