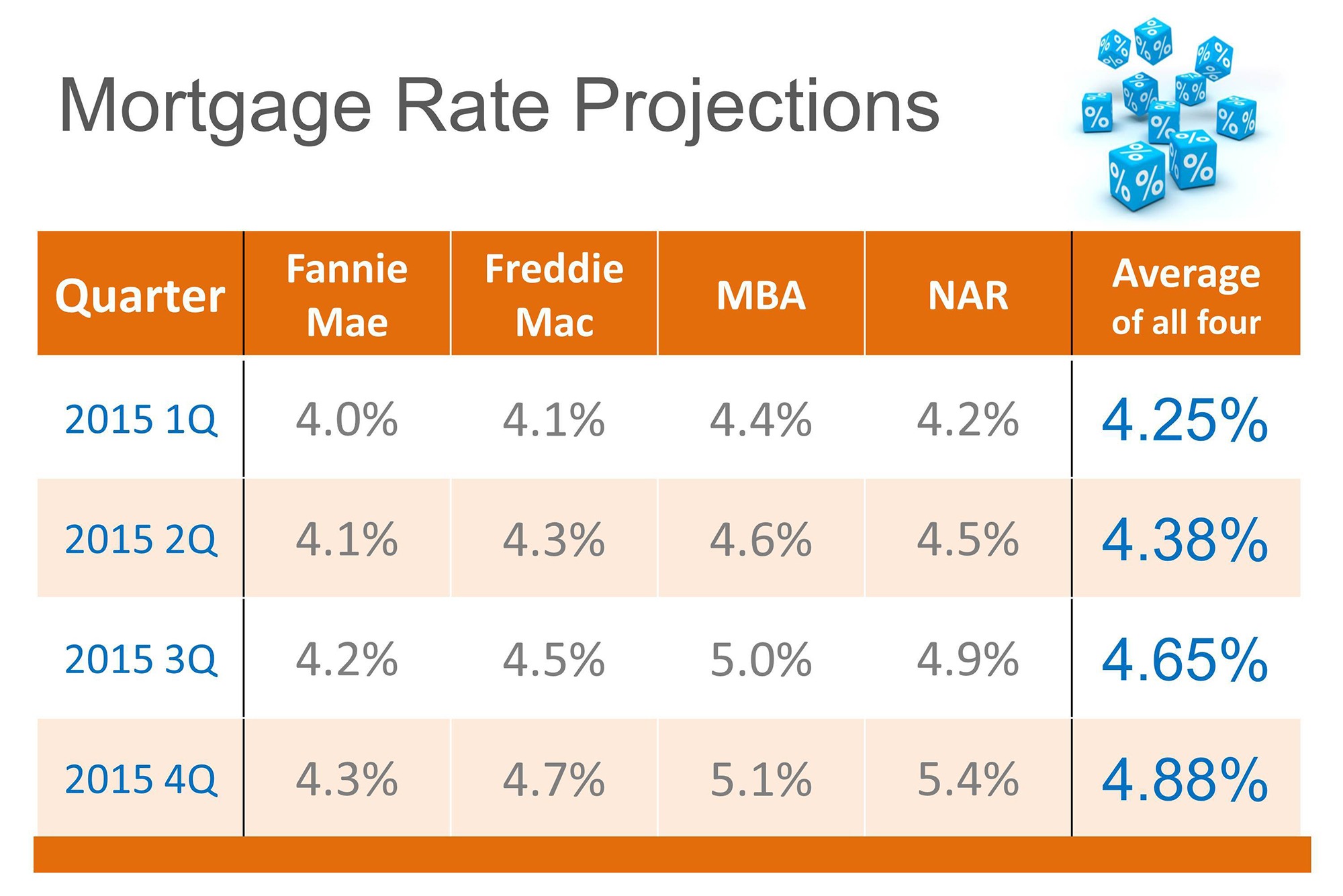

If you spent any part of late 2024 listening to the talking heads on financial news, you probably heard the same song over and over: rates are going to plummet. Everyone had a theory. The Fed would pivot hard, inflation would vanish into the ether, and we’d all be signing papers for 5% mortgages by the time the 2025 spring thaw hit.

Well, it’s early 2026 now. Looking back, mortgage rates predictions 2025 turned out to be a lot messier than the brochures suggested.

Honestly, the "great descent" everyone promised felt more like a slow, painful crawl through the mud. While we did see rates ease off those terrifying 7% and 8% peaks from a couple of years ago, the reality of 2025 was defined by one word: stickiness. Rates didn't just drop off a cliff; they hovered, teased us, and then settled into what many are now calling the "new normal" of the low 6% range.

What actually moved the needle in 2025?

It’s easy to blame the Federal Reserve for everything, but that’s a bit of a lazy take. Yes, the Fed cut rates three times in 2025—specifically at their September, October, and December meetings—bringing the federal funds rate down to a range of 3.50% to 3.75%. But mortgage rates aren't a mirror image of the Fed's overnight rate. They’re more like a moody teenager following the 10-year Treasury yield, which stayed stubbornly high for most of the year.

