Tax season is usually a blur of caffeine and mild panic. If you’re looking at the 2023 1040 tax form right now, you might be feeling that familiar itch of "did I miss something?" It's not just you. Even though we are moving further away from the 2023 tax year, millions of Americans are still filing extensions, dealing with back taxes, or realizing they left money on the table. Honestly, the 1040 is the heartbeat of the IRS. It's the two-page document that decides if you’re getting a Caribbean vacation or if you're eating instant noodles for a month.

People think the 1040 is just a static piece of paper. It isn't. Every year, the IRS tweaks it, adjusts the numbers for inflation, and shuffles the schedules around just enough to keep you on your toes. For the 2023 tax year, specifically for those filing in 2024 or catching up now, the stakes were high because of the massive shifts in standard deductions and the way digital assets were treated.

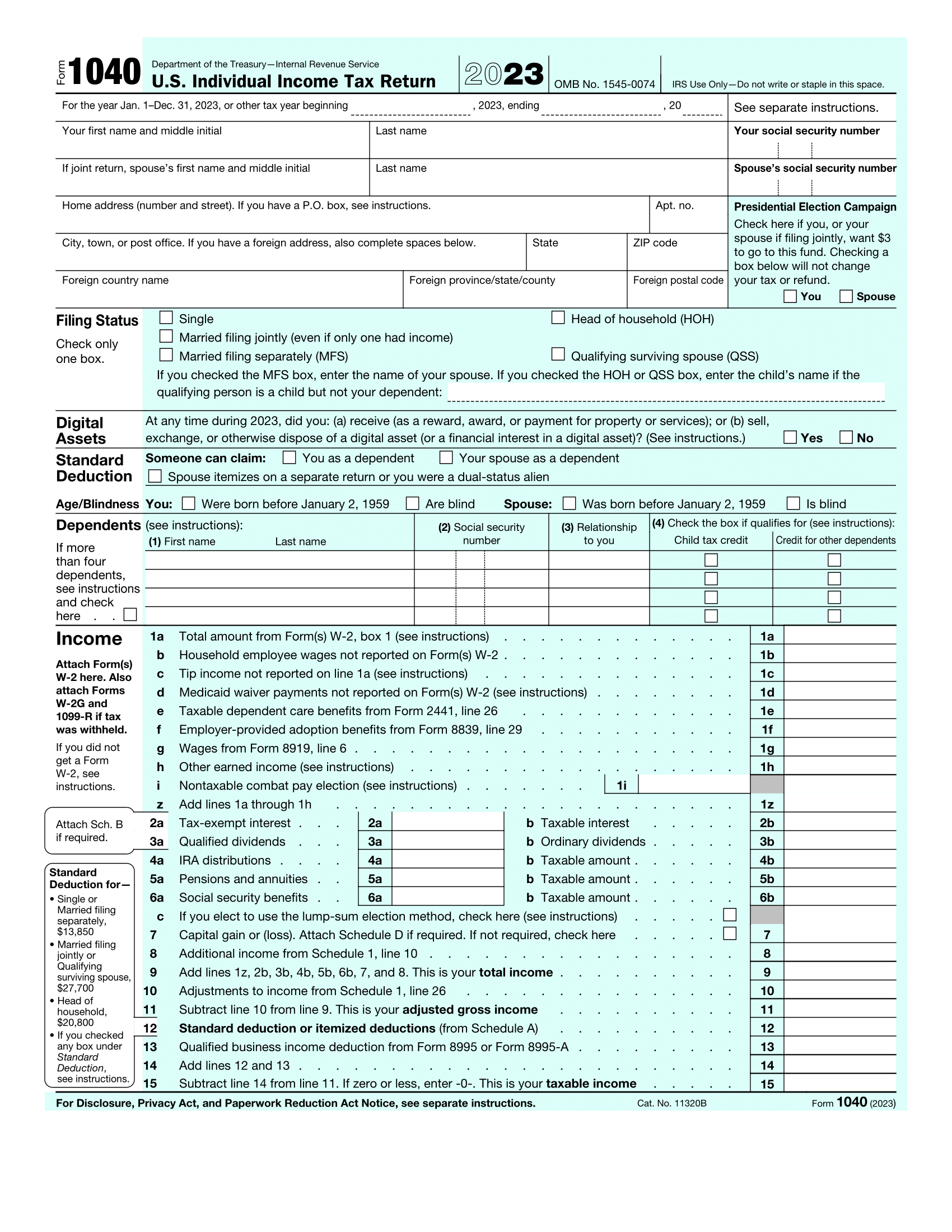

Why the 2023 1040 Tax Form Feels Different

It's about the money. Specifically, the IRS adjusted the tax brackets by about 7% for the 2023 tax year to account for the inflation we all felt at the grocery store. This was a big deal. If your salary stayed the same, you likely paid less in taxes than you did the year before.

But here’s where people trip up: the "gray" areas of the form.

👉 See also: Starbucks Store Closings: Why Your Local Cafe Might Be Next

Take the question about digital assets right at the top of the 2023 1040 tax form. It's not just there for decoration. The IRS is obsessed with crypto. If you sold, traded, or even used Bitcoin to buy a Tesla, you have to check "Yes." Many people think "I didn't sell for cash, so I don't need to report it." Wrong. That's a one-way ticket to an audit. The IRS defines "disposition" very broadly. If you swapped one coin for another, that’s a taxable event. Period.

