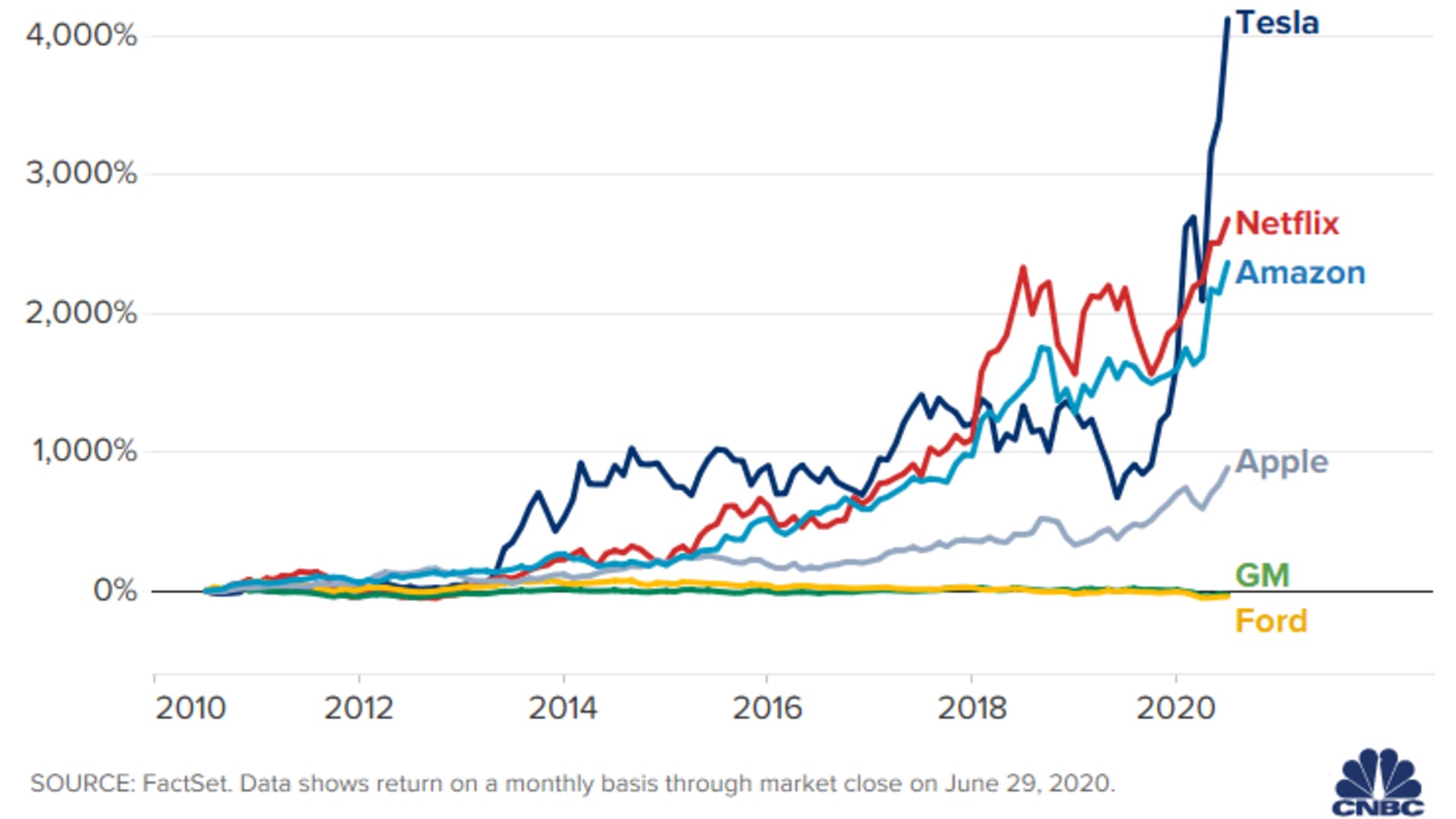

Honestly, if you're looking at the stock value of tesla today and only seeing a car company, you’re basically reading the last chapter of an old book while everyone else has moved on to the sequel. It’s January 2026. The vibe in the markets is... well, it's weird. We just saw the 2025 delivery numbers come in at 1.64 million vehicles. That’s a drop for the second year in a row. For any other car maker, that’s a "call the board of directors" level emergency.

But this is Tesla.

People are freaking out because the "Hypergrowth" narrative for the Model 3 and Model Y feels like it hit a brick wall. The federal EV subsidies in the U.S. are largely gone now, thanks to the policy shifts after the 2024 election. It's a tougher environment. Yet, somehow, the stock is still trading at a valuation that makes Toyota look like a lemonade stand. Why? Because the math has shifted. We aren't just counting wheels anymore; we’re counting neurons in an AI and gigawatt-hours in a box.

