Honestly, trying to peg exactly where the Federal Reserve will be in 2031 feels a bit like trying to predict the weather for a specific Tuesday four years from now. But if you're looking at the data we have right now in early 2026, the tea leaves are starting to form a pretty interesting, if slightly confusing, picture. Most people assume rates always go back to "normal"—meaning those dirt-cheap pandemic lows—but that's basically a fantasy at this point.

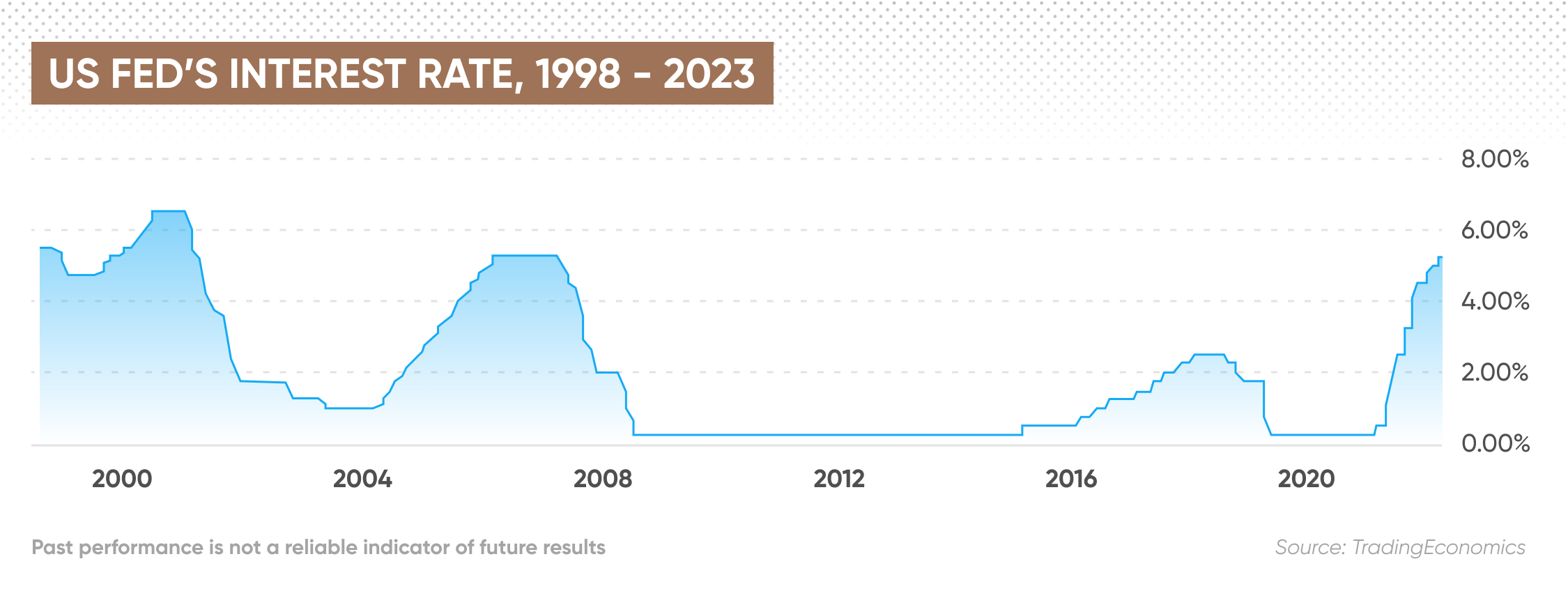

We've just spent the last couple of years watching the Fed play a high-stakes game of chicken with inflation. As of January 2026, the effective federal funds rate is sitting around 3.6%. You've probably noticed your savings account isn't quite as juicy as it was a year ago, but your mortgage quote is still high enough to make you wince.

The Long-Term Drift

The market is currently pricing in a "gentle glide." Basically, the consensus from futures markets (specifically SOFR futures which are the big-money bets on where rates go) suggests we might see a bit of a dip into 2027, maybe hitting a trough around 3.2%. But then something weird happens. Instead of staying low, the curve starts to slope back up.

