You've probably seen those jagged lines on a Bloomberg terminal or a CNBC broadcast. They look like a mountain range made of debt. Most folks call it "the yield curve" and move on, but if you’re actually moving money—or trying to understand why your mortgage rate just spiked—you need to look at the treasury par yield curve.

It sounds dry. It sounds like something a middle-manager at the Fed obsess over while drinking lukewarm decaf. But honestly? It’s the heartbeat of the entire global financial system.

If the Treasury Department issues a bond today, they aren't just guessing on the interest rate. They use this specific curve to figure out what a bond is worth if it were priced exactly at its face value. That's what "par" means. It’s the coupon rate that makes the bond’s price equal to 100% of its principal. Simple, right? Not exactly.

Why the treasury par yield curve is actually a mathematical ghost

Here is the thing: the par curve doesn't actually exist in the "wild" like a stock price does. You can't go out and buy "The Par Curve." It’s a derived set of data.

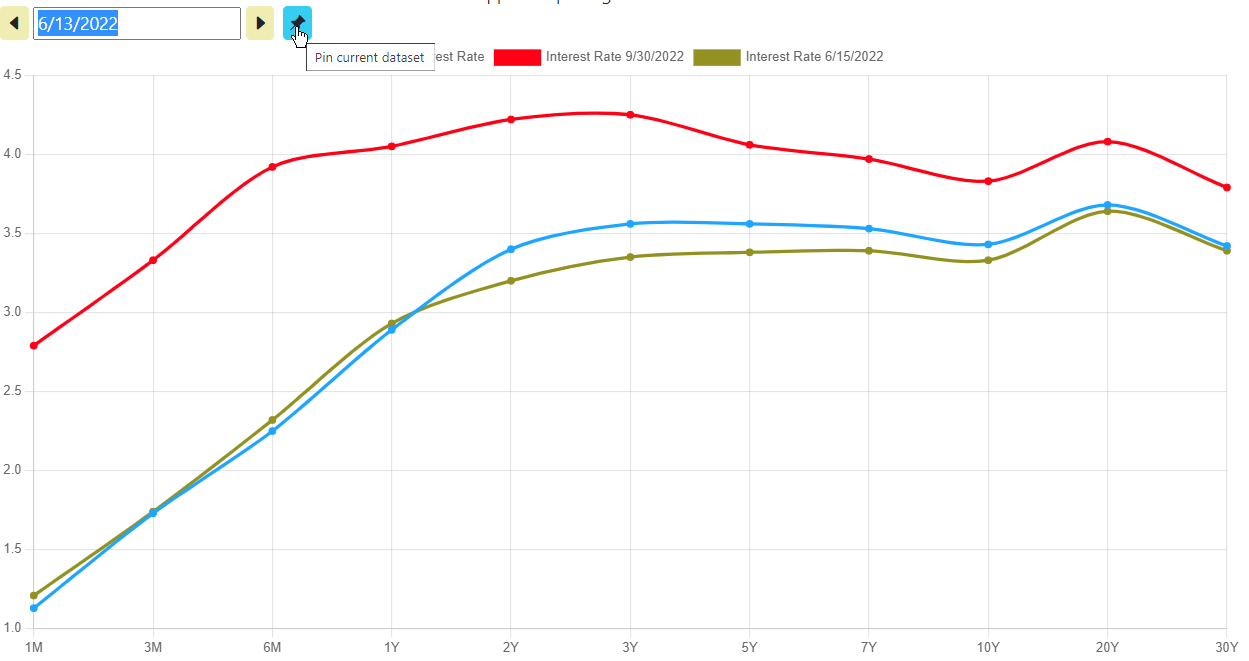

The U.S. Treasury pulls this together every day after the markets close. They look at the "on-the-run" securities—those are the most recently issued, most liquid notes and bonds—and they use a bunch of math to fill in the gaps. They use something called a quasi-cubic hermite spline. Sounds like a sci-fi weapon. In reality, it’s just a way to draw a smooth line through a bunch of scattered data points so there aren't weird jumps in interest rates from a 5-year bond to a 7-year bond.

Most people confuse this with the spot curve or the forward curve. Big mistake.

The spot curve is about single payments (zero-coupon bonds). The treasury par yield curve is about bonds that pay you along the way. If you’re a corporate CFO looking to issue new debt, you aren't looking at spot rates; you’re looking at par yields because that tells you what your coupon should be to attract investors without having to sell your debt at a massive discount.

The weird psychology of the 10-year

Look at the 10-year Treasury. It's the benchmark for everything. When the par yield on the 10-year moves, the world shifts.

Why?

Because of the "par" part. Investors want to know what the current "fair" rate is for a decade of lending their cash to Uncle Sam. If the par yield is 4.2%, and you’re holding an old bond paying 2%, you’re feeling the burn. Your bond is now worth less than par. You’re "underwater" in the bond world. This relationship—this constant tug-of-war between the par curve and the secondary market—is where the real money is made and lost.

