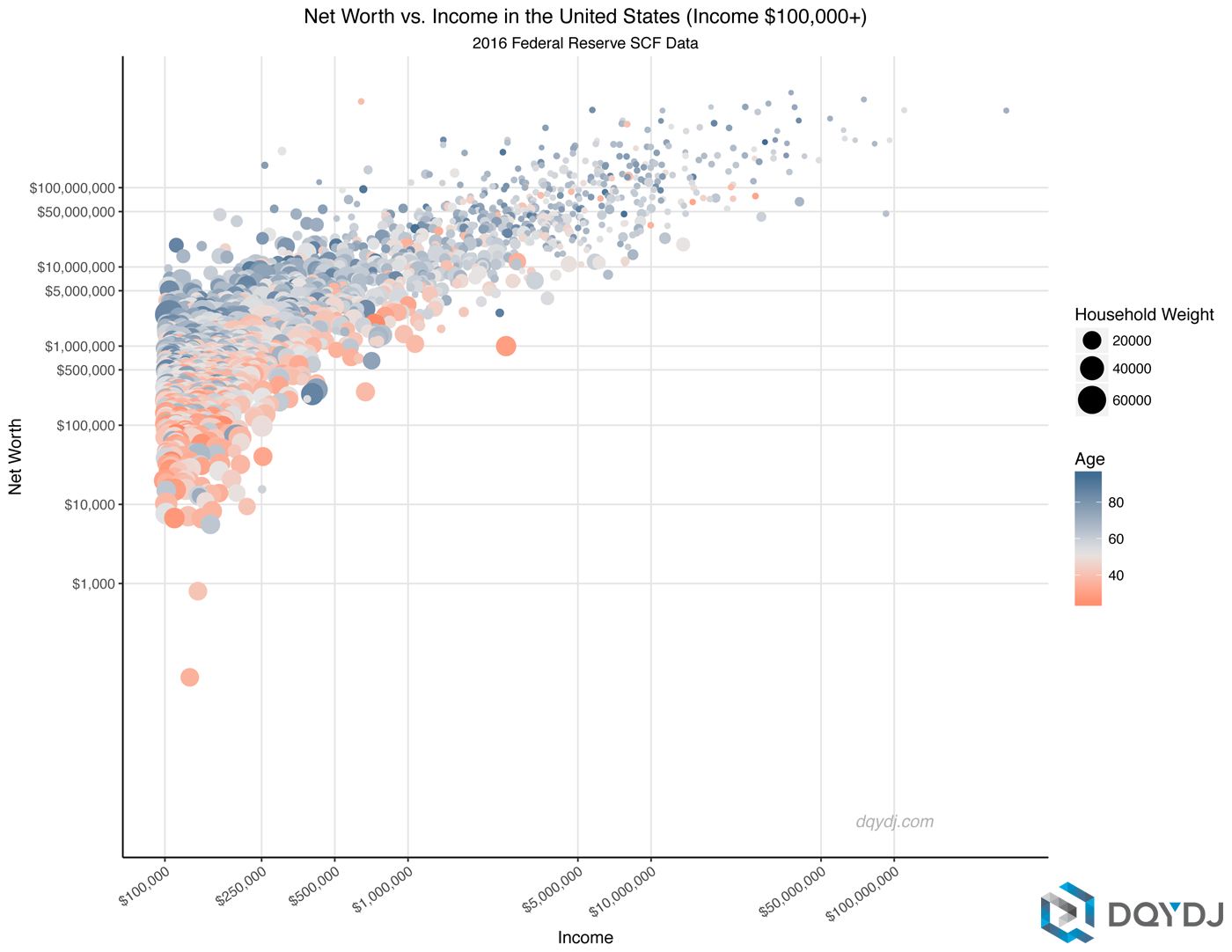

You’ve probably seen the headlines about the "average" American being a millionaire. It sounds great, doesn't it? But if you look at your own bank account and feel a pang of "where is my million dollars," you aren't alone. Honestly, the word "average" is doing a lot of heavy lifting in those reports.

When we talk about middle class net worth, we’re actually looking at a landscape that has shifted dramatically as we move through 2026. The gap between the "mean" (the average) and the "median" (the middle point) is a chasm. Most people aren't sitting on a seven-figure pile of cash. Instead, they are navigating a world of rising home equity, stubborn inflation, and retirement accounts that are finally starting to recover from the volatility of the mid-2020s.

