You’ve probably heard the rumors or seen the campaign headlines: "No tax on Social Security." It sounds like a dream for anyone living on a fixed income. Honestly, who wouldn't want to keep every cent of that check they spent forty years working for? But as we roll into 2026, the reality of no tax on ss benefits is a bit of a mixed bag. It’s not just one big "yes" or "no." It depends entirely on where you live, how much you've saved in your 401(k), and whether a specific piece of legislation actually crossed the finish line.

The truth? For millions of seniors, a significant tax break just kicked in. For others, the IRS is still knocking.

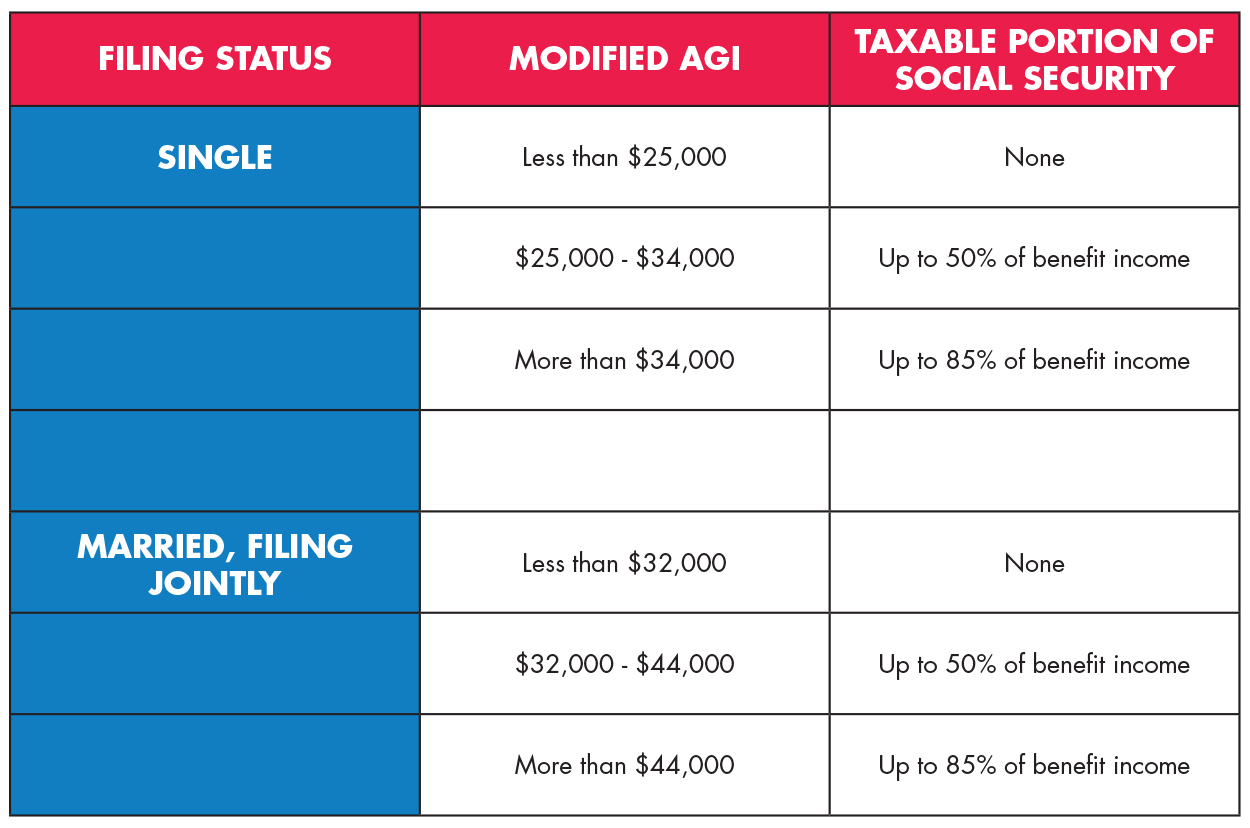

The Federal Reality Check

Let’s get the heavy lifting out of the way first. At the federal level, the rules usually revolve around something called "combined income." This is basically your adjusted gross income plus any nontaxable interest, and then you add in half of your Social Security benefits. If that total is over $25,000 for a single person or $32,000 for a couple, the IRS takes a cut.