How the Fed messes with your head

The Federal Reserve doesn't control the whole curve. They wish they did. They really only have a firm grip on the very front end—the short-term stuff.

When Jerome Powell stands up and talks about "higher for longer," he’s trying to yank the front of the treasury par yield curve upward. But the long end? The 10-year, the 20-year, the 30-year? That’s the "wisdom of the crowds." Or the madness of them.

Sometimes the curve flips upside down.

An inverted yield curve is the financial equivalent of a "check engine" light. It happens when short-term par yields are higher than long-term ones. It’s basically the market saying, "We think things are going to be so bad in three years that we’ll take a lower interest rate then just to be safe now." It has predicted almost every recession since the 1950s. It’s not a perfect crystal ball, but it’s the closest thing we’ve got.

👉 See also: Finding the Right Clipart of a Dollar Bill Without Getting Sued

The "On-the-Run" bias

I mentioned "on-the-run" earlier. This is a nuance most retail investors miss.

The Treasury Department focuses on the newest bonds because they trade the most. But there are thousands of "off-the-run" bonds—older ones—floating around. Sometimes the par curve doesn't perfectly reflect these older bonds because they might be less liquid or have weird tax implications.

If you see a discrepancy between the treasury par yield curve and what an old 2035 bond is doing, that’s an opportunity. Or a warning. Usually a warning.

Real world impact: From mortgages to Macbooks

You might think, "I don't own bonds, why do I care?"

You care because the par curve dictates your life.

- Mortgages: Banks price 30-year fixed mortgages based on the 10-year par yield plus a "spread" (usually 1.5% to 3%).

- Auto Loans: These usually track the 2-year or 5-year par yields.

- Corporate CAPEX: When Apple or Amazon wants to build a new data center, they check the par curve to see if it’s cheaper to borrow for 5 years or 10 years.

If the par curve steepens—meaning long-term rates rise faster than short-term ones—banks get happy. They borrow short and lend long. If it flattens? Banks get cranky. They stop lending. And when banks stop lending, the economy grinds to a halt.

The 2024-2025 Shift

Recently, we've seen some wild swings. We spent a long time in a "deep inversion." People were screaming about a recession that didn't quite show up on schedule.

What changed?

The term premium. That’s the extra "oomph" investors demand for the risk of holding a bond for a long time. For years, the term premium was basically zero or even negative. Now, it’s clawing its way back. This makes the treasury par yield curve look "normal" again, but the transition period is usually chaotic. It’s like a bone being reset. It hurts while it's happening, even if it's better in the long run.

Reading the data like a pro

If you go to the Treasury’s website, you’ll see a sea of numbers. Don’t get overwhelmed.

Look at the "1-month" and compare it to the "10-year." That’s your basic spread.

Then look at the "7-year." It’s often the "belly" of the curve. If the 7-year par yield is bulging outward, it means there’s a lot of demand—or a lot of fear—concentrated in the medium term.

Why "Par" matters for duration

Duration is a fancy word for how sensitive a bond is to interest rate changes.

A bond trading at par has a very predictable duration. If it’s trading way above or below par, the math gets messy. By using the treasury par yield curve as your baseline, you’re looking at the "cleanest" version of interest rate risk. It strips away the noise of individual bond quirks and gives you the pure, unadulterated price of time.

Because that’s all an interest rate is: the price of time.

Actionable steps for the savvy observer

Stop looking at the stock market in a vacuum. It’s a side show. The bond market is the main event.

First, bookmark the Daily Treasury Par Yield Curve Rates page. It’s updated every business day around 6:00 PM ET.

Second, watch the 2-year and 10-year spread. If it’s negative, keep your cash in high-yield savings or short-term T-bills. You’re getting paid more to take less risk. That’s a gift. Don’t ignore it.

Third, if you’re planning a big purchase—a house, a car, a business expansion—watch the 5-year par yield. It’s the most sensitive to mid-term inflation expectations. If it starts ticking up while the Fed is saying they’ll cut rates, the market is calling the Fed’s bluff. Trust the market.

Finally, understand that the treasury par yield curve is a reflection of us. It’s a collective mathematical representation of every fear, every bit of greed, and every expectation of the future held by millions of people across the globe. It’s the most honest thing in finance because it involves trillions of dollars voting on what tomorrow looks like.

Pay attention to the curve. It’s usually telling you exactly what’s coming next, if you’re willing to do the math.

Next Steps for Implementation:

- Audit your fixed-income portfolio: Compare your current holdings' coupon rates against the latest par yields to determine if you are holding "discount" or "premium" debt.

- Monitor the 2/10 Spread: Check the Daily Treasury Par Yield Curve Rates once a week. A shift from a negative to a positive spread (re-steepening) often precedes significant market volatility.

- Evaluate borrowing timing: If the 5-year par yield is trending downward while the 30-year remains high, consider shorter-term financing options with the intent to refinance later.