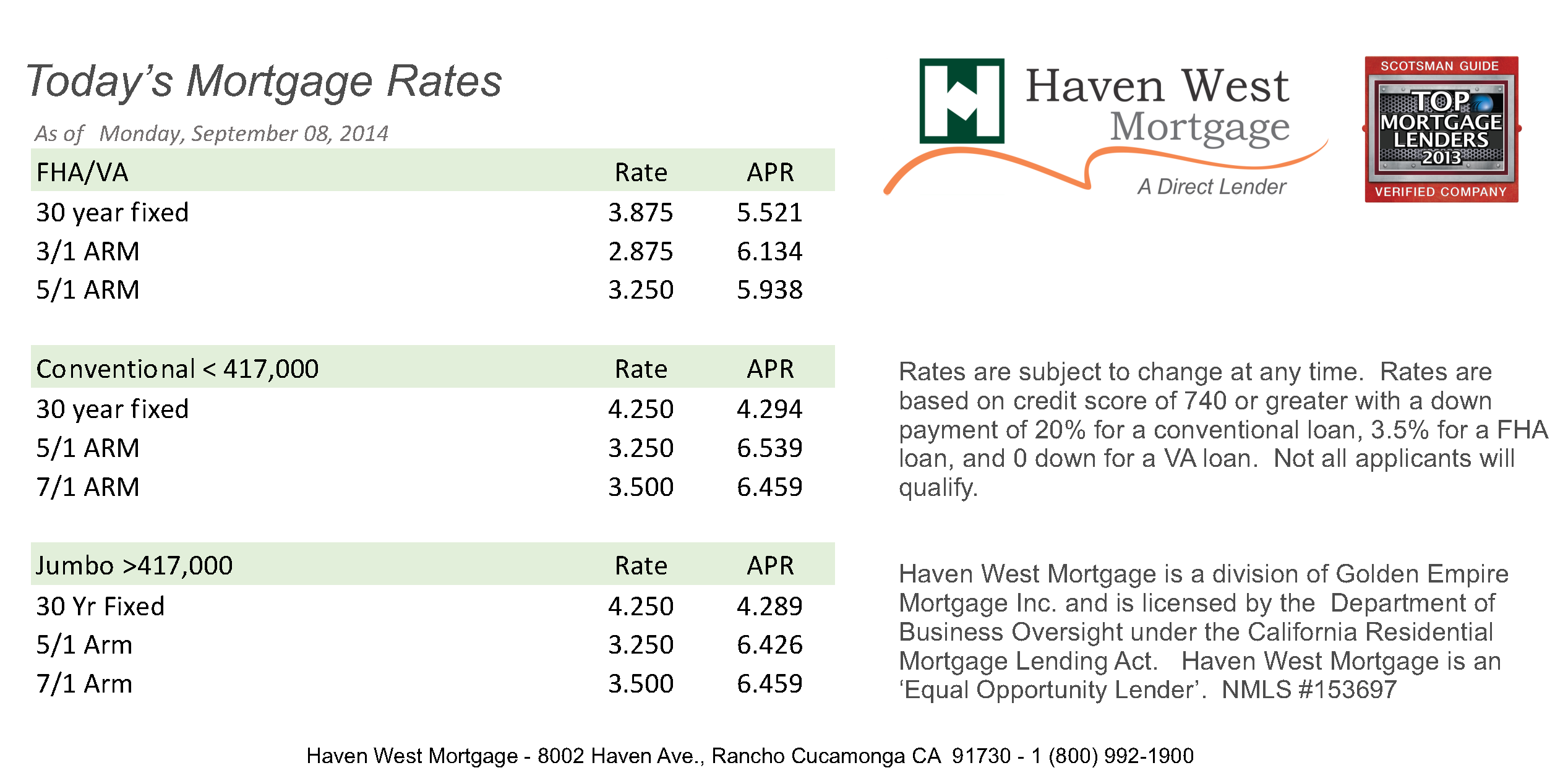

If you’re staring at Zillow listings and wondering if you should pull the trigger, the question of what are the mortgage rates today is probably living rent-free in your head. It’s a weird time. For a while there, everyone was waiting for some sort of massive "crash" in rates that just never quite showed up.

