Look at a fed interest rate graph from the last forty years and you’ll see something that looks like a heart monitor for a very stressed person. It's jagged. It's steep. Sometimes it’s flat for so long you’d think the economy had actually died. But most people look at these charts and see the wrong thing. They see a "line going up" and think their mortgage is doomed, or they see a "line going down" and assume the stock market is about to moon.

It’s way more complicated. Honestly, it's about the "Neutral Rate."

The Federal Reserve—basically the world’s most powerful bank—uses the federal funds rate as its primary lever to keep the U.S. economy from either exploding into hyper-inflation or freezing over into a depression. When you pull up a fed interest rate graph, you aren't just looking at costs. You're looking at a visual representation of the Fed’s anxiety. If that line is climbing, Jerome Powell and the Board of Governors are worried about "overheating." If it’s crashing toward zero, like it did in 2008 and 2020, they’re in full-blown panic mode, trying to jumpstart a stalled engine.

Why a Fed Interest Rate Graph Looks Like a Mountain Range

If you zoom out to the 1980s, the graph is a literal cliff. Paul Volcker, the Fed Chair at the time, pushed rates to nearly 20% to kill off the stagflation of the 70s. People were burning effigies of him. Builders were mailing him 2x4s to protest the death of the housing market. But he did it. He broke the back of inflation. Ever since then, the long-term trend on any fed interest rate graph has been a steady, decades-long slide downward.

Until 2022.

