Honestly, walking into a supermarket lately feels like a bit of a gamble. You grab a loaf of bread, some eggs, maybe a bag of pasta, and suddenly you’re staring at a self-checkout screen asking for twenty quid. It’s exhausting. We keep hearing that the rate of inflation UK is "stabilising," but if you’re looking at your bank balance, it probably doesn't feel that way.

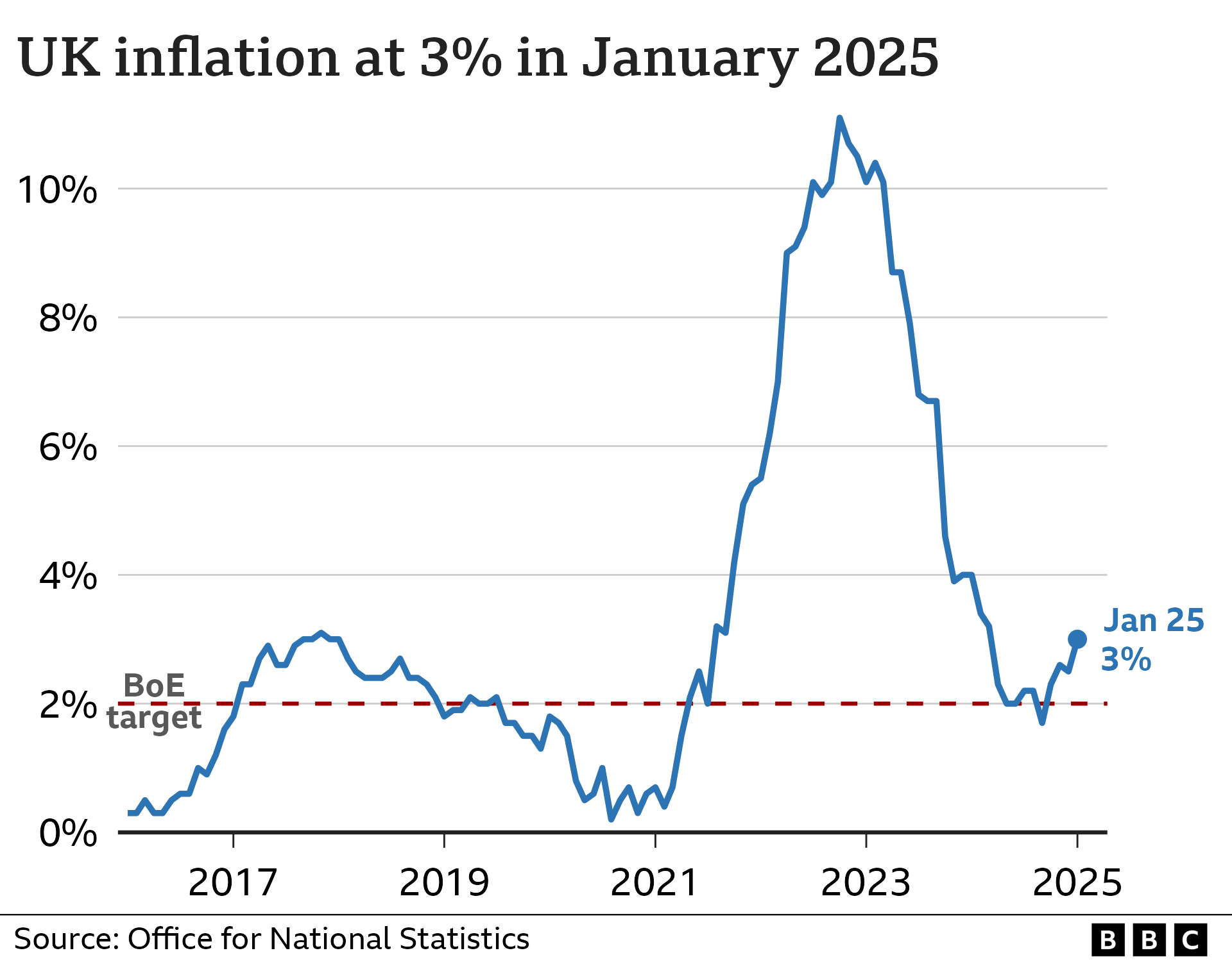

The latest numbers from the Office for National Statistics (ONS) show that headline inflation dipped to 3.2% as we entered 2026. On paper, that sounds great. It's a massive drop from those terrifying double-digit peaks we saw a few years back. But there’s a massive gap between a "falling rate" and "falling prices."

Inflation slowing down just means things are getting expensive slower. It doesn’t mean that £5 block of cheddar is going back to £3.50.

The Reality of the Rate of Inflation UK Right Now

The Bank of England is currently in a bit of a head-scratching phase. They’ve managed to get the headline CPI (Consumer Prices Index) down significantly, but "core" inflation—the stuff that strips out volatile things like energy and food—is being a bit stubborn.