Honestly, the market feels a bit more settled now than it did a year ago. As of Sunday, January 18, 2026, the national average for a 30-year fixed mortgage is sitting right around 6.11%. Some lenders are quoting closer to 6.18% APR once you factor in the fees.

It’s not the 3% we saw during the pandemic (and let's be real, those days are gone). But it’s also a far cry from the terrifying 7.5% or 8% peaks that made everyone want to hide their wallets.

Breaking Down Today's Numbers by Loan Type

Not all mortgages are created equal. Depending on your credit score or whether you served in the military, your "real" rate might look a lot different from the headline news.

📖 Related: Birr to Dollar Exchange: Why the Official Rate is Only Half the Story

The 30-Year Fixed

This is the big one. Most people go this route because it’s predictable. Currently, you’re looking at an interest rate of about 6.11%. If you’re looking to refinance an old loan from 2023, be prepared for a slightly higher hit; refinance rates are averaging roughly 6.56%.

The 15-Year Fixed

If you can stomach the higher monthly payment, the 15-year is actually looking pretty decent. The average is about 5.47%. It’s a solid way to save literally hundreds of thousands in interest over the life of the loan, provided your budget has the breathing room.

FHA and VA Loans

FHA rates are hovering around 5.78% today. These are great if your credit isn't "perfect" or if you have a smaller down payment. VA loans, which are for veterans and active-duty members, are even more competitive, often dipping down to 5.375% for those with solid credit.

What are the mortgage rates today doing to your monthly budget?

Numbers are just numbers until you apply them to a house. Let's say you're looking at a $400,000 home with 20% down.

At a 6.11% rate, your principal and interest payment is roughly $1,942. If rates were to drop to 5.5%, that payment falls to about $1,817. That’s a $125 difference. Is it worth waiting six months or a year for $125?

Maybe.

But if home prices rise by 3% in that same timeframe—which some analysts like those at Morgan Stanley are predicting for 2026—that $400,000 house now costs $412,000. You basically lose your "savings" to the higher purchase price.

Why aren't rates falling faster?

It’s easy to blame the Federal Reserve. And sure, they have a lot to do with it. The Fed kept the benchmark rate steady at its last meeting, and many experts from J.P. Morgan and Goldman Sachs think they might stay on hold for a good chunk of 2026.

But here is the thing: mortgage rates actually track the 10-year Treasury yield more closely than the Fed’s short-term moves.

Investors are still a bit nervous about inflation sticking around. Because of that, they’re demanding higher yields, which keeps your mortgage rate stuck in the 6% range. We’ve seen a "lock-in effect" where people with 3% rates refuse to sell, which keeps housing inventory low and prices high. It’s a cycle that’s been tough to break.

The "Marry the House, Date the Rate" Trap

You’ve probably heard this cheesy phrase from a real estate agent. The idea is that you buy the house now and just refinance later when rates drop.

Be careful with this. Refinancing isn't free. You usually have to pay 2% to 5% of the loan amount in closing costs. If you buy today at 6.1% and rates drop to 5.7% next year, it might take you three or four years just to break even on the cost of the refinance.

Only buy if you can actually afford the payment today. If a lower rate comes along later, treat it like a bonus, not a requirement for survival.

Actionable Steps for Borrowers This Week

The market is moving fast, but you can still get the upper hand if you're smart about the process.

- Check your credit like a hawk. A jump from a 680 to a 740 credit score can move your rate by half a percent. In today's market, that's the difference between an "okay" deal and a great one.

- Look into "Rate Buydowns." Many sellers are still willing to pay for a 2-1 buydown. This means your rate is 2% lower the first year and 1% lower the second year. It’s a great way to ease into a mortgage.

- Get quotes from three different sources. Don't just go to your local bank. Check a mortgage broker and an online lender. You’d be surprised how much "overhead" varies between companies.

- Ask about "Float Down" options. If you lock in a rate today but rates drop before you close, some lenders let you grab the lower rate for a small fee. It gives you some peace of mind.

If you are ready to move, don't let the "perfect" be the enemy of the "good." A 6% rate is historically average, even if it feels high compared to the weirdness of 2020. Focus on the house and the long-term equity rather than trying to time a market that even the experts can't quite figure out.

Next Step: Pull your latest credit report and use a mortgage calculator to see exactly how a 6.11% rate fits into your current monthly take-home pay.