Honestly, trying to keep up with the Indian tax system feels a bit like trying to solve a Rubik’s cube while riding a roller coaster. Just when you think you've finally understood the rules, the Union Budget rolls around and shifts the goalposts. For the financial year 2025-26, the changes to the new tax regime slabs aren't just minor tweaks; they’re a complete overhaul designed to make you forget the old regime even exists.

If you're sitting there wondering why your take-home pay looks different or if you should finally ditch those 80C insurance policies, you're not alone. Most people focus on the percentages. 5%. 10%. 15%. But the real magic—or the real headache—is in how these brackets stack up and the massive rebate that effectively wipes out tax for a huge chunk of the population.

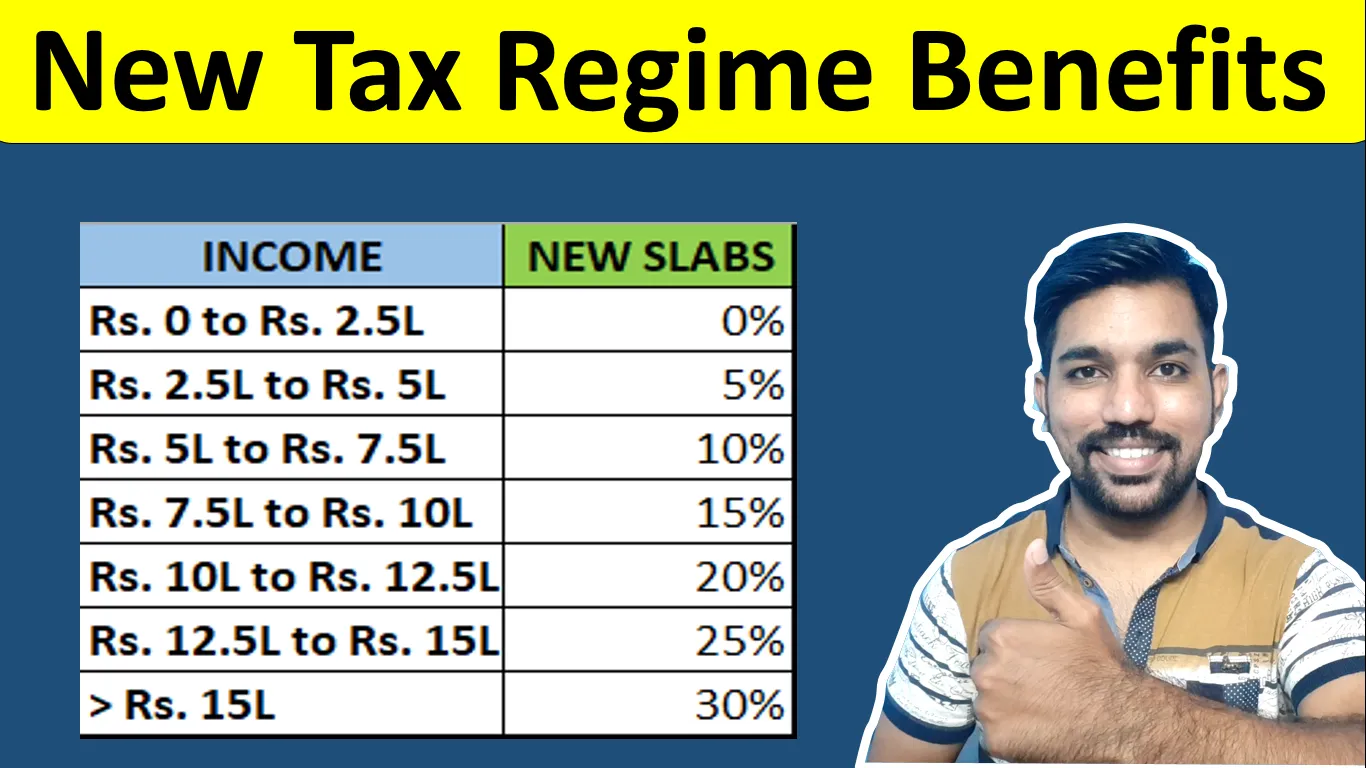

The 2025-26 Reality Check

Basically, the government is pushing everyone toward the new regime by making it the "default" and then sweetening the deal so much that for many, it's a no-brainer.

