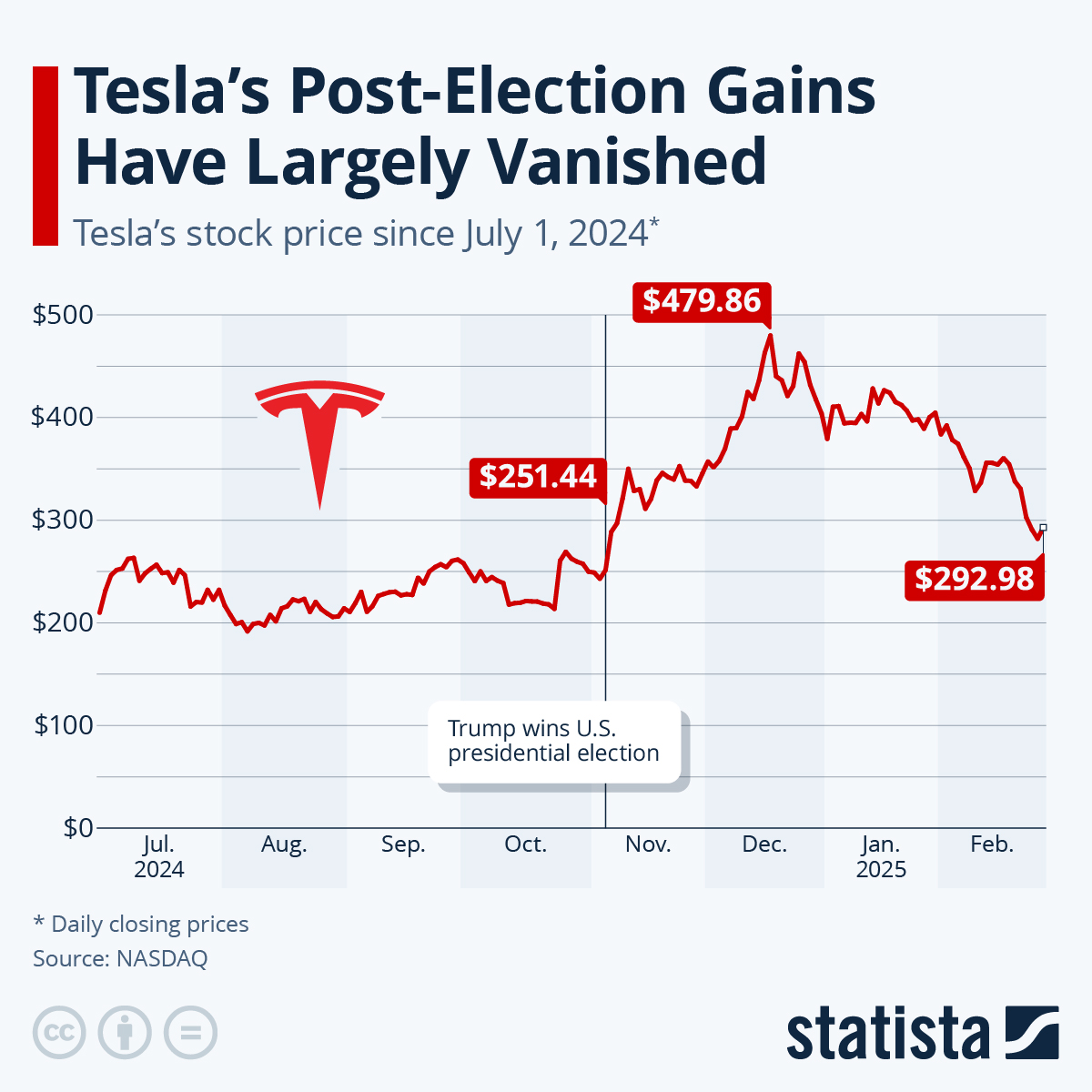

Tesla isn't a car company anymore. Honestly, if you're still looking at vehicle delivery charts to figure out the stock price tesla today, you're basically reading a map of a city that's already been demolished.

As of Tuesday, January 13, 2026, Tesla (TSLA) is hovering around the $447.20 mark. It’s down a fraction—about 0.39%—but that tiny wiggle in the numbers hides a much more chaotic reality happening under the hood of the global markets. The stock opened at $450.20 and hit a high of $451.81 before the afternoon "CES hangover" started to set in.

Why the stagnation? It's simple. Investors are currently trapped between two wildly different versions of the future.

