Money isn't just the paper in your pocket. It’s a flood. Sometimes it’s a drought. If you've looked at the price of a ribeye steak or a used Ford F-150 lately and felt a physical pang of annoyance, you’re actually feeling the ripples of the United States M2 money supply.

Most people ignore the "M" words. They sound like something whispered in a wood-paneled room at the Federal Reserve. But honestly? M2 is basically the thermostat for the entire American economy. When it’s turned up too high, everything gets uncomfortably hot. When it’s dialed back, things start to freeze. For the first time in decades, we are seeing the thermostat get cranked in directions we haven't seen since the era of disco and bell-bottoms.

💡 You might also like: Converting NIS to Dollars: What Most People Get Wrong About the Shekel

What the Heck is M2 Anyway?

Let's keep it simple. The Federal Reserve classifies money into different "aggregates." M1 is the really liquid stuff—physical cash, coins, and the money sitting in your checking account that you can spend with a debit card swipe right this second.

M2 is the bigger brother.

It includes everything in M1 plus "near money." We're talking about savings accounts, money market securities, and time deposits like CDs. It’s the total pool of liquid assets that households and businesses can get their hands on relatively quickly. If M1 is the water in your glass, M2 is the entire plumbing system of the house.

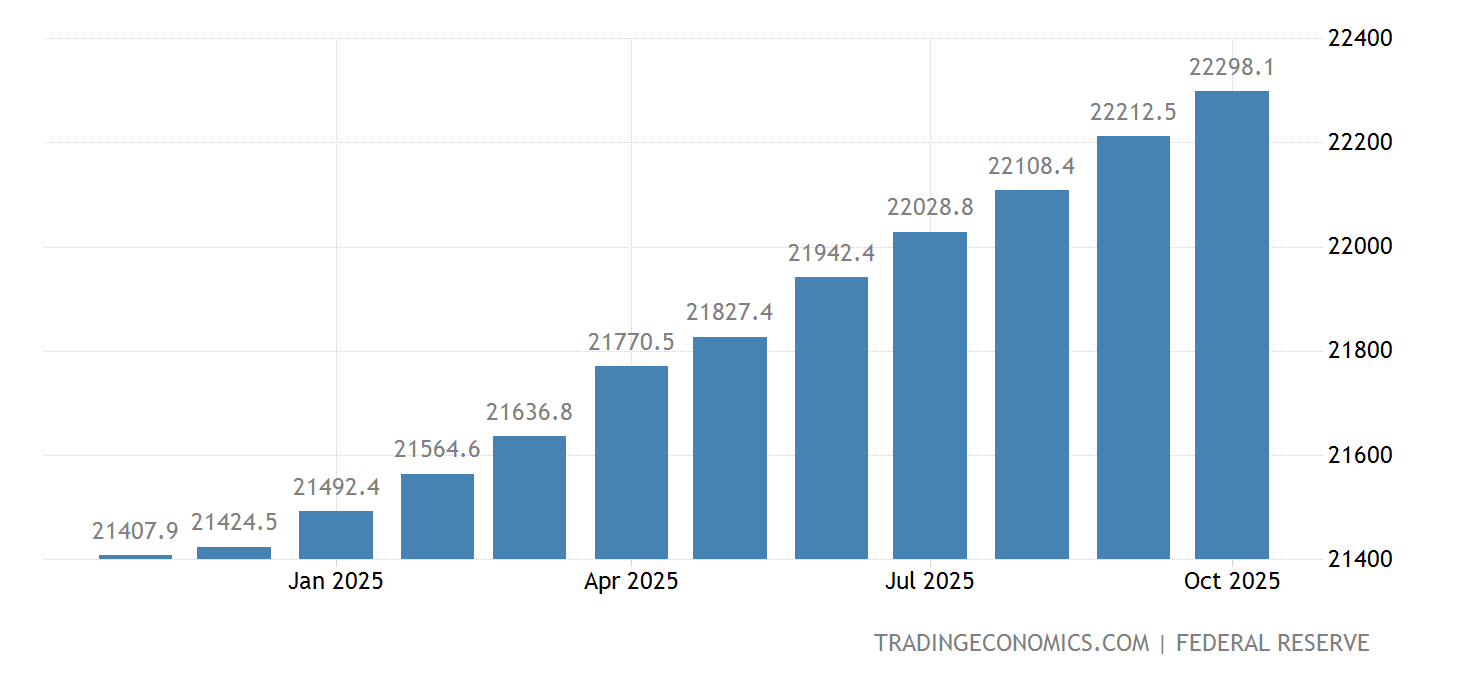

For nearly seventy years, this number only went one way: Up. It was a slow, steady climb. Then 2020 happened. The world stopped, and the government decided to floor the accelerator. Between February 2020 and the peak in 2022, the United States M2 money supply exploded by roughly 40%. That is a staggering, almost incomprehensible amount of liquidity pumped into the system in a heartbeat.

You saw it in stimulus checks. You saw it in PPP loans. You saw it in the Fed buying up bonds like they were going out of style. But you can't just add 40% more money to a system without the price of "stuff" reacting. It's basic math, even if it's painful math.

The Great Contraction: Something Weird is Happening

Here is the part that should make you sit up. Since late 2022, the M2 money supply started doing something it almost never does. It shrank.