That hasn't fundamentally changed for everyone yet.

📖 Related: Musgrove Mortuary Eugene OR: What Really Happens Behind the Scenes

However, there is a massive new wrinkle for 2026. Under the "One Big Beautiful Bill" Act passed recently, a brand-new senior bonus deduction has entered the chat. If you are 65 or older, you can now deduct up to $6,000 (or $12,000 for a married couple) from your taxable income. For many people, this effectively creates a "no tax" zone by pushing their taxable income so low that the IRS can't touch their benefits.

But wait.

If you’re a high-earner—say you’ve got a massive pension or a lucrative consulting gig on the side—you’re still likely paying federal tax on up to 85% of those benefits. It’s a sliding scale. It’s messy. It’s definitely not a blanket "free pass" for everyone in every bracket.

The States Are Abandoning the Tax

While the federal government is moving slowly, the states are practically sprinting away from taxing Social Security.

West Virginia is the big news this year. They finally finished their phase-out. As of January 1, 2026, West Virginia officially offers no tax on ss benefits for all residents, regardless of income. They joined the club that’s been growing fast lately, following in the footsteps of Missouri, Nebraska, and Kansas.

Currently, only a handful of "holdout" states still put a hand in your Social Security pocket:

- Colorado (though they're super generous to those over 65)

- Connecticut

- Minnesota

- Montana

- New Mexico

- Rhode Island

- Utah

- Vermont

If you live in one of the other 42 states or D.C., you're already in the clear at the state level. Florida and Texas get all the credit for being "tax-friendly," but even "high-tax" states like California and New York actually don't tax your Social Security checks. It's one of those weird quirks of state law that surprises people.

Why Does This Matter Right Now?

Inflation. That’s the short answer. The 2026 Cost-of-Living Adjustment (COLA) came in at 2.8%. That’s an extra $56 a month for the average retiree. It sounds nice, but here’s the kicker: more money from Social Security can actually push you over those federal income thresholds.

It's called "bracket creep."

💡 You might also like: Finding an Amazon US Prime Warehouse Map: Why It’s Harder Than You Think

You get a raise from the government, and then the government takes it back because your "combined income" hit $25,001. That is why the new $6,000 senior deduction is such a big deal this year. It acts as a buffer. It keeps that COLA increase in your pocket instead of the Treasury’s.

How to Actually Get to Zero Tax

If you’re looking at your 2026 projections and realizing you’re right on the edge of paying taxes, you have options. It’s not just about waiting for Congress to pass the "You Earned It, You Keep It Act"—which, by the way, is still sitting in a pile of papers in D.C. as of this month.

You can take control of the math.

One move people are loving lately is the Qualified Charitable Distribution (QCD). If you’re over 70½, you can send money directly from your IRA to a charity. That money never shows up as income on your tax return. Since it’s not income, it doesn't count toward the "combined income" formula that triggers the tax on your Social Security.

Another trick? Roth conversions.

If you can move money into a Roth IRA before you start taking Social Security, those future withdrawals are tax-free. They don't count toward the threshold. It’s basically a way to "hide" your wealth from the Social Security tax formula.

Actionable Steps for Your 2026 Return

Don't wait until next April to figure this out. The rules changed significantly this year, and you need to pivot.

- Check your state status. If you live in West Virginia, celebrate—the tax is gone. If you're in Utah or Vermont, look at the specific income caps, because they are more restrictive.

- Calculate your "Combined Income" today. Take your expected AGI, add your municipal bond interest, and add half of your projected Social Security for the year. If you're near $25,000 (single) or $32,000 (joint), you're in the "taxable" zone.

- Apply the Senior Bonus Deduction. Subtract $6,000 per person from your total income if you're over 65. Does that pull you below the taxable threshold? If so, you’ve achieved no tax on ss benefits for the year.

- Adjust your withholdings. If you realize you will owe money, don't let the IRS surprise you. You can ask the Social Security Administration to withhold 7%, 10%, 12%, or 22% of your check now so you don't have a giant bill later.

Tax laws in 2026 are more favorable for retirees than they've been in decades, but they aren't automatic. You have to know which deductions to claim and which state rules apply to your specific zip code.