The Standard Deduction Jump

For 2023, the standard deduction jumped to $13,850 for individuals and $27,700 for married couples filing jointly. That is a huge leap. It means that for the vast majority of people, itemizing—trying to track every single $10 donation to Goodwill or every mortgage interest payment—became a waste of time. Unless your total expenses exceed those high thresholds, you’re basically throwing hours of your life away by filling out Schedule A.

The Mystery of the Schedules

The 1040 itself is just the face of the operation. The real work happens in the schedules.

Think of the 2023 1040 tax form as a summary of a much longer, more boring book. Schedule 1 is where the "fun" stuff lives—business income, unemployment compensation, and those educator expenses that teachers always forget to claim. Did you know teachers can deduct up to $300 for out-of-pocket classroom supplies? It’s not much, but it’s something.

Then there’s Schedule 2 and 3. These deal with additional taxes (like the Alternative Minimum Tax) and nonrefundable credits. Most people ignore these until they realize they qualify for the Energy Efficient Home Improvement Credit. If you put in new windows or a heat pump in 2023, you’re looking at significant credits that flow directly onto the 1040.

A Real-World Example: The Freelance Trap

Imagine a graphic designer named Sarah. She’s a freelancer. Sarah looks at her 2023 1040 tax form and sees Line 1z (total income). She puts her total earnings there and thinks she’s done. But she forgot Schedule SE. Because she’s self-employed, she has to pay both the employer and employee portions of Social Security and Medicare. This is roughly 15.3%. Sarah’s $50,000 income suddenly looks a lot smaller after the self-employment tax hits.

This is where the nuances of the 2023 form matter. Sarah should have looked at the adjustments to income on Schedule 1. You can deduct half of your self-employment tax. It’s a "top-line" deduction, meaning it lowers your Adjusted Gross Income (AGI) before you even get to the standard deduction.

The "Dirty Dozen" and Your 1040

The IRS releases a list every year called the "Dirty Dozen." It’s basically a list of scams they are currently hunting. For the 2023 filing season, they were heavily focused on the Employee Retention Credit (ERC) and "ghost" preparers.

If you used a tax preparer who refused to sign your 2023 1040 tax form, you’ve got a problem. That’s a ghost preparer. They take your money, claim fake credits to get you a bigger refund, and then disappear when the IRS sends a letter. You are legally responsible for every single number on that form, even if a professional filled it out for you.

Credits That Actually Matter

Let's talk about the Earned Income Tax Credit (EITC). For the 2023 tax year, the maximum credit for those with three or more qualifying children was $7,430. That is life-changing money for some families. But the rules are dense. The IRS estimates that about 20% of eligible taxpayers don't claim it because they find the forms too intimidating.

- You must have earned income.

- Your investment income can't exceed $11,000 for the year.

- You must be a U.S. citizen or resident alien all year.

Then there is the Child Tax Credit. For 2023, it remained at $2,000 per qualifying child. However, the refundable portion—the part you get back even if you owe zero taxes—was capped at $1,600. It's a common misconception that the entire $2,000 is "cash back." It’s not. It’s a credit against what you owe first.

Common Errors That Trigger Delays

The IRS still uses some pretty old-school technology. If you hand-write your 2023 1040 tax form, your chances of a delay skyrocket. A simple typo in a Social Security number or a misspelled name (it has to match your Social Security card exactly!) can put your return in a manual review pile for months.

Another big one? Direct deposit info. One wrong digit in your routing number and your refund gets sent back to the IRS. Then you’re waiting weeks for a paper check in the mail.

Moving Parts: State vs. Federal

Your federal 1040 is the baseline for almost every state tax return. If you live in a state like California or New York, your AGI from the 2023 1040 tax form is the starting point for your state taxes. But be careful. Some states don't recognize the same deductions the federal government does. For instance, some states don't allow the same "bonus depreciation" rules for business equipment that the federal 1040 allows. It creates a "book-to-tax" difference that can be a nightmare for small business owners.

Actionable Steps for Handling Your 2023 Taxes

If you haven't filed yet, or if you think you made a mistake on your 2023 1040 tax form, don't just sit on it. The IRS is surprisingly easy to work with if you’re proactive.

- Gather the right documents. You need W-2s, 1099-NECs (for side gigs), and 1099-INTs for that high-yield savings account interest you probably forgot about.

- Check your AGI. If you're using software to file, it will ask for your 2022 AGI to verify your identity. If you don't have it, you can get a transcript from the IRS website.

- Look at Form 1040-X. If you realized you missed a deduction or forgot to report that Robinhood trade, file an amended return. It's better to tell the IRS you made a mistake than to have them tell you.

- Verify the Crypto question. Even if the answer is "No," don't leave it blank. Leaving it blank is an incomplete form.

- Contribute to an IRA. For the 2023 tax year, you had until the April 2024 deadline to contribute to a traditional IRA and potentially lower your taxable income on that 1040. If you missed it, keep it in mind for the current year.

Navigating the 2023 1040 tax form doesn't require a CPA degree, but it does require a bit of patience and an eye for detail. The form is shorter than it used to be—remember when it was a full page longer?—but the complexity has just shifted to the supporting schedules. Take it line by line. Double-check your math. And for the love of everything, make sure your signature is on the second page. A 1040 without a signature isn't a tax return; it's just a stack of paper.