Honestly, if you had grabbed just a few handfuls of Taiwan Semiconductor Manufacturing Company (TSM) stock back in the early 2000s and fell into a coma, you’d wake up today in a different tax bracket. We’re talking about a company that basically functions as the lungs of the global tech economy. Without them, your iPhone is a glass brick, and Nvidia’s AI dreams are just expensive PowerPoints. Looking at the TSM stock price history, it isn’t just a line going up; it’s a map of how the world became obsessed with silicon.

Back in January 2000, TSM was trading around $8.40. Fast forward to mid-January 2026, and we've seen it screaming past $340. That's not just growth; that's a total takeover.

The Early Days and the "Slow" Burn (1997-2010)

When TSM first hit the New York Stock Exchange as an ADR in 1997, it wasn't exactly a household name. Most people didn't get the "foundry model." Why would a company just make chips for others instead of designing their own? Intel was the king because they did both.

But Morris Chang, the legendary founder, saw something others didn't. He realized that as chips got smaller, the factories (fabs) would get so expensive that only one or two companies could afford to build them. He was right.

For the first decade, the TSM stock price history was... well, kinda boring. It bumped along between $3 and $10 for years. It survived the dot-com bubble burst, though it took a 50% haircut in 2002, dropping to under $4. If you were an investor then, you needed nerves of steel and a lot of patience.

The Smartphone Era Changed Everything

Everything shifted when the world moved from PCs to pockets. Around 2010, the stock started to find its footing, crossing the $12 mark. Why? Because the mobile revolution needed low-power, high-performance chips, and TSM was the only one who could reliably churn them out at scale.

Then came the Apple deal.

Once TSM became the primary manufacturer for Apple’s A-series chips, the stock price stopped walking and started running. By 2017, the market cap actually surpassed Intel’s for the first time. It was a symbolic passing of the torch. TSM wasn't just a "contract manufacturer" anymore; they were the gatekeepers of the future. By late 2017, the price was comfortably in the $40s.

The 2020-2022 Rollercoaster: Shortages and Slumps

You probably remember the "everything shortage" during the pandemic. Cars were sitting in lots because they lacked $2 microcontrollers. This was a double-edged sword for TSM. On one hand, demand was through the roof. On the other, the world realized how scary it was that 90% of advanced chips came from one island.

🔗 Read more: Merck in Rahway NJ Explained: Why the Landmark Campus is Changing Everything

In 2020, the stock nearly doubled, ending the year around $100. It peaked in early 2022 near $140 before the "hangover" hit. High inflation and fears of a PC/smartphone slump sent the price tumbling back down to the $60 range by October 2022.

Many people thought the party was over. They were wrong. They just didn't see the AI wave coming.

The AI Explosion (2023-2026)

If the smartphone era was a steady climb, the AI era has been a rocket launch. Since early 2023, TSM has outperformed the Nasdaq significantly.

- 2023: The stock began recovering as Nvidia’s H100 chips became the most valuable commodity on Earth. TSM ended the year around $104.

- 2024: This was the breakout year. The stock almost doubled again, hitting $150 and eventually crossing the $200 threshold as 3nm production ramped up.

- 2025: A massive year for the "Trillion Dollar Club." TSM's market cap blew past $1.5 trillion as earnings grew by nearly 50%.

