If you’ve spent any time looking at a historical chart of mortgage rates, you probably felt a weird mix of relief and absolute panic. It's a wild ride. Most people look at the 7% or 8% rates of recent years and think the world is ending. They remember the "free money" era of 2021 when you could snag a 30-year fixed for 2.65% and feel like they missed the only boat that ever sailed.

But history is long. It’s messy.

When you zoom out—I mean really zoom out—you realize that for the last fifty years, "normal" has been a moving target. My parents bought their first place when rates were climbing toward 18%. They weren't speculators; they were just people who needed a roof. Today, we treat a 1% shift like a national emergency. Understanding the historical chart of mortgage rates isn't just about nostalgia; it’s about realizing that the ultra-low rates of the 2010s were the outlier, not the rule.

Why 1981 Still Haunts Every Federal Reserve Meeting

Let’s talk about the monster under the bed: October 1981.

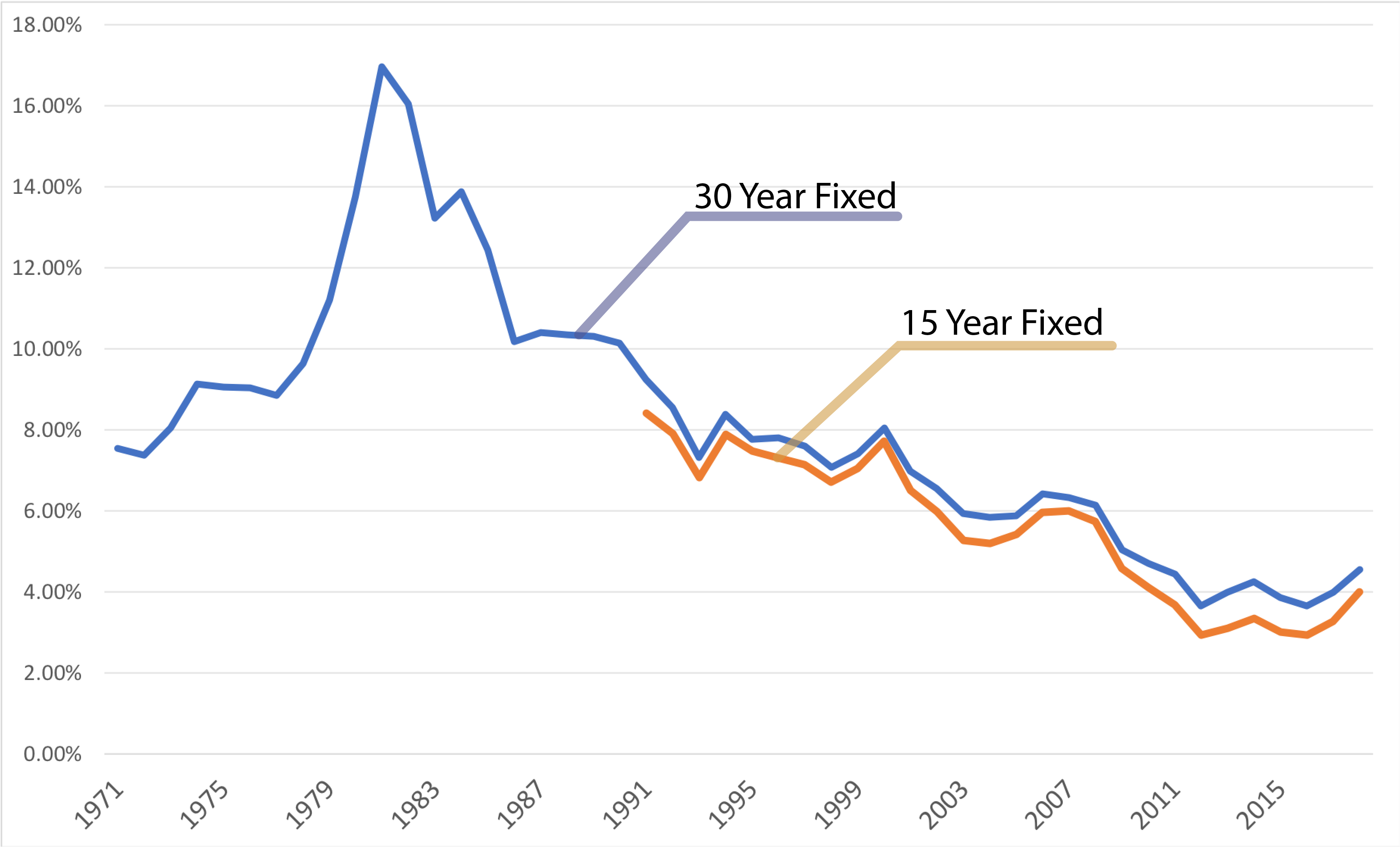

Freddie Mac started tracking the Primary Mortgage Market Survey (PMMS) in 1971. For a decade, things were relatively calm, with rates hovering between 7% and 9%. Then, the Great Inflation hit. Paul Volcker, the Fed Chair who looked like he ate cigars for breakfast, decided to break inflation's back by hiking the federal funds rate aggressively.

🔗 Read more: Why the Post It Super Sticky Easel Pad Still Dominates Your Strategy Meetings

By the time the dust settled in late '81, the average 30-year fixed-rate mortgage hit 18.63%.

Think about that. On a $100,000 loan, your interest payment alone was nearly $1,500 a month—in 1981 dollars. People weren't buying houses; they were assuming existing mortgages or using "creative financing" like balloon payments and seller carry-backs. If you look at the historical chart of mortgage rates, that peak looks like a jagged mountain top that hasn't been scaled since.

It took nearly a decade for rates to drop back into the single digits. By the early 90s, we were seeing 9% and feeling "lucky." It’s all about perspective. If you grew up in the 90s, a 7% rate felt like a gift from the heavens compared to what your older siblings paid.