The Reality of the Numbers

The Federal Reserve's recent data—including the momentum leading into 2026—paints a startling picture. If you take every household in the U.S. and average their wealth, you get a number north of $1 million. But that’s skewed by the billionaires. It’s like Jeff Bezos walking into a dive bar; suddenly, the "average" person in that bar is a multi-millionaire.

For the actual middle class—defined by Pew Research as those earning between two-thirds and double the national median income—the middle class net worth is much more grounded.

Specifically, the median net worth for a typical middle-class household currently hovers around $192,900 to $204,100. This is the "real" middle. Half of the people in this bracket have more, and half have less. If you’re at this number, you’re doing exactly what the stats say you should be.

Where is the money hidden?

It’s not in gold bars under the bed. For the vast majority of middle-income families, wealth is tied up in two very specific places:

- Primary Residence: Home equity makes up the lion's share of net worth. With home prices hitting record highs in mid-2025, many families are "house rich" but "cash poor."

- Retirement Accounts: Think 401(k)s and IRAs. The "AI Gold Rush" of 2025 gave these a nice bump, but it’s money you can’t touch without a penalty.

Middle Class Net Worth by Age: The Staircase Effect

Net worth isn't a static number; it's a lifecycle. A 25-year-old with $10,000 is often in a better relative position than a 50-year-old with $100,000.

In your 20s, you’re basically in the "negative or zero" phase. Student loans and entry-level salaries mean the median net worth for those under 35 is only about $39,000. It feels low because it is. You’re just starting the engine.

By the time you hit your 40s, things start to get interesting. This is the "accumulation phase." The median jumps to roughly $135,300. You’ve likely bought a home, and you've been contributing to a retirement plan for a decade.

The peak happens in your 60s. Right before retirement, the median middle class net worth reaches about $410,000. This is the nest egg. It sounds like a lot until you realize it has to last 20 or 30 years.

The Stealth Killers of Middle Class Wealth

Why does it feel harder to build wealth now than it did for our parents? It’s not just "avocado toast."

First, there’s the "lifestyle creep" fueled by the 2026 digital economy. We’re spending more on subscriptions, high-speed connectivity, and "convenience" services than any previous generation.

Second, the cost of "entry-level" wealth has skyrocketed. In 1970, a middle-class income could easily afford a home that would eventually become a massive asset. Today, that same home requires a down payment that often takes a decade to save.

💡 You might also like: Nifty 500 Momentum 50: Is This Strategy Actually Sustainable in a Volatile Market?

The Debt Factor

Debt is the anchor. While the upper class uses debt as a tool (like low-interest business loans), the middle class often uses "consumer credit."

- Credit Card Debt: Reached record highs in late 2025.

- Auto Loans: The average car payment is now a significant chunk of the monthly budget.

- Mortgages: Even with rates settling around 6.5%, the sheer size of the loans means more interest paid over time.

How to Actually Move the Needle

If you want to beat the median and move into the upper-middle-class tier—where net worth starts at roughly $800,000—the strategy hasn't changed, even if the tools have.

Automate the boring stuff. You’ve heard it before, but most people don't do it. If you don't see the money, you don't spend it. Increase your 401(k) contribution by just 1% today.

Focus on the "Big Three" expenses. Housing, transportation, and food. If you can keep these under control, the rest of your budget almost takes care of itself. Buying a used car instead of a new one in 2026 can save you $500 a month. That’s $6,000 a year straight into an index fund.

Kill high-interest debt with a vengeance. Any debt over 7% is a financial emergency. You cannot out-invest a 22% credit card interest rate. It’s mathematically impossible.

🔗 Read more: Mirae Asset NYSE FANG+ ETF Explained: What Most People Get Wrong

Actionable Steps for 2026

- Calculate your "Real" Net Worth: Use a simple tool or a spreadsheet. Assets (what you own) minus Liabilities (what you owe). Don't count your "estimated" inheritance.

- The 1% Rule: Increase your savings rate by 1% every six months. You won't feel the pinch, but the compounding effect over a decade is massive.

- Diversify Away from the House: If 90% of your wealth is in your home, you’re vulnerable to a local real estate dip. Try to build your "liquid" net worth in brokerage accounts.

- Audit Your Subscriptions: In 2026, "subscription fatigue" is real. Cancel two things today that you haven't used in a month.

Building middle class net worth isn't about hitting a home run with a meme stock or a lucky break. It's about the "boring" middle—the consistent, unglamorous habit of spending less than you earn and letting time do the heavy lifting. You aren't behind; you're just in the middle of the story.

To start, pull your latest credit card statement and your 401(k) balance. Seeing the numbers in black and white is the only way to stop guessing and start growing.