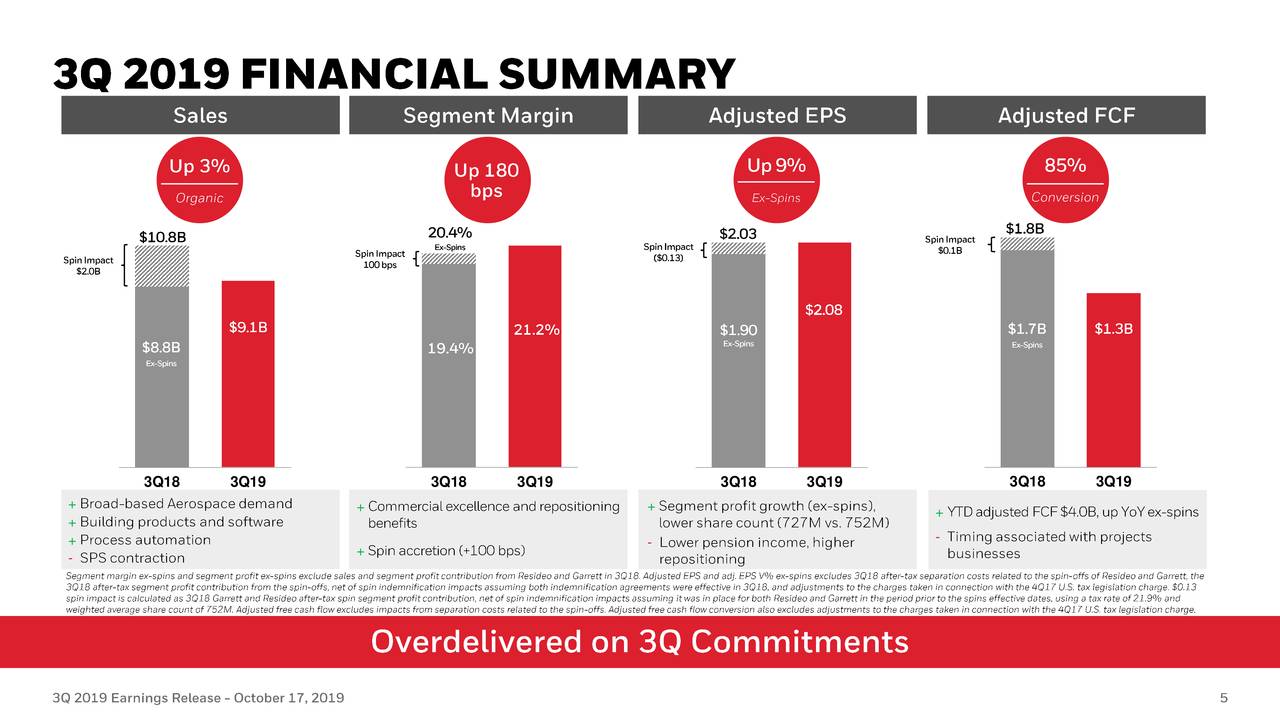

Honeywell is a weird one. Honestly, if you look at the stock price Honeywell International has been sporting lately, you might think it's just another slow-moving industrial giant. But that's exactly where most people get it wrong. As of mid-January 2026, the stock is hovering around $213. It’s up about 7% for the year, which isn't exactly "to the moon" territory, but there is a massive structural shift happening under the hood that the average retail trader is completely missing.

You've probably seen the headlines about the "Honeywell Breakup." It’s not really a breakup in the messy, legal sense, but more of a surgical extraction. CEO Vimal Kapur is basically taking a sledgehammer to the old conglomerate model.

The $213 Question: Is it Undervalued?

Most analysts on Wall Street—about 46 of them if you’re counting—are sitting on the fence with a "Hold" rating. But here’s the kicker: their median price target is up around $233. Some bulls are even whispering about $270.

✨ Don't miss: The JPMorgan Chase Return to Office Reality: What Really Happened to Wall Street Work Culture

Why the gap?

It's the complexity tax. Markets hate complexity. Right now, Honeywell is a bit of a jigsaw puzzle. You have Aerospace, Building Automation, Industrial Automation, and Energy/Sustainability all living under one roof. By the second half of 2026, that's all changing.

The Great Separation of 2026

If you're holding HON stock right now, you're basically holding a ticket to three different companies.

