If you’ve been watching the pennar industries stock price lately, you’ve probably noticed the mood has turned a bit sour. As of mid-January 2026, the stock has been sliding, hitting around ₹183.31. That’s a far cry from the highs of nearly ₹280 we saw just a few months back in November 2025. Honestly, it’s enough to make any retail investor sweat. But if you only look at the red on the screen, you’re missing the actual mechanics of what this company is doing behind the scenes.

Pennar isn't just a "steel company" anymore, even though that's how most people categorize it. They’ve morphed into a diversified engineering beast. We are talking about everything from hydraulic cylinders and aerospace components to those massive pre-engineered buildings (PEBs) you see in industrial parks. The disconnect between the business performance and the current stock price is where the real story lives.

The Reality Behind the Recent Slide

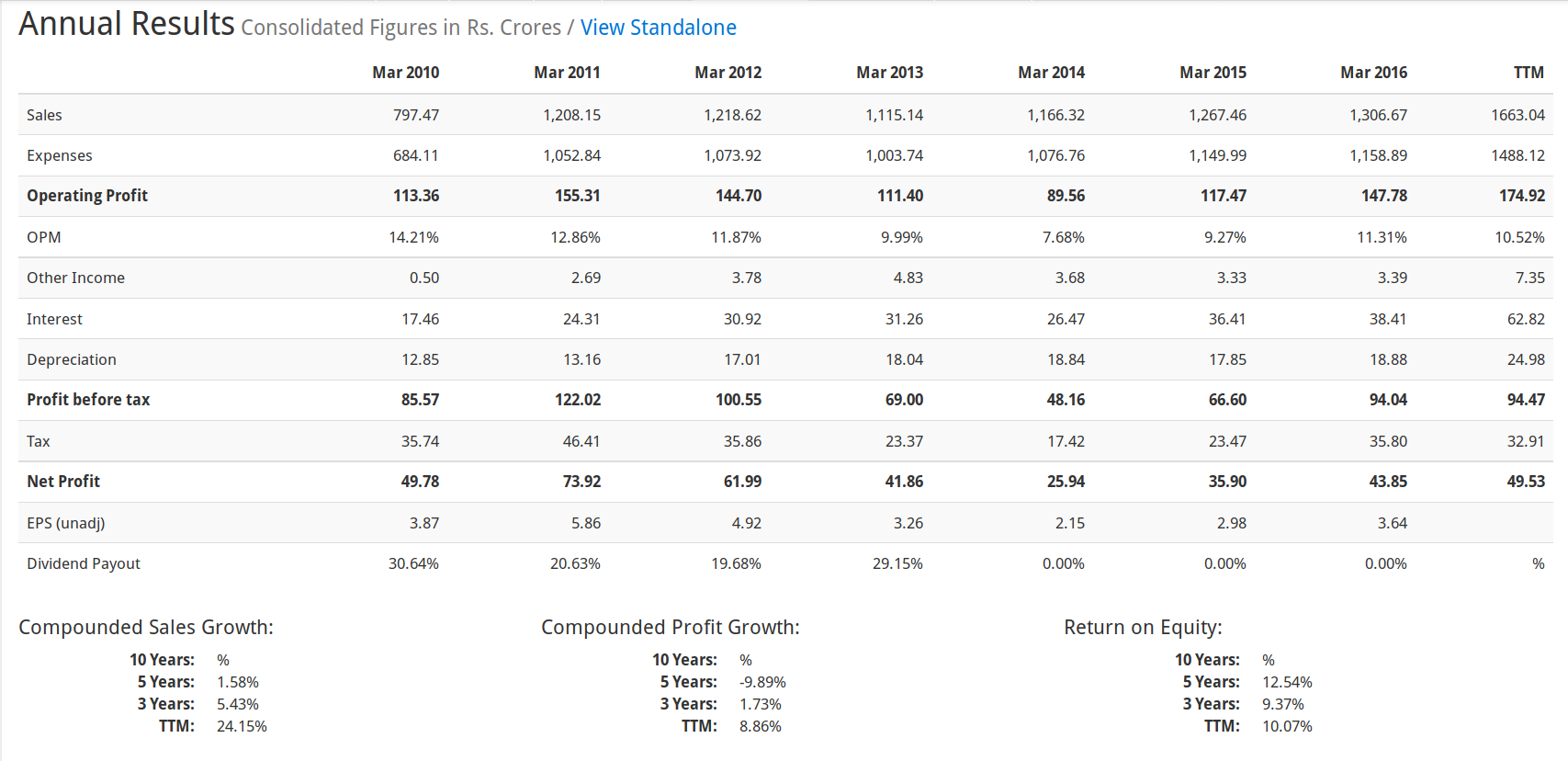

The market can be a fickle beast. In the last week alone, the stock dropped roughly 9%. Why? It’s not because the company is failing. In fact, their Q2 FY26 results were actually quite strong. Revenue jumped 22% year-over-year to ₹919.60 crores. Profit after tax (PAT) rose by 20%.