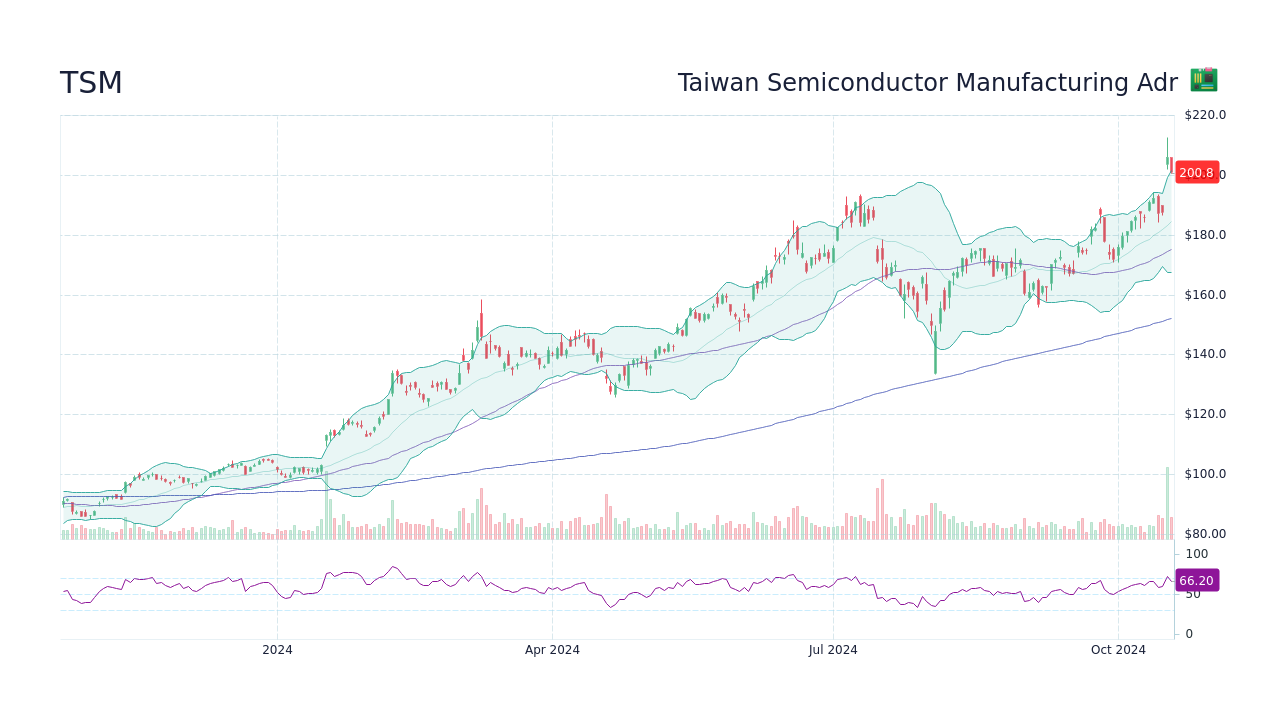

- Current Status (January 2026): We are seeing all-time highs. On January 16, 2026, the stock closed at $342.44.

What’s driving the current $340+ price?

Honestly, it's the margins. In the most recent Q4 2025 earnings report, TSM posted a gross margin of 62.3%. That’s unheard of for a hardware company. They aren't just selling chips; they are selling "bottlenecks." If you want to train an AI model in 2026, you pay TSM's price, or you don't get your chips.

Geopolitics: The Elephant in the Room

You can't talk about TSM stock price history without mentioning the "Taiwan Risk." It’s the reason the stock often trades at a lower P/E ratio than software companies with similar growth.

✨ Don't miss: Heritage Tractor Galesburg IL: Why This Shop Still Matters to Local Farmers

To hedge this, TSM has been building like crazy outside of Taiwan. They’ve poured over $165 billion into U.S. operations, including a massive "GigaFab" cluster in Phoenix, Arizona. Recently, in early 2026, reports surfaced about even more expansion in the U.S. as part of trade deals intended to lower tariffs.

While these global fabs are expensive and initially hit margins, investors are starting to see them as "insurance." If 70% of the leading-edge capacity stays in Taiwan, but the remaining 30% is diversified, the "catastrophe discount" on the stock price starts to shrink.

Why the "Foundry 2.0" Strategy Matters

TSM recently started talking about "Foundry 2.0." This basically means they aren't just making the silicon wafers anymore. They are doing the packaging (CoWoS), the testing, and the mask-making.

Advanced packaging is the new secret sauce. As we hit the physical limits of how small a transistor can get, we have to start stacking chips on top of each other. TSM’s CoWoS capacity is expected to reach 90,000 wafers per month by the end of 2026. This isn't just a technical detail—it’s a massive revenue driver that competitors like Intel and Samsung are struggling to replicate.

👉 See also: Musk Takes Over Treasury: What Most People Get Wrong

Actionable Insights for Investors

If you're looking at the historical data and wondering what's next, keep these points in your back pocket:

- Watch the Capex: TSM just signaled 2026 capital expenditure (spending on new equipment/fabs) between $52 billion and $56 billion. When TSM spends that much, it's because their customers (Apple, Nvidia, AMD) have already promised to buy the output. It’s a huge "buy" signal for long-term demand.

- The "AI Accelerator" CAGR: Management expects AI-related demand to grow at a mid-40% compound annual rate through 2029. If that holds, the current valuation might actually be "cheap" despite the record highs.

- Inventory Cycles: Historically, semiconductors are cyclical. We see 2-3 years of boom followed by 1 year of "digestion." We’ve been in a boom since early 2024. Keep an eye on PC and smartphone lead times; if those start to stretch too thin, a cooling period might be due in late 2026 or 2027.

- Dividend Growth: TSM has paid a dividend since 2004 and has never reduced it. It’s a "growth" stock that acts like a "value" stock in terms of reliability.

Your next steps: Start by reviewing the 2026 guidance from the mid-January earnings call. Pay close attention to the "N2" (2-nanometer) timeline. That process is slated for volume production soon, and if it yields well, it will be the next major catalyst for the stock price. You should also monitor the U.S.-Taiwan trade negotiations regarding tariff reductions, as a drop from 20% to 15% could immediately pad the bottom line for ADR holders.