The Long Slide to Zero (And Why It Broke Our Brains)

After the 1980s peak, the historical chart of mortgage rates shows a beautiful, agonizingly slow downward slope. It was a thirty-year bull market for bonds.

- The 90s: Rates averaged around 8.12%. We had the tech boom, and housing was steady.

- The 2000s: The "Great Moderation." Rates dropped into the 6% range, then the 5% range after the Dot-Com bubble burst.

- The 2008 Crash: This changed everything.

When the housing market imploded, the Fed stepped in with Quantitative Easing (QE). They started buying Mortgage-Backed Securities (MBS) by the truckload. This wasn't just a market shift; it was a thumb on the scale. For the first time ever, the historical chart of mortgage rates saw the 30-year fixed dip below 4%.

We stayed there for a long time. Too long, maybe?

Between 2011 and 2021, we became addicted to cheap debt. When the pandemic hit in 2020 and the Fed slashed rates to near zero, mortgage rates followed, bottoming out at an average of 2.65% in January 2021. That specific data point is the most dangerous number on the entire historical chart of mortgage rates because it created a "lock-in" effect. Millions of homeowners are now sitting on rates so low they can never afford to move, which has totally choked off the supply of existing homes.

Comparing the Decades: A Reality Check

| Era | Average 30-Year Fixed Rate | Context |

|---|---|---|

| 1970s | 8.86% | Decent growth, rising inflation |

| 1980s | 12.70% | The Volcker era and stagflation |

| 1990s | 8.12% | The "Normal" years |

| 2000s | 6.29% | Pre-crash exuberance |

| 2010s | 4.09% | The era of QE and recovery |

| 2020-2024 | 4.5% - 7.5% | The post-pandemic surge |

Actually, looking at a table is sort of boring. The real story is in the volatility. In 2022 alone, we saw the fastest doubling of mortgage rates in history. We went from roughly 3% to 7% in a matter of months. That kind of vertical movement on the historical chart of mortgage rates is what causes "sticker shock." It's not just that rates are high; it's that they moved so fast that the market couldn't breathe.