✨ Don't miss: Why the Call Center for Pizza Hut Still Exists in a Mobile App World

So, if the numbers are up, why is the price down?

Basically, it’s a mix of "priced in" expectations and some temporary margin pressure. Investors got really excited leading up to November, pushing the stock to that ₹280 peak. When the results came out, they were good, but maybe not "explosive" enough to justify the vertical climb. People started pocketing profits.

Then you’ve got the margins. PAT margins dipped slightly to 3.56%. Management blamed this on one-time costs from their $14 million acquisition of Telco Enterprises’ structural assets in the US and some temporary labor supply issues. The market hates "temporary issues" until they are officially over.

Why the Pennar Industries Stock Price Still Matters

To understand where the stock might go, you have to look at their order book. It’s sitting at nearly ₹956 crores. That’s a lot of work already lined up.

💡 You might also like: 401k performance by president: What Most People Get Wrong

The US Factor

One thing most people ignore is their US subsidiary, Ascent. While Indian markets are volatile, the US business is seeing double-digit growth. Their order backlog in the States expanded to about $51 million recently. The Telco acquisition is expected to add another ₹100 crores annually to the top line starting from Q3 FY26.

The Raebareli Boost

Back home, their new PEB plant in Raebareli is finally fully functional. In the engineering world, "functional" means the heavy lifting is done and the cash should start flowing. Management expects capacity utilization to jump from 65% to over 75% very soon. Higher utilization usually leads to better margins because you’re spreading fixed costs over more products.

Technicals vs. Fundamentals

If you talk to a chartist, they’ll tell you the pennar industries stock price is in a "weak" trend. The stock is trading below its 50-day and 200-day moving averages (which are currently around ₹209 and ₹216 respectively). Technically, it’s in a bit of a no-man's-land.

But look at the valuation. The price-to-earnings (P/E) ratio is hovering around 18-20x. Compare that to some of their peers or the broader industrial sector, and it starts looking a lot more reasonable than it did at ₹280. Their Return on Capital Employed (ROCE) is still a healthy 13.7% to 21% depending on the quarter you analyze. That’s a sign of a company that knows how to use its money.

Peer Comparison at a Glance

- Tata Steel: Massive, but legacy-heavy.

- Jindal Stainless: Strong, but highly sensitive to raw material price swings.

- Pennar: Smaller (Small-cap), more agile, and shifting toward high-margin "Body in White" (automotive) and engineering services.

What Most People Get Wrong

The biggest misconception is that Pennar is a commodity play. It’s not. If steel prices drop, Pennar actually benefits in many of its segments because steel is an input for them. They are a value-add engineering firm. They take the raw material and turn it into something complex—like a specialized hydraulic part for a European tractor or a structural component for a Hyundai car.

They’ve also been quietly cutting debt. The debt-to-equity ratio is around 0.8. While that’s not "debt-free," it’s a whole lot better than the bloated balance sheets many engineering firms carried five years ago.

Actionable Insights for Investors

If you’re holding or looking at Pennar, here is the ground truth:

📖 Related: Why Emerald Coast Utilities Authority Is Actually Changing How You Think About Trash

- Watch the ₹175–₹180 level: This has historically acted as a bit of a floor. If it breaks significantly below this, the technical "pain" might last longer.

- Monitor the Telco Integration: The Q3 FY26 results (expected soon) will show if the US acquisition is actually contributing to the bottom line or just adding revenue.

- Keep an eye on the Auto Sector: Since they supply to big names like Ashok Leyland and Stellantis, their "Diversified Engineering" segment lives and dies by how many trucks and cars are being built.

- Ignore the Daily Noise: Small-cap stocks like this can swing 5% on no news. Focus on the quarterly EBITDA margins. If they can push those back above 10.5% consistently, the stock price will eventually follow.

The current dip in the pennar industries stock price reflects a market that is re-calibrating after a massive run-up. The fundamentals—order books, US expansion, and capacity utilization—suggest the "engine" is still running fine, even if the "paint job" looks a bit scratched right now.

To stay ahead, track the upcoming Q3 earnings specifically for the "Custom Designed Building Solutions" revenue growth. If that segment continues to grow at 30%+, the current bearishness will likely be a short-lived memory by mid-2026. Review your portfolio's exposure to small-cap cyclicals before making a move, as the volatility in this segment isn't for the faint of heart.