Actually, to be precise, we saw the first year-over-year decline in M2 since the Great Depression. Let that sink in. We aren't just talking about a "slowdown" in growth. We are talking about money actually vanishing from the system. When Milton Friedman, the godfather of monetarism, talked about the relationship between money and prices, he made it clear: inflation is always and everywhere a monetary phenomenon.

Why did it shrink? Because the Fed finally got scared.

They hiked interest rates at the most aggressive pace in history to suck that liquidity back out. Quantitative Tightening (QT) became the name of the game. They stopped reinvesting in maturing bonds, effectively deleting money from existence. It’s the ultimate "reset" button, but the button is sticky and it’s making a lot of noise.

Why This Matters for Your Savings

If you have money in a high-yield savings account right now, you’re finally winning. For a decade, savers were essentially punished. With the United States M2 money supply being reigned in, the "cost" of money has gone up. Banks actually have to compete for your deposits again.

But there’s a dark side.

When the money supply shrinks, credit gets tight. You’ve probably noticed that getting a mortgage or a car loan feels like an interrogation lately. Banks are becoming stingy. They’re looking at their balance sheets and realizing the era of "easy money" is over. This creates a "liquidity crunch" where small businesses can't expand, and families can't easily move houses. It’s a cooling effect that's meant to kill inflation, but it often kills growth right along with it.

The Velocity Factor

There’s a secret ingredient most people miss: Velocity.

Velocity is how many times a dollar changes hands in a year. You can have a massive money supply, but if everyone is hoarding cash under their mattress, inflation stays low. During the pandemic, M2 spiked, but velocity crashed because we were all stuck at home. As things "normalized," that velocity picked up. Suddenly, all that printed money started moving. That's when the 9% inflation prints started hitting the headlines.

Now, we’re in a tug-of-war. The Fed is trying to shrink the supply (M2) while people are still spending what they have left.

The Regional Bank Scare and M2

Remember the Silicon Valley Bank collapse? That was a direct side effect of the shifting United States M2 money supply. When M2 shrinks, deposits leave the banking system. People move their cash from 0.01% interest checking accounts into 5% Money Market funds.

Small and medium-sized banks rely on those deposits. When the "pool" of M2 gets smaller, these banks feel the pressure first. It’s a systemic stress test that we are still living through. Every time you see a headline about "banking stability," just remember that it’s really a story about where the M2 is flowing.

What History Tells Us (And What It Doesn't)

Economists like Steve Hanke at Johns Hopkins have been shouting from the rooftops about M2 for years. Hanke argued that the massive surge in 2020 guaranteed the inflation we saw in 2022 and 2023. He was right. Most of the "transitory" crowd at the Fed ignored the M2 data until it was too late.

But now, the debate is on the other side. Some experts worry that the contraction in M2 is too sharp. If you drain the pool too fast, the fish die. Historically, every time we've seen a significant drop in the money supply, a recession followed. No exceptions.

🔗 Read more: ¿Cuánto se cotiza el dólar hoy en México? Lo que nadie te dice del tipo de cambio actual

However, we are in weird territory. Because the 2020 jump was so massive, a slight contraction might just be "returning to the trend line" rather than a death spiral. It’s like a person who gained 50 pounds and is now losing 10. They aren't starving; they're just correcting.

How to Protect Yourself in a Shifting M2 Environment

You can't control the Federal Reserve, but you can control your reaction to the data. Knowing that the United States M2 money supply is tightening should change how you handle your finances.

First, cash is no longer trash. In an era of shrinking liquidity, having a liquid "war chest" is vital. When M2 is expanding, you want to own "stuff" (commodities, real estate, stocks). When M2 is contracting, you want to be the person with the cash when everyone else is forced to sell their "stuff" at a discount.

Second, watch the spread. If the gap between M2 growth and GDP growth stays negative, expect the stock market to be a roller coaster. Markets love liquidity. They hate "quantitative tightening."

Third, stay skeptical of "soft landing" talk. While it’s possible, the historical track record of M2 contractions without a recession is... well, it’s non-existent. Be prepared for a labor market that gets a bit shakier.

💡 You might also like: Who is John Morgan? The Truth About America's Most Famous Lawyer

Actionable Steps for the "New Normal"

Stop waiting for 3% mortgage rates. They were a product of an M2 explosion that we are currently trying to mop up. They aren't coming back anytime soon unless the economy completely falls off a cliff.

- Ladder your CDs. Since the money supply is tight and rates are high, lock in these yields while the Fed is still fighting the M2 bulge.

- De-leverage. If you have high-interest debt, kill it now. In a tightening money environment, debt becomes a much heavier anchor.

- Watch the "M2 Real" data. That’s M2 adjusted for inflation. If real M2 is crashing, it means the purchasing power of the total money supply is evaporating even faster than the nominal numbers suggest.

- Diversify into "Hard" Assets. Even though liquidity is tightening, the long-term trend of the US dollar involves some level of debasement. Gold and Bitcoin often react to the expectation of future M2 growth, even when the current data is flat.

The bottom line? The United States M2 money supply is the most important indicator you aren't watching. It explains why your groceries are expensive, why your savings account finally earns interest, and why the housing market feels like a standoff. Keep your eye on the liquidity. It's the only signal that truly matters in the end.