✨ Don't miss: s and p 500 performance by year: Why Most Investors Get the Numbers Wrong

By the time we hit 2030 and 2031, projections from places like StreetStats and various Fed-watchers show the rate creeping back toward 3.8%.

Why? Because the "neutral rate"—the goldilocks zone where the economy isn't being throttled but isn't over-inflated either—is moving. It's higher than it used to be. Jerome Powell, whose term is winding down, has hinted that the old days of near-zero interest are likely gone for good.

What’s Actually Driving the 2031 Numbers?

There are a few massive gears turning in the background that determine projected interest rates in 5 years. It’s not just about one guy at a podium in D.C.

- The Debt Trap: The U.S. government is carrying a massive amount of debt. While you'd think that would force rates down to keep interest payments cheap, the Congressional Budget Office (CBO) actually points out that high federal borrowing can crowd out private investment and push rates up to attract buyers for all those Treasury bonds.

- Demographics: We’re getting older. An aging population usually means less labor and slower growth, which typically pushes rates down. The European Central Bank has actually estimated that this "greying" effect could depress real rates by another 0.25% to 0.5% by 2030.

- The Tariff Wildcard: This is the big one for 2026. If trade wars heat up and average tariff rates stick around 15%, as some Deloitte analyses suggest, that’s going to keep inflation "sticky." Sticky inflation means the Fed can’t cut rates as much as they might want to.

Mortgages: The 5.5% Wall

If you're reading this because you're waiting to buy a house, listen up. The days of 3% mortgages were a historical anomaly, sort of a "once in a lifetime" glitch.

Fannie Mae and Redfin are both looking at the end of this decade—the 2030 to 2031 window—and they see a "new normal" for 30-year fixed rates hovering around 5.5% to 6.0%. If you’re holding out for 4%, you might be waiting until you're retired.

👉 See also: Customer Service in McDonald's: Why It Feels So Different Lately

Realistically, if mortgage rates hit 5.5% by 2030, Redfin thinks housing affordability might finally return to those 2018 levels. But that assumes your income keeps growing and home prices don't pull another 2021-style moon mission.

Not Everyone Agrees (The Bear Case)

It’s worth noting that some models, like those from the CBO, are a bit more pessimistic about growth. They see GDP slowing to about 1.8% annually toward 2031. If the economy feels sluggish or if we hit a real recession in 2028 or 2029, the Fed will slash rates to zero again faster than you can say "quantitative easing."

J.P. Morgan’s analysts are currently cautious, suggesting that while we might see cuts in the short term, they expect the Fed to remain on hold for long stretches to avoid letting inflation flare back up. They’ve noted that the labor market is "tightening by the second quarter" of 2026, which usually keeps a floor under how low rates can go.

The Bottom Line for Your Wallet

So, where does that leave you?

Kinda in the middle. We aren't heading back to the "free money" era, but we also aren't stuck in the 8% mortgage nightmare of 2023.

👉 See also: ¿Dónde está mi declaración enmendada? Por qué el IRS tarda tanto y cómo rastrearla hoy

Next Steps for the 5-Year Horizon:

- Locking in yields: If you have cash, the current 2026 rates (mid 3% range for the Fed, 4% for 10-year Treasuries) are likely the best you’ll see for a while before that 2027 dip.

- The Refinance Window: Keep an eye on the late 2026 or early 2027 period. That’s when the "trough" is projected to hit. If you bought in 2024 or 2025, that’s your likely window to swap that high-rate mortgage for something in the 5% range.

- Variable Debt: If you’re carrying credit card debt or a HELOC, don't expect a massive rescue. Even in 5 years, the base rate is likely to be significantly higher than the 0-1% range we saw for most of the 2010s.

Ultimately, the 2031 outlook is about stability. The era of extreme volatility—where rates jump 4% in a year—is hopefully behind us. We’re moving toward a "higher for longer" world that is actually just a "normal for longer" world.