Tax season in the Garden State is usually a headache. Most people just want to get through their paperwork without owing the state a small fortune, but that's harder than it sounds. If you’ve ever looked at your paycheck and wondered why your take-home pay feels light—or worse, why you ended up with a massive bill in April—the culprit is almost certainly the NJ-W4.

It’s the Employee’s Withholding Allowance Certificate. Basically, it’s the legal document that tells your employer exactly how much New Jersey Gross Income Tax to skim off the top of your earnings before that money ever hits your bank account.

Most folks treat it like a "set it and forget it" chore. You fill it out on your first day of a new job, sandwiched between HR videos and signing up for health insurance, and then you never look at it again. That’s a mistake. New Jersey has a progressive tax system, and if your withholding doesn’t match your reality, you’re either giving the state an interest-free loan or setting yourself up for a nasty shock when you file your NJ-1040.

Why the NJ-W4 is Actually Different From the Federal Form

A few years back, the IRS completely overhauled the federal W-4. They got rid of "allowances" and moved to a system based on dollar amounts and credits. It was supposed to be simpler, but it mostly just confused everyone who had spent twenty years claiming "1" or "0."

New Jersey didn't follow suit.

The NJ-W4 still relies on the old-school allowance system. This creates a massive disconnect. You can’t just copy your federal info over to the state form and call it a day. If you do, you’re probably going to under-withhold. New Jersey wants you to calculate your allowances based specifically on their state-level exemptions, which are totally separate from what Uncle Sam cares about.

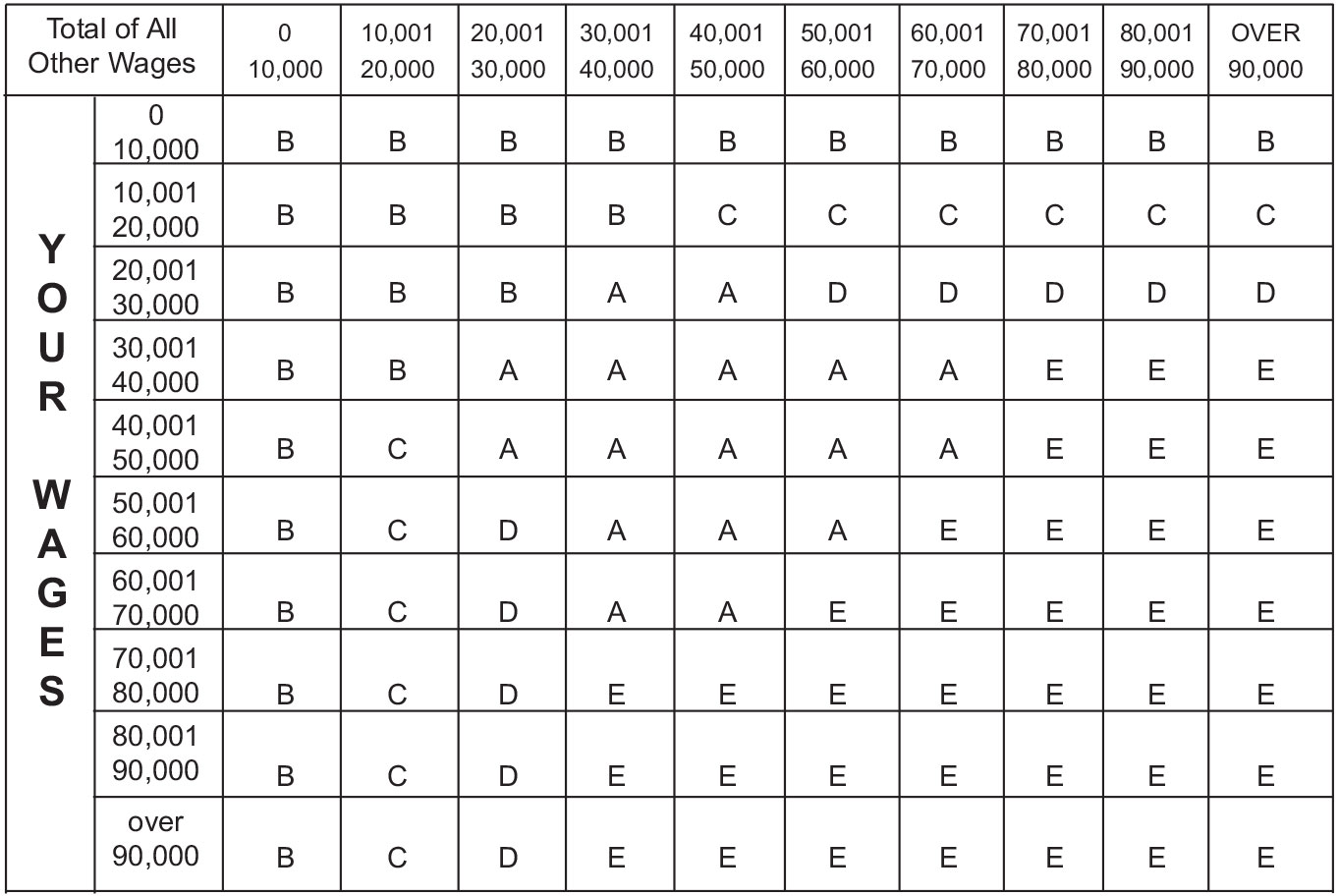

The Mystery of the Rate Tables

New Jersey uses different "Rate Tables" to determine your withholding. This is where most people get tripped up. On the form, you’ll see instructions asking you to choose between Rate Table A, B, C, D, or E.