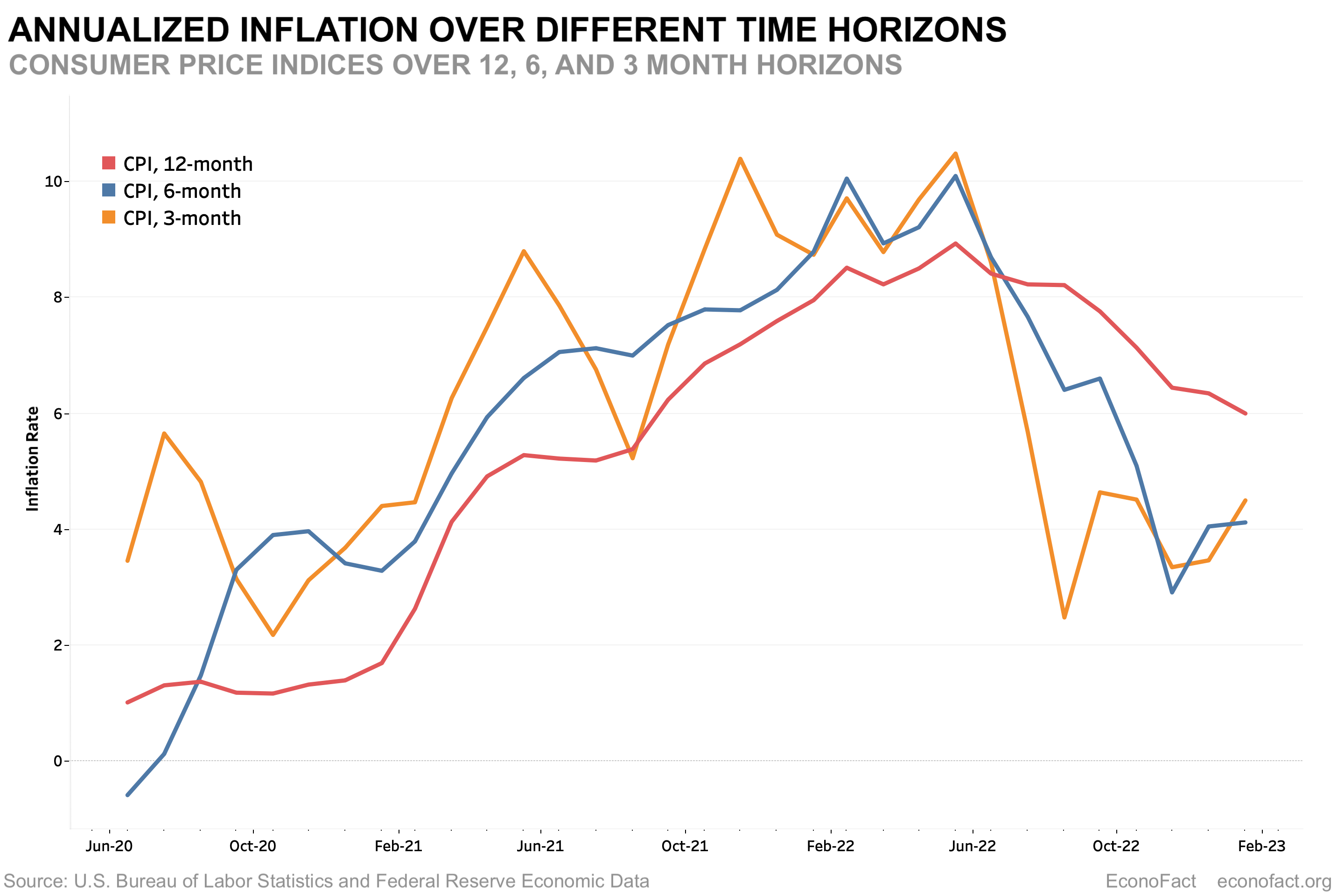

That’s when the "Era of Easy Money" hit a brick wall. We saw the steepest hiking cycle in modern history. You can see it on the chart—a vertical line that looks like the side of an Egyptian pyramid. The Fed moved from 0% to over 5% in what felt like a weekend. It wasn't just about making car loans more expensive; it was a desperate attempt to suck liquidity out of a system that was drowning in COVID-era stimulus and supply chain mess-ups.

The "Lag Effect" is the Real Killer

Here is the thing about these graphs: they don't show you what is happening now. They show you what the Fed thinks happened six months ago. Economists call this "long and variable lags." Think of it like steering a massive container ship. You turn the wheel (change the interest rate), but the ship doesn't actually start moving for another three miles.

By the time the fed interest rate graph shows a peak, the damage to the economy might already be done. This is why "soft landings" are so rare. Usually, the Fed keeps hiking until something breaks—like Silicon Valley Bank in early 2023—and then they have to scramble to pivot.

👉 See also: Billings MT Red Lobster: What Most People Get Wrong About Its Survival

Understanding the "Dot Plot" vs. Historical Reality

When you see news outlets talking about where the fed interest rate graph is going next, they usually reference the "Dot Plot." This isn't an actual record of rates; it’s a forecast where each Fed official puts a literal dot on a chart to show where they think rates should be in a year or two.

It's often wrong. Shockingly wrong, actually.

In 2021, the Dot Plot suggested we wouldn't see rate hikes until 2023. By early 2022, they were hiking aggressively. Why? Because the Fed is "data dependent." They’re staring at the Consumer Price Index (CPI) and employment numbers like a hawk. If the "Summary of Economic Projections" says one thing but the price of eggs doubles, the dots don't matter. The graph will follow the inflation.

You've gotta realize that the Fed has a dual mandate: stable prices and maximum employment.

- They want inflation at 2%. Not 0%, because that leads to deflationary death spirals.

- They want everyone who wants a job to have one.

When these two goals fight, the fed interest rate graph is the casualty. If inflation is 8% but everyone has a job, they’ll hike rates until people start getting fired. It’s cold. It’s math. It’s how the system is designed to "rebalance."

The 10-Year Treasury Connection

A lot of folks get confused here. They think the Fed sets the rate for their 30-year fixed mortgage. They don’t. The Fed sets the overnight lending rate for banks. However, the 10-Year Treasury Yield usually tracks the expectations of the fed interest rate graph. If investors see the Fed's line heading up, they demand higher yields on bonds. Since mortgages are often priced based on that 10-year yield plus a "spread," your housing cost goes up even if the Fed hasn't moved yet.

