Stock markets are weird. One day you're looking at a company that seems to be doing everything right—bagging massive infrastructure contracts, diversifying into green energy, and keeping debt low—yet the ticker symbol on your screen is flashing red. That is basically the story of the Refex Industries Ltd share price lately.

Honestly, it’s been a bit of a rollercoaster. If you’ve been tracking this stock, you’ve probably noticed the sharp contrast between its operational wins and its market performance. On January 16, 2026, the stock closed at ₹239.10 on the NSE. To put that in perspective, that’s a far cry from its 52-week high of ₹534. It’s a classic case of "the business is growing, but the stock is catching its breath."

The Reality Behind the Recent Slide

Why has the price been sliding? Markets hate uncertainty. Recently, news broke about the Income Tax Department conducting search operations at Refex's registered offices. Even though the company was quick to clarify that operations weren't affected and they were cooperating fully, investors often sell first and ask questions later. This "search" news wiped out a chunk of market cap in a single session.

But let’s look at the numbers. They tell a different tale.

In Q2 of FY2025-26, the company reported a net profit of ₹52 crores, which was actually a sequential jump. Their EBITDA nearly doubled to ₹74 crores. Despite a slight dip in year-on-year revenue, the bottom line is getting thicker.

Refex isn't just about refrigerant gases anymore. They are a massive player in ash and coal handling. They’re currently working across roughly 40 thermal power plants. In January 2026 alone, they bagged multiple orders worth over ₹43 crore and ₹30 crore for transporting pond ash to NHAI road projects. These are five-month and four-month contracts. Quick turnaround. Steady cash.

Breaking Down the Business Verticals

Refex is a bit of a shapeshifter. They started in 2002 with refrigerant gases (hence the name "Refex"), but the current revenue engine is Ash & Coal Handling.

- Ash and Coal Handling: This is the bread and butter. It contributed over ₹400 crore to the standalone revenue in the September 2025 quarter. They handle about 70,000 metric tons daily and want to push that to 110,000 within three years.

- Green Mobility: There’s a big de-merger happening here. Refex Green Mobility Limited is being carved out into its own listed entity. It's a strategic move to unlock value. If you're a shareholder now, you're essentially waiting for this split to finalize, which usually takes 6–7 months.

- Wind Energy: They’ve ventured into manufacturing 5.3 MW wind turbines. They claim these have an "edge" over competitors, and the order book here is sitting at a massive ₹1,225 crores. Revenue from this segment is expected to start hitting the books in Q4 FY26.

Analyzing the Refex Industries Ltd Share Price Value

When you look at the valuation, the P/E ratio is sitting around 19 to 20. Compare that to the industry average of over 45, and you start to wonder if the market is missing something.