What the Experts Miss About the "Historical Average"

You’ll often hear pundits say, "The historical average for mortgage rates is around 7.7%."

Technically, they’re right. If you average every weekly Freddie Mac data point from 1971 to 2024, you get somewhere in that neighborhood. But averages are liars. If I have one hand in a bucket of ice and the other on a hot stove, on average, I’m comfortable.

💡 You might also like: Cook Walden Davis Funeral Home Georgetown TX: What to Actually Expect When Planning

The 18% rates of the 80s heavily weight that average upward. Conversely, the 3% rates of the 2010s weight it downward.

The real question for anyone looking at the historical chart of mortgage rates today is: Where is the "new neutral"?

Lawrence Yun, the Chief Economist at the National Association of Realtors, has often pointed out that mortgage rates track the 10-year Treasury yield. Usually, there’s a spread of about 1.7 to 2 percentage points. Recently, that spread widened to nearly 3 points because of market uncertainty and the Fed's balance sheet reduction.

This means that even if the economy stays the same, rates could drop just by the market "calming down" and the spread narrowing back to its historical norm.

The Psychological Trap of "Waiting for 3%"

Here is the hard truth. We are probably never seeing 3% again in our lifetimes unless there is another global catastrophe on the scale of 2008 or 2020.

If you look at the historical chart of mortgage rates, those sub-4% periods were interventions. They were artificial. Expecting them to return is like expecting gas to be 99 cents again. It’s a nice dream, but it’s not a financial plan.

What we’re seeing now—rates between 6% and 7.5%—is actually very consistent with the 1990s and early 2000s. The difference is the home prices. In 1995, a 7% rate on a $150,000 house was manageable. A 7% rate on a $500,000 house is a different beast entirely.

💡 You might also like: When Does Joann Fabrics Close: Why the Lights Are Going Out

The historical chart of mortgage rates tells us that people still buy houses at 7%. They still buy at 9%. They just buy less house. They adjust. They negotiate.

Actionable Insights: How to Use History to Your Advantage

Stop obsessing over the daily ticks. Seriously.

If you're looking at the historical chart of mortgage rates to try and time the bottom, you've already lost. Markets price in Federal Reserve moves months before they actually happen. Instead of trying to beat the chart, focus on the things you can actually control.

1. Marry the House, Date the Rate

This is a cliché for a reason. If you find a property that fits your life, buy it. If rates drop in three years, you refinance. If they go to 10%, you look like a genius for locking in 7%. The historical chart of mortgage rates shows that rates almost always cycle. You aren't stuck forever.

2. Focus on the Spread

Watch the 10-year Treasury note ($TNX). If the gap between the 10-year yield and the 30-year mortgage rate is over 2.5%, it’s a sign that mortgage rates are "overpriced" due to fear. When that gap shrinks, it’s often a better time to lock in a rate than waiting for the Fed to cut.

3. Credit Score is King

In the 80s, if you had a heartbeat, you got the 18% rate. Today, the "average" on the historical chart of mortgage rates is only for those with 740+ credit scores. If your score is 620, you aren't getting the "historical average"—you're getting a penalty. Improving your score by 50 points can save you more than a 1% drop in market rates.

4. Consider the 15-Year Option

If you look at the historical chart of mortgage rates for 15-year fixed loans, they consistently run about 0.6% to 1% lower than the 30-year. If you can swing the payment, the total interest savings over the life of the loan is staggering. You end up paying less than half the total interest of a 30-year loan at the same rate.

The bottom line? The historical chart of mortgage rates is a map of where we've been, not a GPS for where we're going. It shows resilience. It shows that the "perfect time" is usually just whenever you are financially ready to stop paying someone else's mortgage and start paying your own.

Don't let the ghosts of 1981 or the "free money" of 2021 haunt your decision-making today. Look at the long-term trend, check your own budget, and remember that real estate is a game of decades, not days.

Get your credit report in order today. Call a local lender and get a "manual underwrite" quote if your situation is complex. Stop looking at the national average and start looking at your specific "buy box." History happens whether you're participating or not.