It's all anticipation. Markets are basically a giant machine that tries to guess what the next inch of the graph will look like.

✨ Don't miss: University of Georgia Tuition Explained (Simply): What You’ll Actually Pay

Common Misconceptions About High Interest Rates

"High" is relative. If you talk to someone who bought a house in 1984, a 7% interest rate sounds like a dream. If you bought a house in 2021 at 2.8%, a 7% rate sounds like a human rights violation.

Historically, the "normal" rate on a fed interest rate graph isn't zero. The 2010s were a weird anomaly. We spent a decade with rates near the "Zero Lower Bound" because we couldn't get enough growth. That created "Zombie Companies"—businesses that only stayed alive because borrowing money was basically free. When the graph spiked in 2022, those zombies started to die off.

That’s actually healthy, even if it feels like a disaster. It’s called "creative destruction."

The Real Impact on Your Wallet

When the line on the fed interest rate graph moves, your life changes in three specific ways:

The Debt Trap: Credit card APRs are tied directly to the prime rate, which is tied to the Fed. If the Fed moves up by 0.25%, your credit card interest likely moves up too. Over a year of hiking, that can turn a manageable balance into a permanent debt cycle.

The Savings Silver Lining: For the first time in forever, High-Yield Savings Accounts (HYSAs) are actually paying out. You can get 4% or 5% just for letting your cash sit there. When the graph is low, you're forced into the stock market to get any return. When the graph is high, "Cash is King" again.

The Wealth Effect: High rates generally put downward pressure on asset prices. If it costs more to borrow money to buy a company or a house, those things become worth less. People feel poorer, so they spend less, which (in theory) lowers inflation.

What to Watch for in the Next 12 Months

Everyone is looking for the "pivot." That’s the point on the fed interest rate graph where the line stops going up or sideways and starts heading down.

But be careful what you wish for.

Historically, the Fed only cuts rates quickly when something is broken. If the graph drops like a stone in 2026, it’s probably because unemployment is skyrocketing or a major sector of the economy has collapsed. A "slow glide" down is what you want—it means the Fed thinks they've won the war on inflation without destroying the labor market.

Watch the "Real Rate." That's the Fed funds rate minus the inflation rate. If the Fed is at 5% and inflation is at 2%, the "Real Rate" is 3%. That is extremely "restrictive." It’s like driving with the parking brake on. If that gap stays too wide for too long, the economy eventually stalls out.

Actionable Steps for Navigating Rate Cycles

Stop trying to time the Fed perfectly; even the Fed can't time the Fed. Instead, look at where the fed interest rate graph is currently sitting and adjust your personal balance sheet accordingly.

- Lock in yields while you can: If the graph is at a local peak, long-term CDs or bonds are a great way to "capture" those high rates before the Fed starts cutting.

- Deleverage high-interest debt: If the line is high, your credit card debt is a fire that's being fed pure oxygen. Put every spare dollar toward the highest APR first.

- Watch the "Inverted Yield Curve": This is when short-term rates on the graph are higher than long-term rates. It’s been the most reliable recession indicator for fifty years. If you see the 2-year yield higher than the 10-year yield, tighten your belt. A storm is usually coming within 12 to 18 months.

- Refinance strategy: If you're stuck with a high-rate loan from the recent peak, don't panic. You don't need the Fed to go back to 0% to benefit. Even a move from 7% to 5.5% on a mortgage can save you hundreds of thousands over the life of the loan.

The fed interest rate graph is essentially the heartbeat of global capitalism. It dictates how much you pay to live, how much you earn on your savings, and whether your employer can afford to keep you on the payroll. Respect the line, but don't fear it. Understanding that the Fed is always reacting to old data allows you to stay one step ahead of the "crowd" that only reacts when the news hits the front page.