On one side, you've got the hardware reality. Tesla just rolled out a massive "Tesla bonus" in Norway to fight off a nasty VAT increase that was killing sales. They also launched a new Model Y Standard Long Range in Europe with a 657 km range because, let's face it, range anxiety is still the boogeyman of the EV world. But on the other side, the AI side, the competition is getting scary. At CES 2026 in Las Vegas, Nvidia just dropped their "Alpamayo" AI model for autonomous driving. People are calling it a "Tesla-killer" software suite, and that’s making the TSLA bulls a little twitchy.

The $1.4 Trillion Identity Crisis

Tesla’s market cap is sitting at $1.49 trillion. That is a staggering number for a company that some analysts, like the folks over at GLJ Research, think is still just a "car company" with a bloated valuation. But if you talk to Dan Ives at Wedbush, he’s looking at a $2 trillion to $3 trillion bull case.

How can two smart people see the same stock price tesla today and come to such opposite conclusions?

It’s about the "AI Chapter." Right now, Tesla is trading at a price-to-earnings (P/E) ratio of nearly 300. For context, most legacy automakers like Ford or GM trade at a P/E of around 8 or 9. You’re not paying for the steel and the tires. You’re paying for the Robotaxi. You’re paying for the Optimus robot. You’re paying for the dream that Elon Musk’s "Master Plan IV" actually works.

If the Robotaxi fleet doesn't start showing real, unsupervised miles soon, that $447 price point is going to feel like a very long way down.

👉 See also: Wealthiest People in Maine Explained (Simply): The Names You Might Not Know

Why the Next 15 Days Matter More Than Today

The real catalyst isn't today’s minor dip. It’s January 28, 2026.

That’s when Tesla drops its Q4 2025 financial results. We already know the production numbers: they produced 434,000 vehicles and delivered 418,000 in the final quarter of last year. They also deployed a record 14.2 GWh of energy storage. The "Energy" side of Tesla is the quiet hero here, growing at a rate that would make most tech companies weep with envy.

But the earnings call is where the blood is. Analysts expect earnings of about $0.44 per share. If they miss that, or if Musk gets on the call and starts talking about Mars instead of margins, the stock price tesla today will look like a bargain compared to the post-earnings fallout.

Tom Zhu, Tesla’s "top problem solver," just got a massive equity award disclosed in regulatory filings today. That's a huge signal. Tesla is locking in its best operational talent because they know the "Cybercab" production ramp-up in April 2026 is going to be a nightmare. Cars without steering wheels? Legal hurdles in the U.S.? It’s a mess. A beautiful, high-stakes mess.

The Competition is No Longer Just BYD

For years, the story was "Tesla vs. China." While companies like XPeng are launching 800V architectures that charge to 80% in 12 minutes, the threat has shifted.

The real enemy now is Silicon Valley and the chipmakers. Nvidia isn't just making GPUs for gamers anymore; they are moving directly into Tesla's "Full Self-Driving" (FSD) territory. When Nvidia’s Jensen Huang says his AI models are the new gold standard, investors listen. Tesla’s FSD v14 is impressive, sure, but it’s still "supervised." The market is getting impatient for the "unsupervised" leap.

What You Should Actually Do

If you’re holding TSLA or thinking about jumping in, stop looking at the daily ticks.

First, watch the 10-year Treasury yields. Growth stocks like Tesla hate high rates because it makes future earnings look less attractive. Second, keep an eye on the "One Big Beautiful Bill Act" (OBBBA) stimulus. There’s about $270 billion in business tax incentives starting to flow in February 2026, and Tesla is positioned to swallow a huge chunk of that through their energy and industrial segments.

Actionable Steps for Investors:

- Verify the "Energy" Growth: Check the Q4 earnings on Jan 28 specifically for the margin on energy storage. If the energy business is subsidizing the hardware price cuts, Tesla’s valuation is safer than it looks.

- Monitor the FSD v15 Beta: Rumors are swirling about a mid-Q1 release. Any sign of "unsupervised" certification in even one state (likely Texas) will send the stock north of $500.

- Set Stop-Losses Around $415: This has been a heavy support level. If it breaks, the next stop is $380, which is the current Wall Street average price target.

The stock price tesla today is a snapshot of a company in transition. It’s no longer about how many Model 3s are in driveways. It’s about whether Elon Musk can turn a car company into an AI utility before the competition catches up to his lead. It's a gamble, but then again, it always has been.