Wall Street is currently holding its breath. Just a few months ago, Nvidia felt untouchable, a literal money-printing machine that seemed to defy the laws of gravity as it cruised past a $5 trillion market valuation. But lately, things have gotten a bit messy. If you've looked at the tickers recently, you've seen it—a massive Nvidia market cap drop that has wiped out nearly $460 billion in value since its October 29 record.

Honestly, it's enough to make any retail investor sweat.

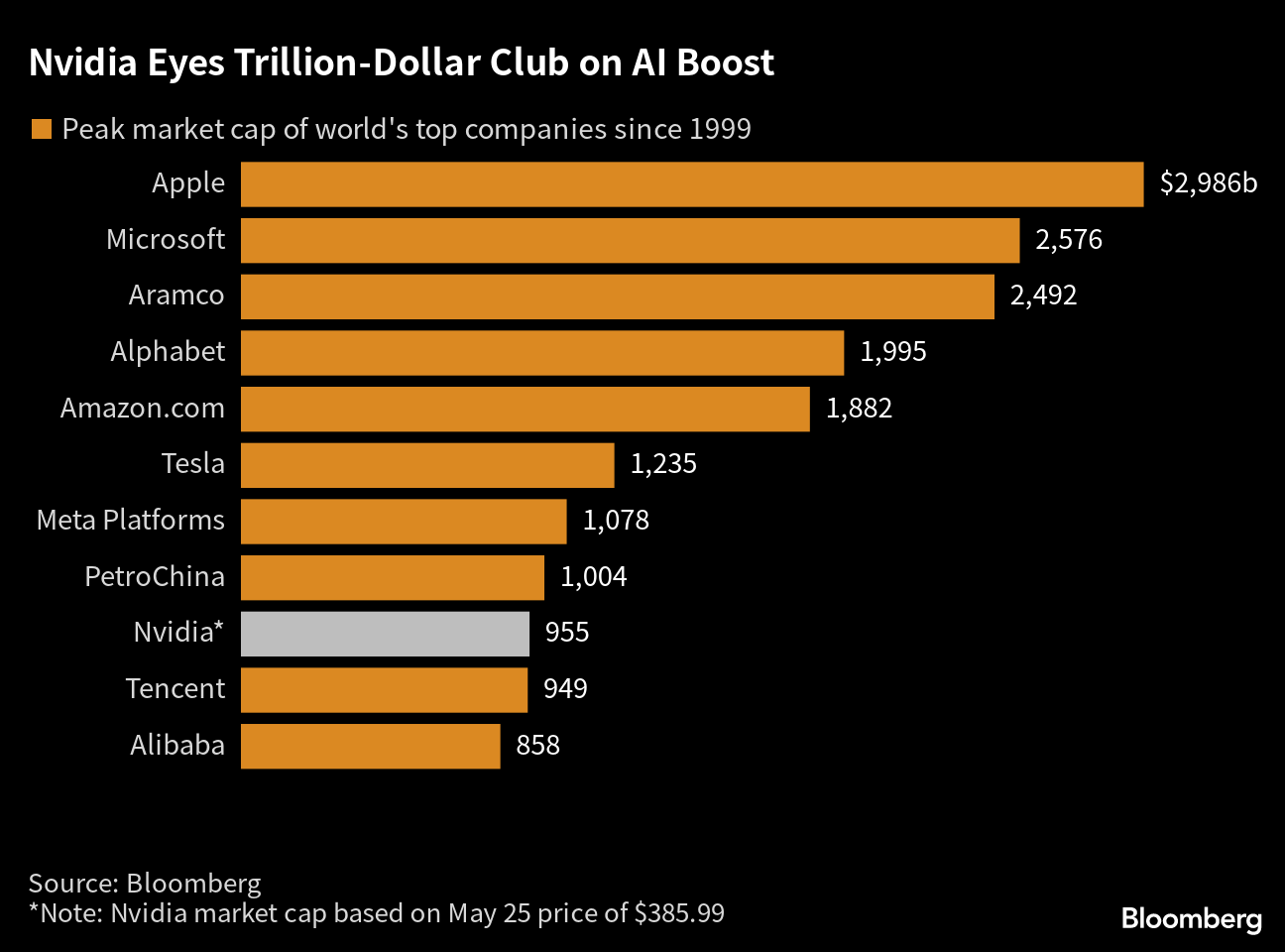

💡 You might also like: City of Los Angeles Employee Salaries Explained (Simply)

We aren't just talking about a little "dip" here. We’re talking about a slide that has seen the stock underperform the S&P 500 for the first time in what feels like forever. While the AI giant is still up more than 1,200% over the last three years, this recent 9.1% slump has people asking a scary question: Is the AI bubble finally popping, or is this just a massive corporation hitting a very expensive wall?