The biggest shocker? You can now earn up to ₹12 lakh a year and pay zero tax. No, that’s not a typo. Thanks to the updated Section 87A rebate, if your taxable income stays within that ₹12 lakh limit, the government basically hands you a "get out of tax free" card. For salaried folks, it gets even better because the standard deduction has been maintained at ₹75,000. This means you could be pulling in ₹12.75 lakh and still not owe a single rupee to the taxman.

Here is how the actual new tax regime slabs break down for FY 2025-26:

Income from zero to ₹4 lakh is now completely exempt. If you earn between ₹4 lakh and ₹8 lakh, you're looking at a 5% rate. The next jump is from ₹8 lakh to ₹12 lakh, which carries a 10% tax. Once you cross into the ₹12 lakh to ₹16 lakh territory, the rate hits 15%. From ₹16 lakh to ₹20 lakh, it's 20%. The ₹20 lakh to ₹24 lakh bracket is 25%, and anything above ₹24 lakh is taxed at a flat 30%.

It’s a much smoother "staircase" than it used to be. Previously, that 30% rate kicked in much earlier, often making high earners feel like they were being penalized for succeeding.

Why Your "Taxable Income" Isn't Your Salary

People often confuse gross salary with taxable income. Under the new regime, you lose almost all the "fun" deductions like HRA, LTA, and that ₹1.5 lakh 80C limit for LIC and PPF.

But you don't lose everything.

🔗 Read more: Why the 1040 individual tax return Still Confuses Everyone (And How to Fix It)

The ₹75,000 standard deduction is a massive win. Also, the employer’s contribution to your NPS (National Pension System) is still deductible. This is crucial. If your company puts 10% or 14% of your basic salary into NPS, that amount doesn't count toward your taxable total.

Let's look at an illustrative example. Imagine "Rohan," a software engineer in Bangalore. Rohan earns ₹13.5 lakh a year. Under the old rules, he’d be scrambling to find rent receipts and buying insurance he doesn't need just to lower his tax. Now, he takes the ₹75,000 standard deduction, bringing him down to ₹12.75 lakh. If his employer contributes to his NPS, he might dip below that ₹12 lakh threshold. Suddenly, Rohan, who makes over a lakh a month, pays ₹0 tax.

It’s a massive shift in how we think about "middle class" wealth.

The Section 87A Trap

Wait, there’s a catch. There’s always a catch.

The ₹12 lakh "zero tax" rule is a rebate, not an exemption. This is a subtle but vital distinction. If your income is ₹12,00,000, your tax is calculated, and then a rebate of up to ₹60,000 is applied to make it zero.

💡 You might also like: Why 1 US Dollar to 1 Pound Still Matters for Your Wallet

However, if your income is ₹12,00,001—just one rupee over—you lose the entire rebate.

Suddenly, you aren't paying zero. You’re paying the full tax on those slabs, which would be around ₹60,000 plus cess. That is a "cliff" that can catch you off guard. The government does offer "marginal relief" to ensure that the tax you pay isn't more than the extra income you earned, but it's still a sharp jump.

Comparing the Old vs. New

Is the old regime dead? Not quite, but it's definitely on life support.

The old regime slabs haven't changed in ages. You still get the ₹2.5 lakh exemption limit (or ₹3 lakh for seniors). If you have a massive home loan where you're paying ₹2 lakh+ in interest, or if you're heavily invested in tax-saving instruments, the old regime might still occasionally win.

But for the vast majority of people, the new tax regime slabs are designed to be simpler and cheaper. You don't have to save receipts. You don't have to lie to your HR about your house rent. You just get your salary, the slabs are applied, and you’re done.

Actionable Steps for Your Money

Stop blindly investing in ELSS or insurance policies just for tax. In the new regime, those don't help you. If you’re under the ₹12.75 lakh mark (salary), your goal should be to stay there.

📖 Related: NAPA Auto Parts - PM Auto Parts: Why This Local Partnership Actually Works

Check your employer's NPS contribution. If they aren't contributing, ask if they can restructure your CTC to include it. It’s one of the few ways to lower your taxable income in the new system.

Lastly, use an online calculator before the financial year ends. Don't wait until March. If you find you're just slightly over a bracket or the rebate limit, a small contribution to the NPS (Tier 1) can sometimes pull you back into a lower tax liability.

The era of complex tax planning is fading. Now, it's about understanding where you sit on that staircase and making sure you don't accidentally trip over the ₹12 lakh cliff.