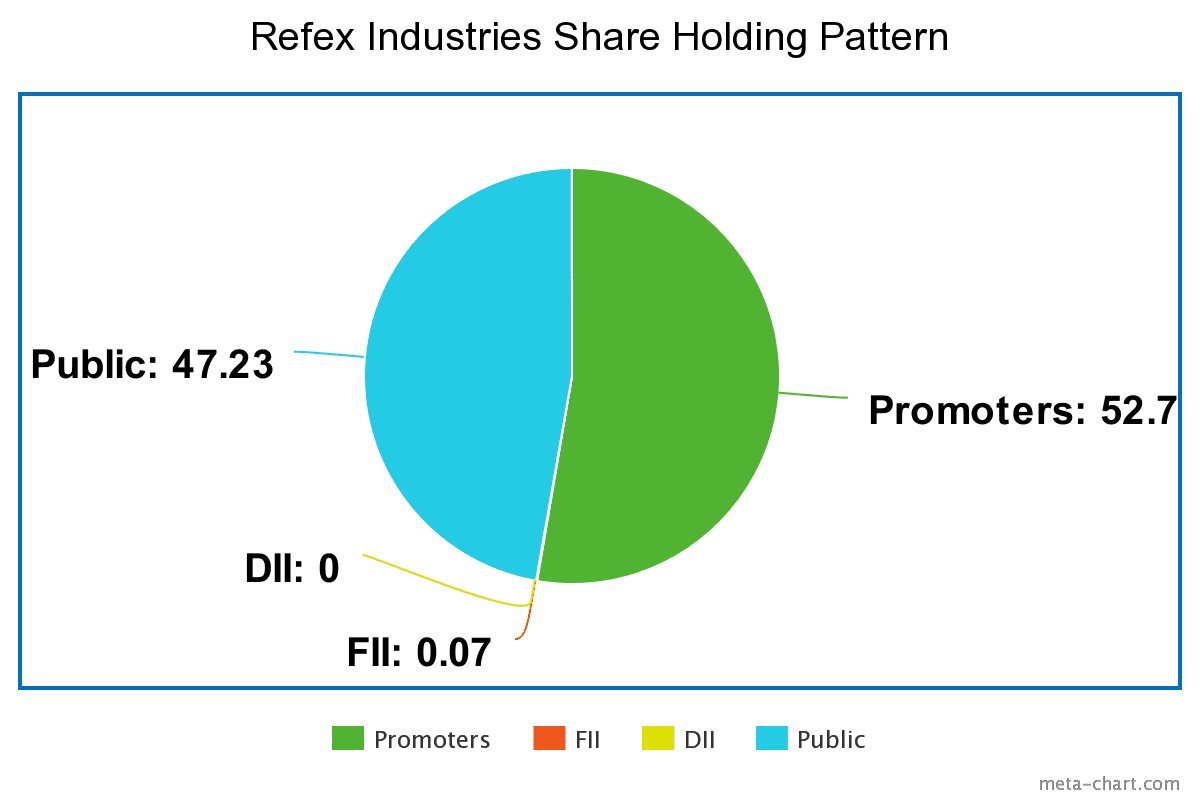

Promoters seem to think so. They actually increased their stake by more than 2% in the last quarter of 2025. When the people running the show are buying more shares while the price is dropping, it’s usually a signal that they believe the current Refex Industries Ltd share price doesn't reflect the company's intrinsic value.

Debt is another area where they’re winning. The debt-to-equity ratio is roughly 0.14. In a high-interest-rate environment, having almost no debt is like having a superpower. They’ve even managed to pay out a 25% interim dividend for FY26 (₹0.50 per share) back in August 2025.

What to Watch in Q3 Results

Mark your calendars for January 21, 2026. The Board of Directors is meeting to approve the Q3 and nine-month financial results. This is the big one. Why? Because management previously mentioned that the impact of the monsoons (which slows down ash handling) would be largely behind them by this quarter.

If they show a strong rebound in site activity, it might be the catalyst the stock needs to break out of its current slump. On the flip side, technical indicators like the RSI and moving averages currently suggest the stock is in a "weak momentum" phase. It’s trading below its short and long-term averages, which often keeps cautious traders on the sidelines.

Actionable Insights for Investors

If you’re holding Refex or considering it, don’t just stare at the daily price fluctuations. Here is what actually matters for the long term:

📖 Related: Converting 500 Pesos to USD: Why the Rate You See Isn't Always the Rate You Get

- The De-merger Timeline: The mobility vertical's separation is the most significant structural change. Keep an eye on regulatory filings regarding the "Refex Mobility Limited" listing.

- Wind Revenue: Check the Q4 results later this year to see if that ₹1,225 crore order book for turbines actually translates into realized cash flow.

- Order Book Execution: They have a ₹1,200 crore order book in coal and ash handling. The stock's recovery depends on how fast they can turn those orders into revenue without letting margins slip.

- Tax Clearance: The shadow of the Income Tax search will likely linger until a formal "all clear" or a settlement is announced.

The Refex Industries Ltd share price is currently caught between strong fundamentals and a nervous market sentiment. While the valuation looks attractive on paper—especially with the low debt and high ROCE—the technical "downward momentum" means catching this falling knife requires a high risk appetite and a long-term horizon.

Wait for the January 21st earnings call. Listen specifically for updates on the wind turbine manufacturing timelines and the status of the mobility de-merger. These are the two levers that will determine if the stock revisits its ₹500+ glory days or continues to consolidate in the ₹200–₹250 range.