Why the Stock Value of Tesla is Losing Its "Car Company" Label

Most investors are stuck in 2021. They want to see 50% year-over-year delivery growth. They aren't getting it. In fact, total 2025 production was about 1.65 million units—way below the 2 million mark Elon Musk was hinting at a couple of years back.

But look at the margins.

The energy division is low-key carrying the team right now. In Q3 2025, Tesla Energy hit a 30.5% profit margin. To put that in perspective, the automotive side (excluding those juicy regulatory credits) has been sweating just to stay in the mid-teens. The Megapack is essentially a money-printing machine at this point. While everyone was obsessed with whether the Cybertruck would rust or not (and yeah, those 115,000 recalls in 2025 didn't help), the energy side deployed 14.2 GWh in Q4 alone.

If you're trying to value the company, you have to split your brain in two. One side is a maturing, slightly struggling car manufacturer facing brutal competition from BYD. The other is a high-margin energy and software powerhouse.

The FSD v14 Factor and the "Cybercab"

The real reason the stock value of tesla hasn't pulled a "Nokia" is the software. We just saw FSD v14 roll out, and for the first time, MotorTrend actually gave it the "Best Driver Assistance" award. That's a huge pivot from the skepticism of two years ago.

- Human-like behavior: It’s taking "hints" from other drivers now.

- The 7-billion-mile milestone: The data moat is getting ridiculous.

- The Unboxed Process: They’re betting the farm on a new way to build the Cybercab in Texas starting this April.

Musk is promising volume production of the $30,000 Cybercab—no pedals, no steering wheel—by the end of this year. Analysts like Dan Ives from Wedbush are still banging the drum that this could add a trillion dollars to the valuation. But let's be real: we've heard "next year" for the robotaxi since 2019. The difference in 2026 is that the hardware is actually sitting on the test tracks in Fremont.

The Bear Case: Why Some Analysts Set a $25 Target

You can't talk about the stock value of tesla without mentioning the bears like Gordon Johnson. He’s still out there with targets that look like a typo—around $25. While that seems extreme, the logic isn't entirely hollow. If the Robotaxi fails to get regulatory approval or if the "Unboxed" manufacturing process turns into a "production hell" sequel, Tesla is just a car company with declining sales and huge R&D costs.

The 2025 revenue estimates are hovering around $28 billion for Q4, which is actually lower than Q4 2024. That’s a scary stat. It means the price cuts Tesla used to move metal last year really chewed into the bottom line.

👉 See also: 160 USD to PKR: Why the Rate is Moving This Way in 2026

What to Watch on January 28

The Q4 2025 earnings call on January 28 is going to be a bloodbath or a celebration. There is no middle ground. Wall Street is looking for three specific things:

- Automotive Gross Margin: Can they keep it above 17% without the federal tax credits?

- Optimus Progress: Is the robot actually doing anything useful in the factories yet?

- The Houston "Megablock" Factory: Updates on the 50 GWh facility are crucial for the energy narrative.

Actionable Insights for the "New" Tesla Reality

If you're holding or looking to buy, stop looking at monthly delivery charts. They’re noisy and, frankly, a bit depressing lately. Instead, track the FSD take-rate. If Tesla can convert 20% of its 7-million-car fleet to a $99/month subscription, that’s pure profit that doesn't require building a single new factory.

Sorta feels like we’re in the "awkward teenage years" of the company. The childhood of explosive car sales is over. The adulthood of being an AI robotics firm hasn't fully arrived.

Next Steps for Investors:

✨ Don't miss: Netflix Earnings Date October 2025: Why the Brazil Tax Hit Surprised Everyone

- Check the FSD v14 reviews from independent testers, not just the fanboys. If the disengagement rates are truly dropping toward Level 4 autonomy, the valuation floor rises significantly.

- Monitor the Houston Megablock construction. The energy business is currently the only thing growing at triple digits.

- Ignore the "Elon Noise" on X. Focus on the 10-K filings and the actual production rates of 4680 cells. That’s where the real story lives.

The stock value of tesla is currently a bet on a transition. You're either buying a legacy car maker at a 50x multiple (bad idea) or you're buying the world's largest distributed battery and AI network at a discount (potentially a great idea). Just make sure you know which one you're betting on before the January 28 volatility hits.

Bottom line: The 2026 outlook is basically a race between declining hardware margins and accelerating software revenue. If the Cybercab starts rolling off the line in Austin this April as promised, the $400+ price targets won't look so crazy after all. But if it slips to 2027? Grab your popcorn, it’s going to be a bumpy ride.