Why?

Inflation wasn't the ghost people thought it was. It stuck around like a bad houseguest. Throughout 2025, we dealt with "tariff dynamics" and a government shutdown that made economic data look like a scrambled TV signal. When the data is messy, investors get nervous. When investors get nervous, they demand higher yields on bonds, and that keeps your 30-year fixed rate sitting right around 6.1% to 6.3%.

I was chatting with a loan officer in D.C. recently who told me his clients are still shell-shocked. A few years ago, these folks were looking at $4,500 monthly payments. Now? For the same house, they’re staring down $8,000. It’s a brutal pill to swallow, even with the slight relief we saw toward the tail end of the year.

The 2025 reality check: By the numbers

If we look at the actual data from the last twelve months, the downward trend was there, but it was incredibly shallow.

- January 2025: We started the year with a gut-punch average of 7.04%.

- The Summer Slump: Rates teased the high 6s for months as the labor market started to show some cracks.

- December 2025: By the time the holidays rolled around, the average had finally dipped to about 6.18%.

Fannie Mae and the Mortgage Bankers Association (MBA) spent the whole year revising their homework. In March 2025, Fannie Mae thought we’d end the year at 6.3%. They weren't far off, but the path to get there was anything but a straight line. The "lock-in effect"—that phenomenon where people refuse to sell because they’re sitting on a 3% rate—began to crack, but it didn't break.

Why the "Lock-In" is finally losing its grip

Something fascinating happened in late 2025. For the first time since the pandemic, the share of people with mortgage rates above 6% actually surpassed the share of people with rates below 3%.

Think about that.

It means the market is finally turning over. People are tired of waiting. Life happens—babies are born, couples get divorced, jobs move to different states. You can only put your life on hold for a lower interest rate for so long before the four walls of your "starter home" start to feel like a prison. Realtor.com’s Danielle Hale noted that this was a major inflection point. We’re finally seeing the "ultra-low-rate era" fade into the rearview mirror.

Looking ahead: Is 2026 the year of the 5%?

If you’re waiting for 3% or 4% to come back, I’ve got some bad news: it’s probably not happening in our lifetime unless the economy falls into a black hole. Experts from Morgan Stanley and Goldman Sachs are looking at the current landscape and seeing a very flat horizon.

There's a chance we see 5.75% or 5.9% by mid-2026 if the Fed keeps its cool, but most forecasts, including those from Wells Fargo and the MBA, suggest we’ll be lucky to stay in the low 6s. The MBA is actually being the "party pooper" of the group, predicting rates might even tick back up to 6.4% if the labor market stays too strong.

It’s a weird paradox. A "good" economy with lots of jobs actually keeps mortgage rates higher. We almost need a little bit of economic pain to get the "relief" of lower borrowing costs.

Actionable steps for the current market

So, where does that leave you? If you’ve been sitting on the sidelines watching mortgage rates predictions 2025 play out, here is how you should actually handle the next few months:

🔗 Read more: Knight-Swift Customer Impact Tariff Uncertainty: What Really Happened

Stop timing the bottom.

The "bottom" of the market is only visible in the rearview mirror. If you find a house you love and can afford the payment at 6.1%, buy it. If rates drop to 5.2% in two years, you refinance. If they go back to 7.5%, you’ll look like a genius.

Watch the "Spread," not just the Fed.

The gap between the 10-year Treasury and mortgage rates (the "spread") has been historically wide—around 218 basis points recently. Usually, it's closer to 170. If that gap shrinks (which happens as the market stabilizes), mortgage rates could drop even if the Fed does absolutely nothing.

Get your credit in "A+" shape.

In a 6% environment, the difference between a 680 and a 740 credit score can be thousands of dollars a year in interest. Don't leave money on the table because of a missed credit card payment from three years ago.

Explore the "New" Refinance.

Refi volume is actually expected to jump by 30% this year. Why? Because the people who bought at 7.8% in late 2023 or 7% in early 2025 are finally seeing a window to shave 1% off their rate. It's not a 3% "legacy" rate, but it’s a meaningful win for the monthly budget.

The "Great Housing Reset" isn't a single event; it's a slow transition. We're moving away from the era of free money and into an era where 6% is just the price of doing business. It’s not as fun, but at least the volatility is finally starting to die down.

✨ Don't miss: Rite Aid Scalp Ave Johnstown PA: What Residents Need to Know About the Richland Mall Store

To stay ahead of the game, check your local inventory levels. While national trends matter, housing is ultimately local. Some markets, like the NYC suburbs or parts of the Midwest, are still seeing bidding wars despite these rates. Others, like coastal Florida, are cooling off fast due to rising insurance costs. Know your neighborhood before you commit to the rate.