Right now, the Bank of England base rate sits at 3.75%. They cut it just before Christmas in 2025, which gave homeowners a tiny bit of breathing room, but they’re moving cautiously. Why? Because services inflation is still sticky.

When you go to a restaurant or get a haircut, you’re paying for someone’s time. And because wages have had to rise to keep up with the cost of living, businesses are passing those costs directly to you. It's a bit of a loop.

Why the "2% Target" is the Holy Grail

The government tells the Bank of England to keep inflation at 2%. It’s a bit like a thermostat. If it gets too hot (high inflation), they hike interest rates to cool spending. If it gets too cold (deflation), they lower rates to get us spending again.

Economists like James Moberly at Goldman Sachs think we might actually hit that 2% mark by the summer of 2026. But reaching it is one thing; staying there is another.

What’s Actually Driving Your Bills Up?

It’s not just "one thing." It’s a messy cocktail of global politics, weather, and a bit of corporate maneuvering.

- The Grocery Gap: Food inflation is actually higher than the general rate. While the overall rate of inflation UK is around 3.2%, food and non-alcoholic drinks have been hovering closer to 4.2%. We’ve seen bread and cereals finally start to chill out, but "regulatory costs" are now the big bogeyman for retailers.

- Energy Relief (Sort of): The 2025 Autumn Budget introduced some energy bill relief and a rail-fare freeze. This is expected to shave about 0.3 percentage points off the inflation rate this year. It’s helpful, but you won't exactly feel like you’ve won the lottery.

- The "K-Shaped" Recovery: This is a fancy way of saying some people are doing fine while others are struggling. If you own your home outright, you aren't feeling the sting of high mortgage rates. If you’re a first-time buyer or renting, the "inflation" you experience is way higher than the national average.

The Experts' Take: Is the Worst Over?

If you ask the folks at RSM UK, they’ll tell you that 2026 is going to feel "calmer but uncertain." They’re forecasting an average inflation rate of 2.7% for the whole of 2026.

But there’s a catch.

👉 See also: ERG Theory of Motivation: Why People Stop Caring at Work (And How to Fix It)

There’s a persistent worry about the "loose labour market." Basically, unemployment is creeping up—forecast to hit 5.3% by March—which usually cools inflation because people have less money to spend. But at the same time, the National Minimum Wage increases are keeping pay pressure high.

It’s a balancing act that would make a tightrope walker sweat.

What Most People Get Wrong

Many people think that if the rate of inflation UK hits 0%, prices stay the same. In reality, we want a little bit of inflation. If prices were constantly falling (deflation), nobody would buy anything today because it would be cheaper tomorrow. The economy would basically grind to a halt.

The sweet spot is where you barely notice the price changes. We aren't there yet.

How to Protect Your Wallet in 2026

Since we can't control the Bank of England, we have to control our own "personal inflation rate."

Check Your Savings

If the base rate is 3.75%, your savings should be earning at least that. If your bank is still giving you 1%, move your money. You are literally losing purchasing power every single day.

The "Shrinkflation" Watch

Keep an eye on weights, not just prices. Manufacturers are getting really sneaky about keeping the price the same but taking ten grams out of the chocolate bar. It’s inflation by stealth.

Lock in Fixes Where Possible

If you have a mortgage renewal coming up in the next 12 months, talk to a broker now. The markets expect rates to settle around 3.25% by the end of the year, but "global shocks"—a phrase economists love to use for "things we didn't see coming"—could change that in a heartbeat.

Looking Ahead: The Spring Pivot

By April 2026, we should see a significant dip in the headline rate as the new energy price caps and budget measures kick in. Most analysts expect the rate of inflation UK to finally drop below 3% during the spring.

Will it feel like a victory? Probably not immediately. But it means the era of "everything gets 10% more expensive every year" is hopefully in the rearview mirror.

The next big date to watch is February 5th, when the Bank of England meets for its first interest rate decision of the year. If they cut rates again, it's a sign they’re confident that inflation is truly under control. If they hold, it means they’re still worried about those sticky service costs.

Practical Steps You Can Take Now:

- Audit your direct debits: Inflation makes us "subscription blind." If you haven't used that streaming service or gym membership in three months, kill it.

- Shop the "lower" brands: We’ve seen a massive shift toward discount retailers like Aldi and Lidl for a reason. Their internal inflation rates often track lower because they have more control over their supply chains.

- Hedge your bets: If you have extra cash, look into inflation-linked bonds or diversified ISAs. Leaving it in a standard current account is the only guaranteed way to lose value in 2026.

Inflation is a slow-motion beast. It took a long time to get this high, and it’s taking a long time to settle. Stay informed, keep an eye on the ONS monthly releases, and don't let the "official" numbers gaslight you—if things feel expensive, it’s because they are.