The January 14 "Risk-Off" Slump

Yesterday, January 14, 2026, was a particularly rough day for Jensen Huang’s empire. Nvidia led a broader tech sell-off, with shares sliding 1.44% to close at $183.14. That might sound like a small percentage, but when your market cap is north of $4.5 trillion, 1% is a staggering amount of money to vanish in a single afternoon.

Basically, investors are getting spooked by a mix of high-level drama. We’ve got uncertainty over Federal Reserve independence, a Department of Justice investigation into White House renovation budget overruns (yes, really), and a general "risk-off" sentiment where people are pulling money out of high-growth tech and hiding it in gold and silver.

But the real reason for the Nvidia market cap drop goes way deeper than a bad day on the Nasdaq. It’s about the "Monetized Competition" era we just entered.

The 25% Chip Tax and the China Headache

On January 13, 2026, the U.S. Department of Commerce flipped the script. They decided to allow Nvidia to sell its high-end H200 chips to China again, which should be good news, right?

Well, not exactly.

It comes with a massive catch: a 25% "chip tax" on advanced AI processors transshipped to restricted regions. The government wants its cut. While this reopens a massive market, it also introduces a heavy fiscal burden and a 50% domestic volume cap. Investors are currently trying to figure out if Nvidia can pass that 25% cost onto Chinese buyers or if they’ll have to eat the loss themselves.

Why the market is nervous:

- The H20 Charge: Last year, Nvidia had to eat a $4.5 billion inventory charge because demand for their "gimped" China-specific H20 chips cratered once export rules changed.

- DeepSeek's Shadow: Back in early 2025, a Chinese AI model called DeepSeek claimed it could run with way fewer processors. That alone caused a 20% flash crash because it threatened the "more is better" GPU mantra.

- The 25% Surcharge: This new executive order essentially makes the U.S. government a silent partner in every high-end sale to China, muddying the profit margins that analysts have worshipped for years.

Is Competition Finally Catching Up?

For years, Nvidia’s moat was more like an ocean. But in 2026, the water is looking a bit shallower. It’s not just AMD anymore. Alphabet and Amazon are dumping billions into their own custom AI chips (ASICs) to avoid paying the "Nvidia tax."

Broadcom is also becoming a massive thorn in Nvidia's side. They just landed a $21 billion order for TPUs from Alphabet. When your biggest customers start building their own tools, the "infinite demand" story starts to show some cracks.

The Blackwell Ramp and the "Staggering" Demand

Despite the Nvidia market cap drop, the actual business is still a beast. In the most recent Q3 2026 results, revenue hit $57 billion. That’s up 62% from a year ago. Jensen Huang recently noted that Blackwell—their latest architecture—is "off the charts."

The company is basically in a race against its own supply chain. They’ve partnered with everyone from OpenAI (a 10-gigawatt infrastructure deal) to the U.S. Department of Energy. They aren't struggling to find buyers; they’re struggling to build enough chips to satisfy the world's hunger for "Agentic AI" and robotics.

Putting the Drop into Perspective

It’s easy to panic when you see $400 billion evaporate. But let’s look at the numbers. Even with this slump, 76 out of 82 Wall Street analysts still say "Buy." The average price target is still sitting around a level that would value the company at over $6 trillion.

✨ Don't miss: Kroger Corporate Office Cincinnati Ohio: What Most People Get Wrong

Most experts see this as a "revaluation" rather than a collapse. The P/E ratio is sitting around 37x to 40x forward earnings. High? Sure. But compared to the 55x historical average, you could actually argue Nvidia is "cheaper" now than it was during the 2024 frenzy.

Key Factors to Watch in 2026:

- The Rubin Launch: The upcoming Rubin platform is promised to be 5x faster than Blackwell. If they nail this, the competition might be left in the dust again.

- TSMC’s CapEx: Nvidia’s supplier, TSMC, just announced they’re spending up to $56 billion this year on production. They wouldn't do that if Nvidia wasn't ordering every chip they can make.

- The "Chip Tax" Impact: Keep a close eye on the next earnings call. If margins stay in the 73-75% range despite the 25% China surcharge, the stock will likely rocket back up.

Actionable Insights for Investors

If you're holding NVDA or thinking about jumping in after this Nvidia market cap drop, don't play the day-to-day volatility game. The "ChatGPT moment for robotics" is the new narrative Jensen is pushing, and the shift toward Physical AI is where the next trillion dollars will likely come from.

Watch the $180 support level. If it holds, the "Monetized Competition" era might just be a brief transition period. Focus on Data Center revenue growth—as long as that stays above 50% YoY, the engine is still humming. The "AI bubble" talk has been around since 2023, yet here we are, talking about a $4.5 trillion company like it’s a struggling startup. Context matters.

Keep an eye on the 10-K filings for any updates on the DOJ investigations or further shifts in trade policy, as those "black swan" regulatory events are now the biggest threat to the market cap—more so than the competition.