💡 You might also like: Why Vanguard Inst Total Bond Market Index Trust is the Boring Foundation Your Portfolio Probably Needs

Honestly, it’s a bit of a mess if you don’t know your filing status.

If you’re single or married filing separately, you’re usually looking at Table A. But if you’re a head of household or married filing jointly, things shift. New Jersey has a quirky way of taxing income where the rates can jump significantly once you cross certain thresholds—like $50,000 or $150,000. If your employer is using the wrong table because you checked the wrong box on your NJ-W4, you might be paying a 3% rate when you should be paying 5.5%.

Think about that over the course of a year. That’s thousands of dollars in "oops."

The "Two Earner" Trap in New Jersey

New Jersey is expensive. Most households need two incomes just to keep the lights on and pay the property taxes. But the NJ-W4 is notoriously bad at handling multi-income households automatically.

🔗 Read more: How to Use syncbank com amazon pay bill Without Losing Your Mind

When both spouses work, each employer assumes they are the only source of income for that household. They apply the lower tax brackets to both people. By the time you combine those incomes on your year-end tax return, you’ve likely been bumped into a much higher tax bracket, but neither employer knew to take out the extra cash.

You end up owing. Big time.

The fix is the "NJ-W4 Worksheet." It’s a boring, two-page addition to the form that nobody wants to fill out. But if you have two jobs or a working spouse, you have to use it. You’ll likely find that you need to check the "Instruction 2" box or manually enter an "Additional Amount" to be withheld each pay period. Even $50 extra a paycheck can save you from a $1,200 bill in April.

Dealing With the 2026 Reality

Tax laws aren't static. In 2026, we are seeing the continued impact of cost-of-living adjustments and changes in how remote work is handled. If you live in Jersey but work for a company in Philly or New York, your NJ-W4 situation gets even weirder because of credits for taxes paid to other jurisdictions.

However, for those working strictly within the four corners of New Jersey, the biggest risk right now is the "bracket creep" caused by side hustles. If you have a 1099 gig on the side, your primary employer has no idea. You should use your NJ-W4 at your "real" job to over-withhold slightly to cover the taxes on your freelance work. It’s way easier than remembering to send quarterly estimated payments to Trenton.

How to Fill It Out Without Losing Your Mind

First, grab your last two paystubs. Look at the "NJ State Tax" line. If that number is less than 3% of your gross pay and you make over $50k, you might have a problem.

- Boxes 1 through 3: Basic identity stuff. Don't mess up your Social Security number; the NJ Division of Taxation is not known for its patience with typos.

- Box 4: Filing Status. This must match how you plan to file your year-end return. If you're "Head of Household" (unmarried but supporting kids/parents), make sure you check that. It’s a more favorable rate than "Single."

- Box 5: Total Allowances. Most people put 1 or 0. If you have kids, you can go higher, which means less tax is taken out now. But be careful. New Jersey's child tax credits and exemptions are specific.

- Box 6: Additional Amount. This is the "Safety Valve." If you owed money last year, divide that total by the number of paychecks you have left in the year. Put that number here.

Common Mistakes That Cost You

People often forget to update their NJ-W4 after life happens. Got married? Change it. Had a kid? Change it. Bought a house? Well, property taxes in NJ are a deduction on your state return, so you might actually be able to withhold less tax because your taxable income will be lower.

✨ Don't miss: Converting 175 Pounds to Dollars: Why the Rate You See Isn't Always the Rate You Get

Another huge error is the "Exempt" status. Box 7 allows you to claim you are exempt from NJ withholding. Do not touch this unless you are 100% sure you will earn less than the filing threshold (which is $10,000 for single filers or $20,000 for married couples). If you claim exempt and you actually owe money, the state can slap you with underpayment penalties that make the original tax bill look small.

Actionable Steps for Your Paycheck

Don't wait until January to realize you've been underpaying. You can submit a new form to your payroll department at any time. They might roll their eyes, but it's your money.

- Run a mid-year check: Look at your total NJ withholding year-to-date. Compare it to what you paid last year. If you got a raise but your withholding stayed the same, you’re likely behind.

- Use the official worksheet: The New Jersey Division of Taxation provides a PDF version of the NJ-W4 with a worksheet. Use it. Don't guess.

- Account for the "Exit Tax" or moving: If you're planning to leave the state, your final year of withholding is critical to ensure you don't have lingering liabilities in a state you no longer live in.

- Adjust for bonuses: If you get a big year-end bonus, employers often tax it at a flat rate. Check if that rate actually covers your true NJ tax bracket.

Ultimately, the NJ-W4 is a tool for cash flow management. If you like big refunds, increase your "Additional Amount" in Box 6. If you’d rather have every cent in your paycheck now and you’re disciplined enough to save for a potential bill, keep your allowances high. Just don't let the state decide for you by leaving the form blank or outdated. Update your paperwork, keep a copy for your records, and breathe a little easier knowing you won't be blindsided when tax season rolls around.