- Honeywell Aerospace Technologies: This is the crown jewel. It’s being spun off as a standalone pure-play. These guys make everything from propulsion systems to cockpit tech. In 2025, their organic growth was hitting 12%. When this becomes its own stock later this year, it’s likely to get a much higher valuation than the parent company currently enjoys.

- The "New" Honeywell (Automation): This will be the remaining core business, focusing on "autonomy." Think software-defined buildings and factories.

- Solstice Advanced Materials: This was the first piece of the puzzle to go, focused on specialty chemicals.

When a company spins off a high-growth division like Aerospace, the parent stock usually experiences a bit of a "conglomerate discount" lift. Basically, the market stops punishing the profitable parts for the slower parts.

What the Numbers Actually Say

Let's talk cold, hard cash. Honeywell is trading at a P/E ratio of roughly 22x. Compared to the broader industrial sector, that looks a bit expensive. But compared to its actual peers—the companies it will be competing with once the spin-offs are done—it’s actually trading at a discount.

👉 See also: The Real Connection Between Black Gold and Blue Hydrogen

- Intrinsic Value: Some DCF (Discounted Cash Flow) models put the "fair" price at $248. That’s a 15% discount from where we are today.

- Dividends: They just paid out $1.19 per share. The yield is sitting at a comfortable 2.2% or so. It’s reliable. They’ve been growing that dividend for years, and they’ve already committed billions to share buybacks.

- The Quantinuum Wildcard: Honeywell owns a massive stake in Quantinuum, a quantum computing leader. They just had a capital raise at a $10 billion valuation. They're planning an IPO for this unit too. That’s a lot of "hidden" value that isn't fully reflected in the $213 share price yet.

Why Some People are Scared

It’s not all sunshine. The bear case is pretty simple: execution risk. Splitting a century-old company into three pieces is like trying to change the tires on a car while it’s doing 80 mph on the highway. There are tax implications, leadership shifts, and the simple reality that the "Industrial Automation" segment has been a bit sluggish lately, with growth staying flat while Aerospace carries the weight.

Plus, we’re dealing with "unpredictable macroeconomics." That’s corporate speak for: "If interest rates stay weird or global trade hits a snag, our guidance might go out the window."

How to Play the Honeywell Transition

If you are looking at the stock price Honeywell International as a long-term play, the next six months are critical.

Watch the January 29th Earnings Call. This is the big one. They’ll be releasing their full 2026 outlook. If they confirm the Aerospace spin-off is on track for the second half of the year without any tax hitches, expect the stock to start creeping toward that $230 mark.

Don't ignore the cash flow. Honeywell generated over $5 billion in free cash flow last year. That’s the fuel for the buybacks. When a company is aggressively buying back its own shares while the market is "unsure," it’s usually a signal that leadership thinks the stock is cheap.

The "New" Segment Reporting. Starting in Q1 2026 (right now), they are changing how they report their numbers. They're grouping things into Building Automation, Industrial Automation, and Process Automation & Technology. This is designed to show investors exactly how profitable the "automation" side of the business is without the Aerospace noise. If those margins expand, the stock moves up.

Actionable Takeaways for Investors

If you're currently holding or thinking about buying, keep these three points in your back pocket:

- The Aerospace Spin-off is the Catalyst. Pure-play aerospace companies (like GE Aerospace) often trade at higher multiples than conglomerates. You're essentially buying into that eventual "re-rating."

- Focus on the 2026 Dividend. Historically, spin-offs can mess with dividend yields. However, Honeywell has a long-standing commitment to shareholder returns. Check the "tax-free" status of the distribution—it’s currently planned to be tax-free for U.S. shareholders.

- Quantum is the "Call Option." Treat the Quantinuum stake as a free lottery ticket. If quantum computing takes off, Honeywell’s stake could be worth a significant chunk of its total market cap.

The smart move here isn't to trade the daily fluctuations. It's to realize that the Honeywell of 2027 will look nothing like the Honeywell of today. You're buying a transformation in progress.

Next Steps for Your Portfolio:

Track the specific organic growth of the "Industrial Automation" segment in the upcoming Q4 report. If that number turns positive (above 2-3%), the biggest drag on the stock price will have been removed, potentially clearing the path for the $240+ analyst targets. Ensure you have a clear understanding of your brokerage's policy on spin-off shares (fractional shares vs. cash-in-lieu) before the H2 2026 deadline.